The major changes that are included in IFRS 9 will be discussed in this paper. IFRS 9 is a better replacement of IFRS 39 or IAS 39. It should be said that IFRS 9 has introduced some better changes that were not evident in IAS 39. The major changes that are being introduced in accordance with the new perspective i.e. IFRS 9 are as below:

Classification and Measurement

The first major change is related to classification and measurement. It determines as to how the financial assets and liabilities undergo an accounting process in the annual statements of any particular company. Therefore, with the introduction of IFRS 9, a logical approach is set up for the classification of assets. This is also driven by the characteristics of the cash flow and the business model where the asset is held. This approach provides a great replacement for the already existing rules that are truly complex and not easy to comprehend (Istrate, 2013).

Image of a waterfall chart showing profit/loss

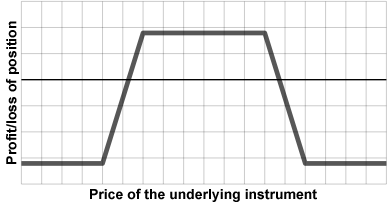

Image of a waterfall chart showing profit/loss Generic Profit/loss graph for a Condor

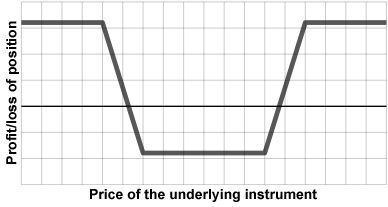

Generic Profit/loss graph for a Condor Profit/loss graph of a short condor

Profit/loss graph of a short condorThe new IFRS 9 also provides a great impairment that is applicable to other financial instruments so as to eliminate the source of complexity that is particularly associated with prior requirements of accounting.

Impairment

Another great change is related to impairment. It is also noted that during the financial crisis, the identification of the losses from credit on loans and various financial instruments is found to be the weakness in the existing FRS 39 standards. With the introduction of IFRS 9, there is an introduction of a brand new, loss impairment model that needs more time to get recognition in accordance with the losses of credit. Therefore, the new IFRS 9 will need the entities to be accountable for losses on credit when the financial instruments get recognition which then lessens the threshold of identification for full losses on credit...