Executive Summary:In my business report I will be stating and discussing the five major financial institutions in Australia. I will be giving detail on one in particular and the different types of loans available to consumers. I will also inform consumers on the rights and responsibilities of borrowers who take out a loan. I will also compare and evaluate the four different types of credit cards available, their intrest rates, the annual fees and the intrest free period.

1.Financial Institutions:In Australia there are at least four main financial institutions. These are:ÃÂBanks: A bank is a financial institution that acts as a payment agent for customers and to borrow and lend money. They provide a wide range of financial services including funds management, superannuation and insurance services. Some examples of banks include ANZ, Westpac, NAB and Commonwealth bank.

ÃÂBuilding societies: is a financial institution that is owned by its members that offers banking and other financial services especially mortgage lending.

English: Old Commonwealth Bank of Australia saving...

English: Old Commonwealth Bank of Australia saving... insurance broker

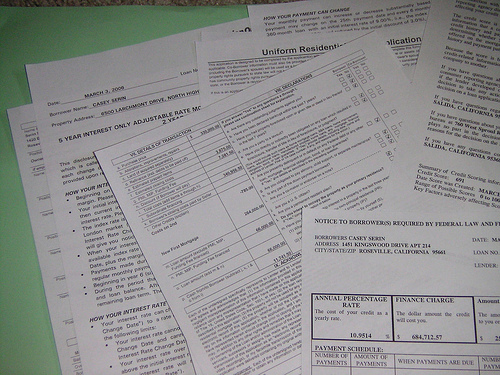

insurance broker My Mortgage Docs to be Reviewed by an Expert

My Mortgage Docs to be Reviewed by an ExpertSome examples of building societies are IMB, Greater building society, Newcastle Permanent building society, ABS building society and Hume building society.

ÃÂCredit Unions: is a non-profit financial institution that is privately owned and in which members vote the bored of directors. Some examples of credit unions are teachers credit union, Qantas credit union and Sydney credit union.

ÃÂFinance companies: is a financial institution which provides business loans for business development and any personal loans for the perchase of cars, etc. An examples of a finance companie is the AFSD.

ÃÂInsurance companies: is a company that offers protection and coverage from lost, theft or fire. There are two types of insurance companies. These are life insurance and general insurance. Some examples of insurance companies are AAMI, Allianz, AMP, NRMA and CGU.

2.Types of loans:The Commonwealth Bank provides a wide range of loans and financial services. Some of the different types of loans include:ÃÂPersonal loans (Fixed rate): A personal loan is a loan offered by the Commonwealth Bank to clients who wish to purchase personal items like computers, televisions and mobile phones.

ÃÂTertiary Student loan: A tertiary student loan lets full-time tertiary students at University, TAFE, Agricultural College or registered training organisations to borrow money to pay for fees, books, computers, cars, etc.

ÃÂBusiness loan (fixed loan): A business loan is a loan that is offered to fund the businessÃÂ growth, expansion or finance. The Commonwealth Bank provides the BetterBuisness for these purposes.

ÃÂHome loan (Variable rate): Commonwealth bank provides a wide range of home loan services like low interest rate home loans and packages. The loan is offered to people who want to buy, build, invest and renovate a home.

Rates and fees:When applying for a loan there are also some rates and some fees that you have to pay on top of the loan repayments. These are different for each loan.

Personal loan (fixed rate):ÃÂEstablishment fee $135ÃÂGuarantee fee $120ÃÂExcess cheque fee $5.40ÃÂCancelled cheque fee $10ÃÂLoan service fee $10 monthlyÃÂLate payment fee $45ÃÂOverdrawing approval fee $30ÃÂRepayment redraw fee $10ÃÂSwitching fee $70ÃÂAdministrative fee $50ÃÂDeferred establishment feeÃÂOther electronic banking feesÃÂGovernment chargesTertiary Student loan:ÃÂEstablishment fee -There is no establishment fee for a Campus Loan.

ÃÂEarly repayment fee ÃÂ there is no early repayment fee and if they pay off the loan early there is less interest.

Buisness loan:ÃÂEstablishment fee $180ÃÂCancelled cheque fee $10ÃÂLate payment fee $50ÃÂGovernment chargesÃÂSwitching fee $70ÃÂAdministrative fee $50ÃÂDeferred establishment feeÃÂLoan service fee $12 monthlyHome loan:12 Month Discounted Variable RateThis enables customers to get a head start on paying off the home loan. The discounted rate is only available for new loans, and at the end of the discounted period the interest rate converts our current standard variable rate. Alternatively, you can choose another home loan option (a switching fee applies).

ÃÂEstablishment fee $250 up front or $450 for the variable loanÃÂService fee $8Loan Term and Amount:Personal loan:ÃÂWhen you borrow a personal loan fom the Commonwealth bank you can borrow between $5,000 and $50,000. The loan term is from 1-7 years.

Student loan:ÃÂFor a student loan you can borrow up to $5,000. This loan has no repayments till you graduate.

Buisness loan:ÃÂFor a business loan the loan amount needs to be over $50,000. The loan term is from 1-10 years.

Home loan:ÃÂThe loan term is up to 30 years and the Commonwealth bank has a means test that determines what you can afford to repay which is how they determine the amount of the loan.

Interest Rates and Comparison Rates:Personal loan:ÃÂThe intrest rates are from 14.95% pa and the comparison rate is 17.95% paStudent loan:ÃÂThe Interest rates are from 14.75% p.a and the comparison rate is 17.75% p.a.

Business loan:ÃÂThe intrest rates are from 10.55% pa and the comparison rate is 12.75% paHome loan:ÃÂThe intrest rates are from 9.35% pa and the comparison rate is 9.56% pa.

3.Basic rights and responsibilities for consumers:As a loan borrower there are many rights and responsibilities that have to be known. Some of these include:ÃÂUnderstanding that you will be getting yourself into debt. You will need to pay the principal plus the intrest charges. Find out what type of security, if any, is required.

ÃÂFind out how much the loan is in total. Finding both the principal and the intrest charges and any additional costs, such as fees, stamp duty and government charges.

ÃÂWork out the repayment amounts like how much per repayment, when each payment is due, and finding out how many repayments there are altogether.

ÃÂGetting information on how the charges and any additional costs, are collected.

ÃÂFind out weather you can repay the loan in a shorter period of time and if so looking out for the penalty rates.

ÃÂUnderstanding the consequenses that you will be faced with if you can not make the repayments.

ÃÂAn explanation of available options for consolidating your loans and a statement that you can prepay your loans without penalty at any time.

ÃÂInformation about the maximum repayment periods and the minimum repayment amount.

ÃÂInformation about the yearly and total amounts you can borrow.

Responsibilities:Think about what your repayment responsibility means before you take out a loan. If you don't repay your loan on time you might go into default, which has serious consequences and will affect your credit rating.

You must make payments on your loan even if you don't receive a bill or repayment notice. Billing statements are sent to you as a convenience, but you're obligated to make payments even if you don't receive any reminders. You must also make monthly payments to pay off the loan. Partial payments are not allowed.

If you apply for a deferment or forbearance, you must continue to make payments until you're notified the request has been granted. If you don't, you might end up in default. You should keep a copy of any request form you submit, and you should document all contacts with the organization that holds your loan.

You must notify your loan servicer when: you graduate; withdraw from school; drop below half time status; change your name, address, or Social Security Number; or transfer to another school if you have a student loan.

Do not sign any loan documentation without carefully reading it and understanding its contents. If you are unsure of anything in the contract, ask the lender for clarification or preferably get independent advice from either a solicitor or financial advisor before signing.

When you take out a loan must be handed a document stating all the condition that apply to the loan. You can also receive a credit contract. Each credit contract and pre-contractual statement must include:ÃÂthe amount of credit to be providedÃÂthe annual percentage rateÃÂhow the interest will be calculated and when it will be chargedÃÂthe total amount of interest if the contract is paid out within seven yearsÃÂthe credit fees and charges and how changes will be advisedÃÂany default rate of interest and how it will be calculatedÃÂthe frequency of account statementsÃÂrelevant commission chargesÃÂif mortgage guarantee insurance appliesÃÂdetails of credit-related insuranceÃÂloan termÃÂrepayment schedule4.Comparison of credit cards in AustraliaBelow is a table of 4 different types of credit cards available to consumers, the intrest rates of these cards, the intrest free perid, annual fees, etc. mastercard visa card American express dinners card*(table included in attachment folder)BIBLIOGRAPHY:http://en.wikipedia.org/wiki/Financial_institution. retrieved: 5/3/08http://en.wikipedia.org/wiki/Bank. Retrieved: 7/3/08http://www.commbank.com.au/ (i then clicked on personal and business loans for more information) Retrieved: 7/8/08http://www.anz.com/personal/home%2Dloans/rates%2Dfees/. Retrieved: 8/8/08http://en.wikipedia.org/wiki/Student_loan. Retrieved: 8/8/08

Commonwealth Bank

Commonwealth Bank English: building located at Martin Place, .

English: building located at Martin Place, .