1. Dividend Growth ModelThe basic assumption in the Dividend Growth Model is that the dividend is expected to grow at a constant rate. That this growth rate will not change for the duration of the evaluated period. As a result, this may skew the resultant for companies that are experiencing rapid growth. The Dividend Growth Model is better suited for those stable companies that fit the model. Those that are growing quickly or that don't pay dividends do not fit the assumption parameters, and thus this model cannot be used. In this model, a company may not exceed the market growth rate.

In addition, since the dividend growth rate is expected to remain constant indefinitely, the other measures of performance within the company are also expected to maintain the same growth rate. If in the current state, the dividend rate is greater that earnings, in time this model will show a dividend payout greater than the earnings of the company.

English: Metropolitan Life Bldg., Manhattan, New Y...

English: Metropolitan Life Bldg., Manhattan, New Y... English: The offices of the American Institute of ...

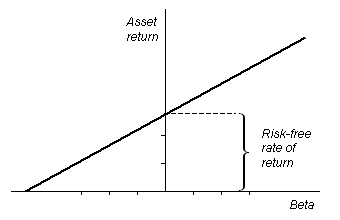

English: The offices of the American Institute of ... The Security Market Line, seen here in a graph, de...

The Security Market Line, seen here in a graph, de...Conversely, if earnings are growing faster than dividends, the payout rate will converge towards zero.

In summary, the Dividend Growth Model works well for those companies growing at a rate equal to or lower than that of the economy and have an established and stable dividend payout.

In order to estimate the cost of equity using the Dividend Growth Model, we simply adjust the model's equation for estimating the price of a stock, given as such:P = D1 / (r - g)Where P = the price of the stockD1 = the expected Dividend in one yearr = the required rate of returng = the expected Growth ConstantBy solving the equation for k we get the following:P(r - g) = D1r - g = D1 / Pr = (D1 / P) + gTherefore in order to estimate the cost of equity...