Accounting for Decision Makers Investment Case Study Scenario |

2013/2014 MOD003674 |

Julia Lutze 1306484 |

�

Contents

Introduction 2

The Accounting Rate of Return 3

Payback Period 4

Net Present Value 6

Internal Rate of Return 9

Conclusion 11

References

�

Introduction

The following case study discusses and criticises the techniques that are generally used to appraise investment decisions. The question is how businesses can make decisions involving new assets such as a new container system. In order businesses should try to go after their key financial objectives, which is to raise the owners (shareholders) wealth. The principal feature of investment decisions overall is time (Atrill, McLaney, 2013). It includes setting the expenses of something of economic value at a certain point of time, mostly cash, which prospectively will make a return to the investors at another point of time. Furthermore mostly large amounts are involved and it might be expensive as well as not possible to bail out of an investment once it is carried out.

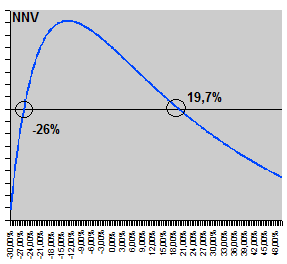

ARR, pt. 1

ARR, pt. 1 Figure 1

Figure 1 English: Internal rate of return, twp solutions Sv...

English: Internal rate of return, twp solutions Sv...Appraisal techniques are an important field for businesses because expensive and significant consequences can be caused by bad investment decisions. Given the importance of investment decisions, it is to ensure that investment proposals are profoundly approved; the business therefor needs appropriate methods of evaluation. These theories are broadly divided into two groups: the ones that adjust the time value of money and those that do not - the more traditional methods. Commonly four methods are known: accounting rate of return (ARR), payback period (PP), net present value (NPV) and internal rate of return (IRR) (Atrill, McLaney, 2013). Each method is going to be assessed in terms of effectiveness with regards to the White Bros plc. case study and whether the investment in a new container system is advisable; the short terms stated above...