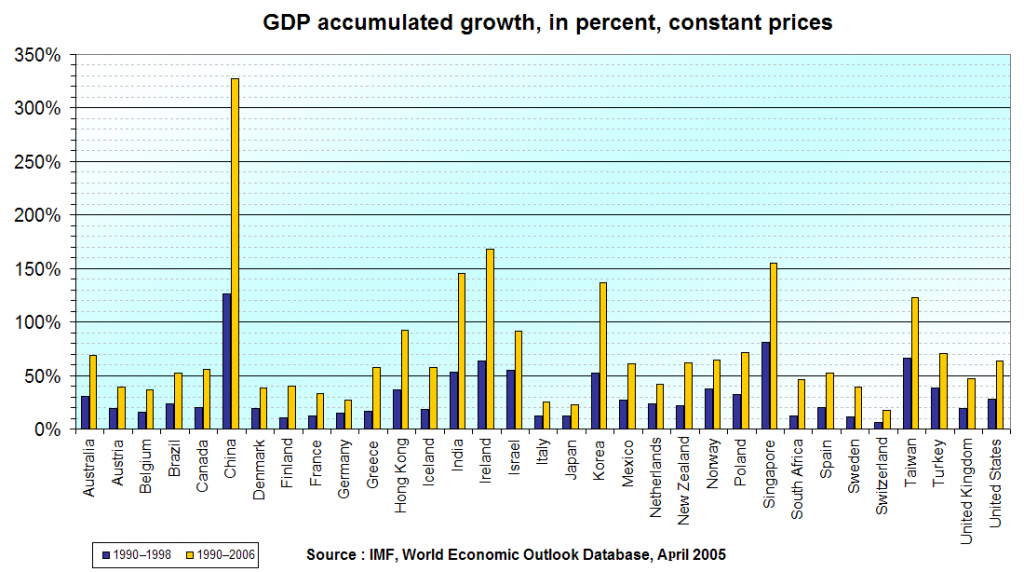

The world economy is at a crossroads. Continental Europe is stuck, emitting only faint signals of revival. Little surprise--no region can ever grow under the gravity of declining populations, 35-hour workweeks and scant entrepreneurs, especially those of the immigrant variety. Japan looks a bit better if you believe the Nikkei's 23% bump this year foreshadows better days. The Land of the Rising Sun has shown us false dawns before. Still, I think we'll finally begin to see GDP growth of 2% or more coming from Japan. That would be good news. The U.S. is clearly the strongest of the G-8 member nations, clipping along at a 3% growth rates or better. This should continue during 2001. But our economy is still underperforming to its potential. Evidence is the 2:1 gap that now exists between GDP growth rates and those astonishing 6% to 7% productivity growth rates that have been recorded this year.

Gross domestic product growth in the advanced econ...

Gross domestic product growth in the advanced econ... United States

United States United States

United StatesOf course, if you're a bull you'll argue that the GDP/productivity gap is a mere lag effect. GDP will catch up to productivity. It always does. By this logic, you chould expect 2004 to be a wildly good year and invest accordingly. Others wonder about that. Yes, GDP has always caught up to productivity before. But the landscape has changed. Now the Mayo Clinic e-mails X rays and MRIs to radiologists in Bangalore. High value-added jobs, in other words. Some experts think the U.S. will outsource 25 million jobs--mostly white collar--to India and China during the next ten years. This trend will spike U.S. productivity, even as it temporarily displaces millions of Americans, who then will downsize their mortgages, car payments and vacations. The net effect is that the American GDP/productivity gap could become a fixture of the early 2000s.

If the GDP/productivity gap continues, along with the...