Running head: BUSINESS ACCOUNTING ASSIGNMENT

�

ANSWER TO SUB-QUESTION [A]

The statement of comprehensive income is defined as the change the change in equity of a business enterprise during a period from transactions and other events and circumstances from non-owner sources. It includes all changes in equity during a period except those resulting from investments by owners and distributions to owners (Fasb.org, 2014).

The general purpose of the statement helps financial statement users evaluate the past financial performance of a company and provides them a basis for predicting future performances. Financial statement users need this information to assess potential changes in the entities economic resources and its ability to generate cash from those resources. Financial statement users can also use this information to evaluate how any additional resources might be effectively used. This statement requires all income statement items to be reported either as a regular item in the income statement or a special item as other comprehensive income (Fasb.org,

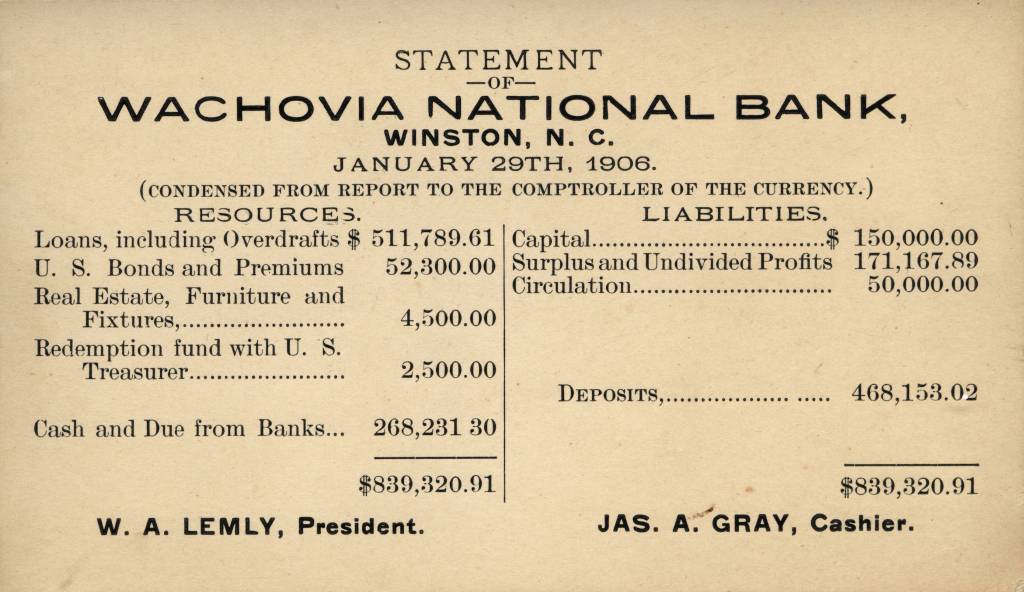

Historical financial statement

Historical financial statement English: BoT and BoE financial statement 2010 meet...

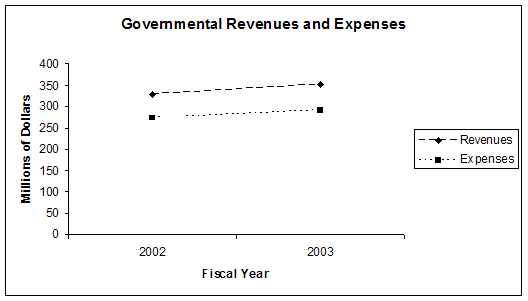

English: BoT and BoE financial statement 2010 meet... English: Seminole County, Florida Revenues and Exp...

English: Seminole County, Florida Revenues and Exp...2014).

�

Income statement, also known as Profit and Loss Account, indicates how the revenues (money received from the sale of products and services before expenses are taken out, also known as the "top line") are transformed into the net income (the result after all revenues and expenses have been accounted for, also known as "net profit" or the "bottom line"). It displays the revenues recognized for a specific period, and the cost and expenses charged against these revenues, including write-offs and taxes (Helfert, E. A., 2002).

Other comprehensive income represents certain gains and losses of the company that are not recognized in the Profit and Loss Account. Some items that comprise this income include unrealized gains and losses on available for sale securities, gains and losses on derivatives held as cash flow hedges, gains and losses resulting...