(A) Rules-based accounting standard

Rule-based systems are fairly simplistic, consisting of little more than a set of if-then statements, but provide the basis for so-called "expert systems" which are widely used in many fields. The concept of an expert system is this: the knowledge of an expert is encoded into the rule set. When exposed to the same data, the expert system AI will perform in a similar manner to the expert.

Rule-based systems are a relatively simple model that can be adapted to any number of problems, rule-based systems are really only feasible for problems for which any and all knowledge in the problem area can be written in the form of if-then rules and for which this problem area is not large. If there are too many rules, the system can become difficult to maintain and can suffer a performance hit.

Rules-based accounting provide a list of detailed rules to follow, the list of rules clearly tell you how to do and provide the exactly format, no any professional judgments is needed.

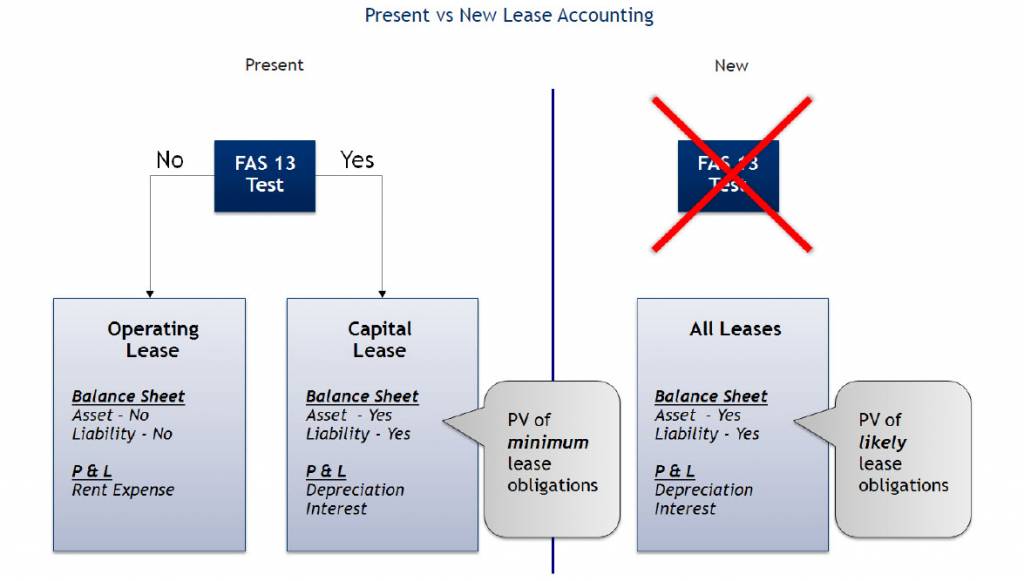

English: Present vs. New Lease Accounting Standard...

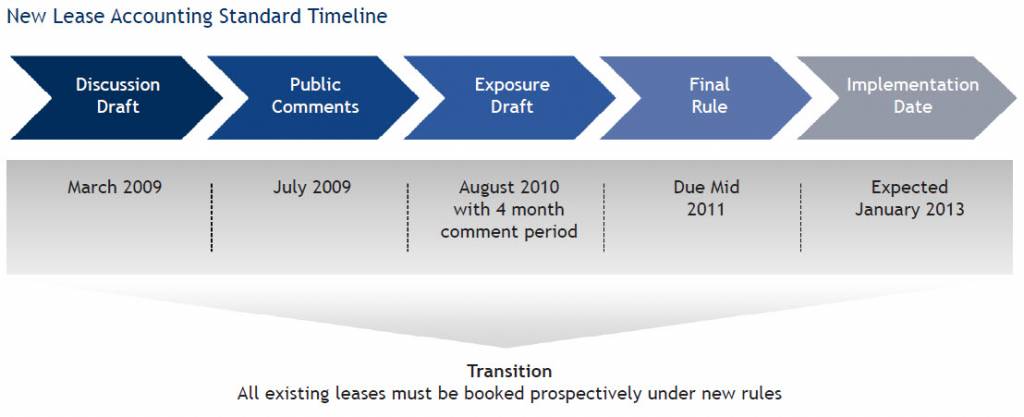

English: Present vs. New Lease Accounting Standard... English: New lease accounting standard timeline

English: New lease accounting standard timeline Accounting Professional & Ethical Standards Board

Accounting Professional & Ethical Standards BoardAdvantages of Rules-based accounting standard

(1) The rules can increase the accuracy with which standard setters communicate their requirements and increase comparability.

(2) The rules increase verifiability for auditors and regulators and a related reduction in litigation.

(3) The rules reduced opportunities for earnings management through judgments, can reduce the sort of imprecision that lead to aggressive reporting choices by managements.

Disadvantages of Rules-based accounting standard

(1) Rules-based system is problematic because those who want to comply with rules are not always sure of everything they need to look at. Those looking to get around the rule can use legalistic approaches to try and do it.

(B) Principles-based accounting standard

Principles-based accounting provides a conceptual basis for accountants to follow instead of a list of detailed...