In the past it was noted that companies reported the asset retirement obligation through taking into account a variety of liabilities. The asset retirement obligation was set up so as to come up a harmonious procedure would be implemented so as to overcome the problem of retiring the long-term asset. Companies should recognize liabilities for the asset retirement obligation during the time when an obligation is incurred and when there is reasonable estimate that a fair value will be made for an asset as per the Statement of Financial Accounting Standards (SFAS) N.O 143.

There are different kinds of approaches that are followed when recognizing the asset retirement obligation, these include: recognition of the asset retirement obligation at fair value without considering the uncertainty that emanates from the timing of the retirement, fair value can be recognized when there is likelihood that asset will be retired and the other approach is that companies may fail to recognize an asset until the time retirement of the asset occurs (Guinn, Schroeder, and Sevi, 2005).

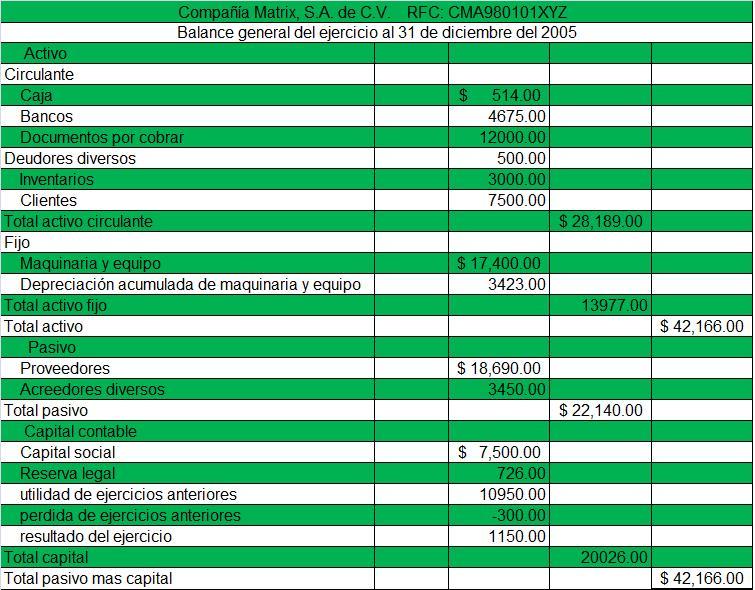

English: Balance Sheet Español: Balance General

English: Balance Sheet Español: Balance General Componenets of the asset side of the Federal Reser...

Componenets of the asset side of the Federal Reser... Schroeder, Major Rudolph W.

Schroeder, Major Rudolph W.An asset refers to the act of getting rid of a long-lived asset through various methods such as; selling, abandoning, recycling or disposing of the asset, but this policy does not apply to the assets that do not contribute to the production of output for an according to the Statements of the Financial Accounting Standards (SFAS) . The exposure draft of Financial Accounting Standards Board (FASB) staff states that the staff's legal obligation to undertake asset retirement activity is based on the fact that a condition on the future event should be within the scope of Statements of the Financial Accounting Standards (SFAS) No.143.

Statements of the Financial Accounting Standards (SFAS) No.143 also states that an entity during acquisition,construction,development or in normal operation of the asset should recognize the assets fair value so as to perform the asset retirement activity when obligation is been incurred .

The Black Gold Inc was a company that was required to construct and to operate offshore oil platforms. The management of the company was expected to remove the platform after a period of 10 years. The construction process began on January 1 20x1 at the coast of Alaska.Capitalisation cost would amount of $1 million which would be depreciated after a period of 10 year using the straight line method.

Black Gold (BG) would recognized the liability for the Asset Retirement Obligation (ARO) as being associated with the getting rid of the platform .This implies that it followed and procedures that were under Statements of the Financial Accounting Standards (SFAS) No.143which required that companies to carry out the asset retirement within their organization. The company used $100,000 to represent its fair value of liability using the expected present value technique .Asset Retirement Cost (ARC) was established as an amount that involved carrying amount of the related platform of the balance sheet.

On December 20x8 there were instances of depreciation and application of interest method of allocation (accretion expense) which showed a net carrying value of the oil platform as being $200,000 asset retirement cost amounted to $ 20,000 while the asset retirement obligation resulted to $175,000.

During the first quarter of 20x9 due to changes in marketplace for labor cost to dismantle oil platform there was a downward adjustment of asset retirement obligation of $50,000 and a resulting balance of $125,000 ( Guinn, Schroeder, and Sevi, 2005)a).The way Black Gold (BG) would offset the entry related to $50,000 downward adjustment while recording the asset retirement obligation in the balance sheet during the first quarter of 31st march 20x9 was: that the management of the company would offset the entry recorded in the accounting principle cumulative effect adjustment that would be later on reflected in the income statement.

Companies should consider the following factors when performing their operations these are ;liability for the existing asset retirement obligation should be adjusted for the cumulative accretion during the date when this interpretation is being adopted, where there is an increase in carrying amount that is associated with long-lived asset, when the adjusted accumulated depreciation results from increased cost and finally when capitalized cost of the underlying asset is been assessed for impairment as per the paragraph 12 of Statements of the Financial Accounting Standard.

The amounts of assets and liabilities under the SFAB 143 are recorded each year as accretion and depreciation expenses the capitalized asset retirement would be allocated in a rational and systematic manner while the depreciation expense would be recorded over the estimated useful life of the asset (Guinn, Schroeder, and Sevi, 2005)Depreciation would be calculated through increasing the asset base by dividing using the assets useful life which is adopted by Statements of the Financial Accounting Standards (SFAS) 143 .The accretion expense is calculated through multiplying the balance of recorded liability while using the company's credit-adjusted discount rate that occurs each year that is also referred to as amortization of the present value discount that is associated with the asset retirement obligation.

b). The period and amount that Black Gold (BG )would account for the decrease that is related to $50,000 downward adjustment recorded to asset retirement obligation in its income statementAccording to SFAS 143 the present value of asset retirement obligation of $175,000 should have been capitalized and recorded as a liability on January 20x1.The management of the company should have also recorded the annual accretion expense of the carrying value of the liability and the additional depreciation of the asset.

The company experienced $50,000 downward adjustment because it had not recorded or depreciated the retirement cost from 20x1 to 20x8 which resulted to cumulative effect of a loss or downward adjustment. The loss is as a result of the catch up effect that is related to depreciation and accretion expense incurred for a period of 7 years (Guinn, Schroeder, and Sevi, 2005)It is important to note that when calculating the asset retirement obligation care should be taken as it involves numerous adjustments and assumptions in order to give a correct answer to a question that one is been asked .The assumptions that are involved in this process are estimation of the properties, life that should be retired, settlement amounts, inflation factors, credit-adjusted discount rates, time of settlement and changes in legal regulatory and environmental landscape.

ReferencesGuinn, R.E., Schroeder, R. G. and Sevi, S. K. "Accounting for Asset Retirement Obligations Understanding the Financial Statement Impact SFAS N.O 143," Understanding the Financial Statement Impact, December 2005, available at http://www.nysscpa.org/cpajournal/2005/1205/essentials/p30.htm

English: Real estate economics - with depreciation

English: Real estate economics - with depreciation English: Components of the asset side of the Feder...

English: Components of the asset side of the Feder... English: A graph of the depreciation of a 1993 Dod...

English: A graph of the depreciation of a 1993 Dod... 4 Depreciation methods (1:Straight-Line method, 2:...

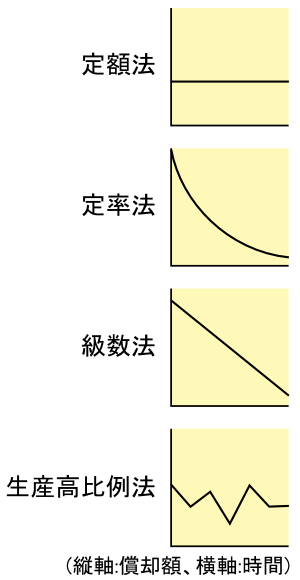

4 Depreciation methods (1:Straight-Line method, 2:...