Background

The opening up of the insurance industry to private sector participation in December 1999 has led to the entry of 20 new players, with 12 in the life insurance sector and eight in the non-life insurance sector. Almost without exception these companies are seeking to utilise multiple distribution channels such as traditional agency, bancassurance, brokers and direct marketing. Bancassurance is seen by many to be a significant or even the primary channel (the latter being the case for at least SBI Life).

In other Asian markets we have seen bancassurance make significant headway in recent times. For example, bancassurance accounted for 24% of new life insurance sales by 'weighted' premium income in Singapore in 2002. This is a significant increase on the equivalent 2001 statistic of 15% and is as a result of growth in significant bank-centric bancassurance operations. In Hong Kong the figure for 2002 is expected to be at the 20% level for the same basic reasons.

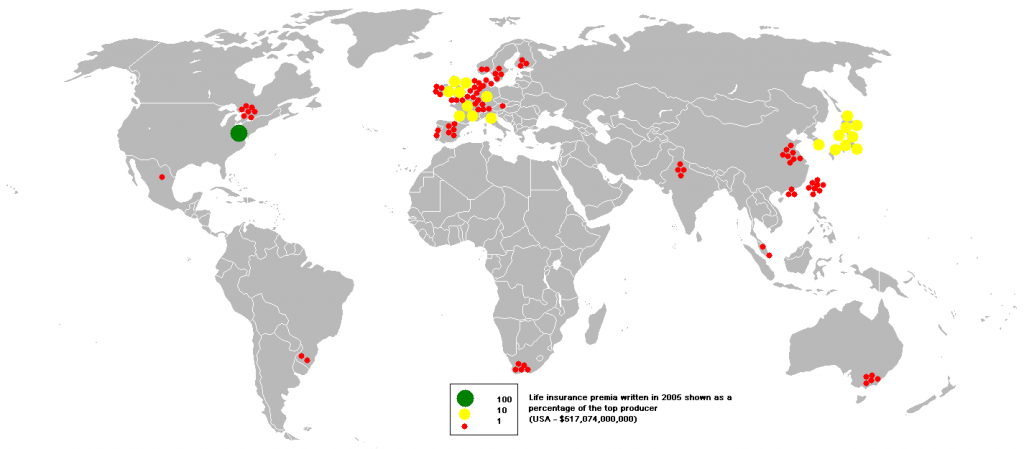

English: This bubble map shows the global distribu...

English: This bubble map shows the global distribu... Chinese Bank of China

Chinese Bank of China insurance broker

insurance brokerWhy bancassurance in India?

The management of the new Indian operations is conscious of the need to grow quickly to reduce painful start-up expense overruns. Banks with their huge networks and large customer bases give insurers an opportunity to do this efficiently.

Regulations requiring certain proportions of sales to the rural and social sectors give an added impetus to the drive for bancassurance. Selling through traditional methods to these sectors can be inefficient and expensive. Tying up with a bank with an appropriate customer base can give an insurer relatively cheap access to such sectors. This is still an issue for insurers despite the recent widening of the definition of the rural sector (so that it now accords with the census definition).

In India, as elsewhere, banks are seeing margins decline sharply in their core lending business. Consequently, banks are...