Before the 1980s, majority of the companies were manufacturing units, producing a limited range of products, with material and direct labour being the paramount costs. Since overhead costs were low and information computing costs high, the companies were satisfied using traditional product costing methods. The emergence of the 1980s, brought with it intensive competition across the globe and growing importance of overheads while that of direct labour declined (Drury, C., pp 225). Also there were problems that were being faced with traditional cost systems. The use of traditional costing lead to a distortion of data as it allocated indirect manufacturing costs by using volume-related formulae. These formulae were actually based on direct labour or direct material and the percentage contributed by these costs towards the product or service was a relatively small amount. The information thus provided by these systems was inaccurate and lead to incompetent decisions being taken on account of matters such as capital investment and product policy.

English: Simprocess integrates Process mapping, de...

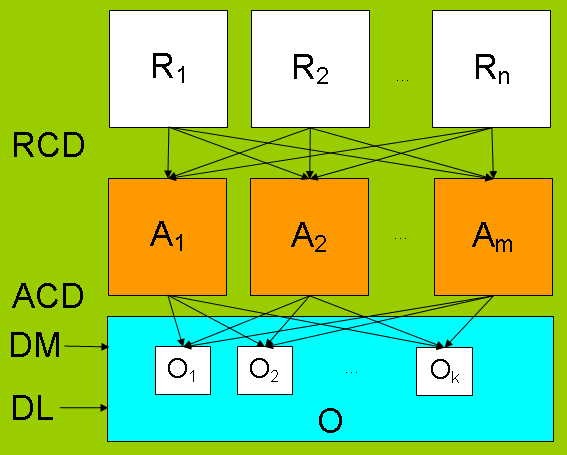

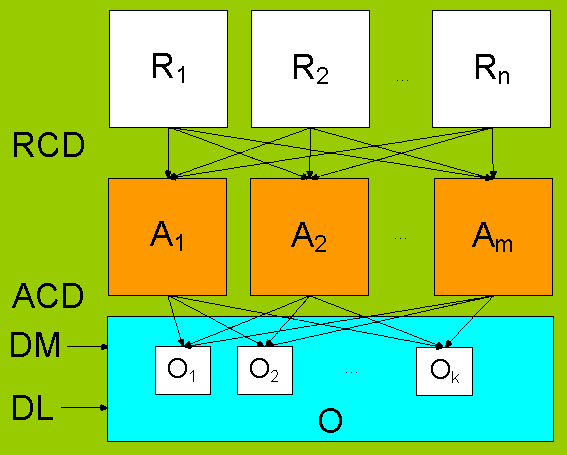

English: Simprocess integrates Process mapping, de... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver...The information would also misdirect the management in terms of the financial situation of the company, this lead to decline in profit (Macintosh, N.B.).

Therefore the changing corporate environment and problems with the traditional costing systems brought about a need for an alternative cost system that was both innovative and sophisticated. This alternative as suggested by Cooper and Kaplan (1988) was Activity Based Costing (ABC) based on the following theory (Harvard Business Review (1988)):

"Virtually all of a company's activities exist to support the production and delivery of today's goods and services. They should therefore all be product costs."

Further on they published a series of articles that explained the key ideas that supported ABC type systems. These articles lead to an appreciable amount of popularity and implementation of ABC by a number of companies, so much so that a...