�PAGE � �PAGE �4� Accounting

Accounting Regulatory Bodies

Ardelia Thompson

University of Phoenix

ACC/300

Jonathan Henry

April 28, 2009

Accounting Regulatory Bodies

Accounting regulatory bodies is an association that is self regulated by management and it is to alleviate accounting scandals by ensuring all accountants are following the generally accepted accounting practices known as GAAP. Most businesses have concerns about the role of a certified public accountant known as CPA in the financial system. There are numerous of companies in the world who cover up the accounting scandals until the incidents arise such as Mark Sanford scandal. In the paper I will examine at least four accounting regulatory bodies and discuss how an organization complies with the standards of the regulatory bodies.

The Financial Accounting Standards Board (FASB) sets the underlying rules of accounting (Libby, Libby, and Phillips, 2006). The rules set by the FASB are the main source of GAAP rules.

Libby

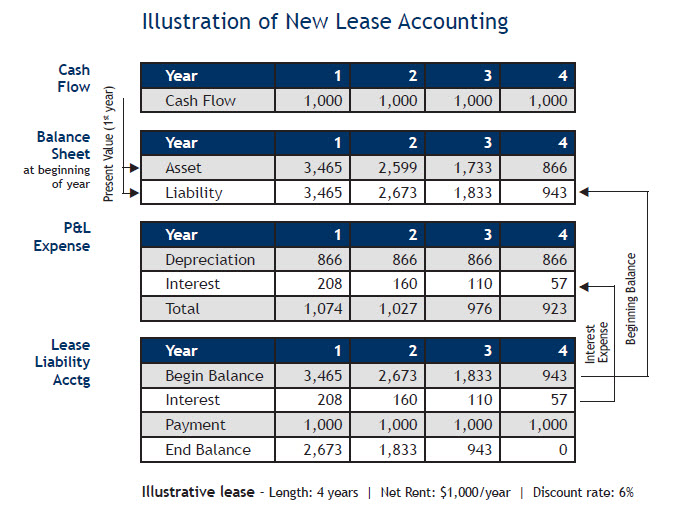

Libby English: Illustration of new lease accounting

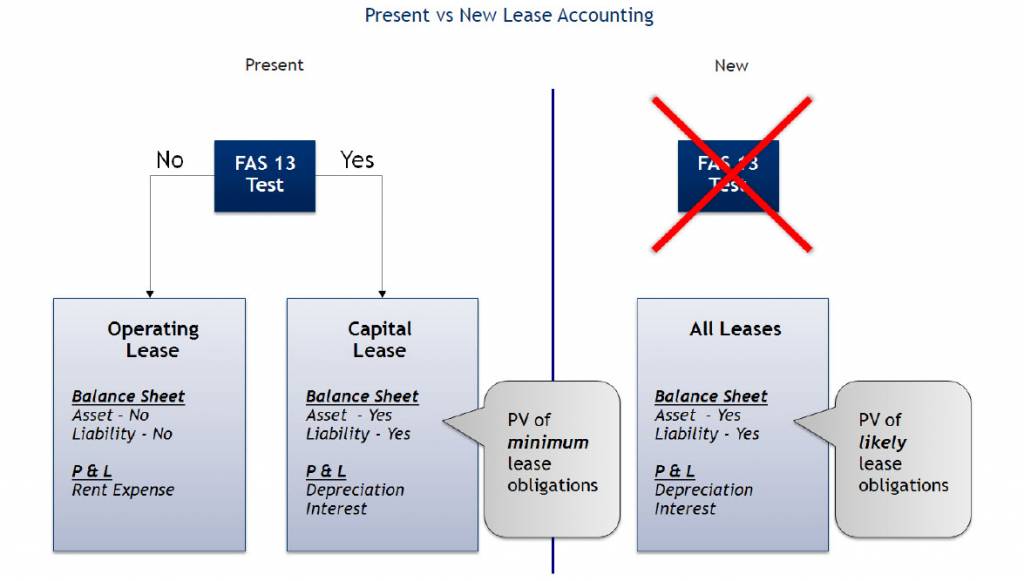

English: Illustration of new lease accounting English: Present vs. New Lease Accounting Standard...

English: Present vs. New Lease Accounting Standard...The purpose of the FASB is to establish and improve principles of financial accounting and reporting to direct and educate the public, including issuers, auditors, and users of financial information. FASB ensures standards are up to date reflecting any changes in the way of conducting business and changes in the economy.

The Public Oversight Board (POB) is an organization which oversees peer review, the quality control inquiry, and other activities of the United States. The POB is usually individuals who are not accountants. The purpose of the POB is to ensure professional services and sufficient quality. The Public Oversight Board issues an annual report that lists all revenues of the previous year.

Several international companies use the International Accounting Standards Board (IASB). The purpose of IASB is to develop a set of high quality international financial reporting standards for the general purpose of financial statements. In 2002,