INTRODUCTION

Financial markets characterise by many entities that interact and affect each other in the trading process. In this context, there are two different approaches to stocks pricing: efficient markets (EM) and noise trading (NT). Each approach implements different scenarios that lead to different results. The aim of this paper is to look at these two different approaches and to compare and contrast between criteria that shape each approach. The first and second sections discuss the EM and NT approaches, respectively, whilst the third section compare and contrast between these two different approaches based on criteria such as investors behavior and risks involve.

EFFICIENT MARKETS APPROACH.

Shleifer (2000) defines an efficient market (EM) as "one in which security prices always fully reflects the available information" (p. 1). A prerequisite for this strong version of the approach is that information and trading costs are always zero (Fama, 1991).

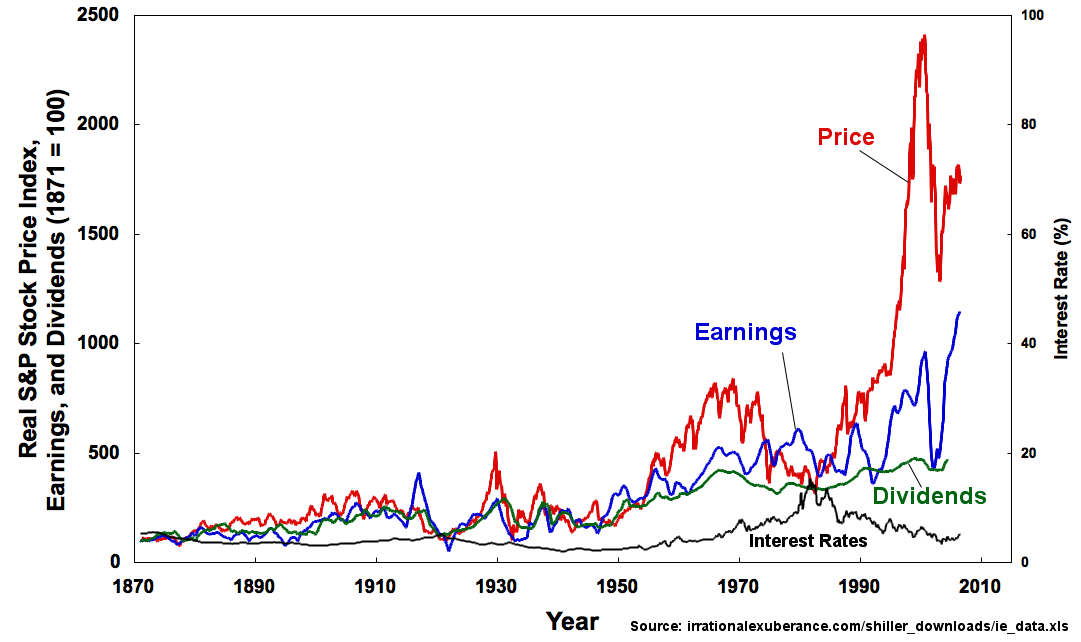

Plot of S&P Composite Real Price Index, Earnings, ...

Plot of S&P Composite Real Price Index, Earnings, ... summer!

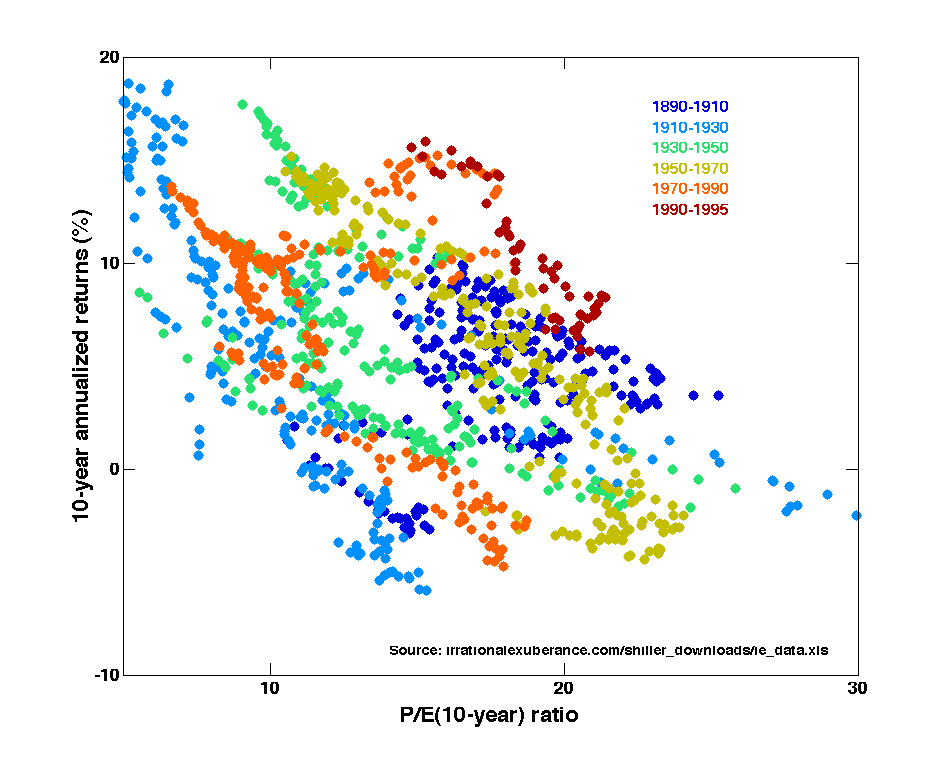

summer! ten-year returns

ten-year returnsA weaker and more rational edition of the EM approach sates that "prices reflect information to the point where the marginal benefits of acting on information do not exceed the marginal costs" (Fama, 1991). Therefore, the approach implies that the price changes are independent of one another (Brealey & Myers, 1996).

Investors follow this approach named arbitrageurs, fully rational investors whose trading decisions are not subject to sentiment (Shleifer & Summers, 1990). According to Malkiel (1996), the EM approach relies on three main assumptions. First, the market is so efficient in a way that nobody can buy or sell quickly enough to benefit. Second, perfect pricing exists. The approach holds that stocks sell at the best estimates of their basic values. Thus uninformed investors buying at the existing prices are getting full value for their investment, whatever stocks they purchase. Third, the approach involves that nobody has power over...