CHAPTER TWO

PRESENTATION OF FINANCIAL STATEMENTS AND ACCOUNTING POLICIES

Learning Outcomes:

Understand about the first time adoption of SLFRS

Explain the purpose and composition of corporate financial statements;

Describe selection, application and changes in accounting policies of companies; and

Assess implications of accounting policy choices made by companies.

2.1 Introduction

LKAS-1 sets out overall requirements for the presentation of general purpose financial statements, prescribes guidelines for their structure, and lays out the minimum requirements for their content and disclosure.

2.2 Objectives of Financial Statements

The objective of financial statements is to provide useful information about the financial position financial performance and cash flows of an entity that is useful in making economic decisions. The objectives of LKAS-1 are to ensure comparability of presentation of that information with the entity's financial statements of previous periods and with the financial statements of other entities. Financial statements are prepared on a going concern basis, unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so.

financial statements, charts only for 5 years

financial statements, charts only for 5 years Graphique du bilan de la Wikimedia Foundation / Gr...

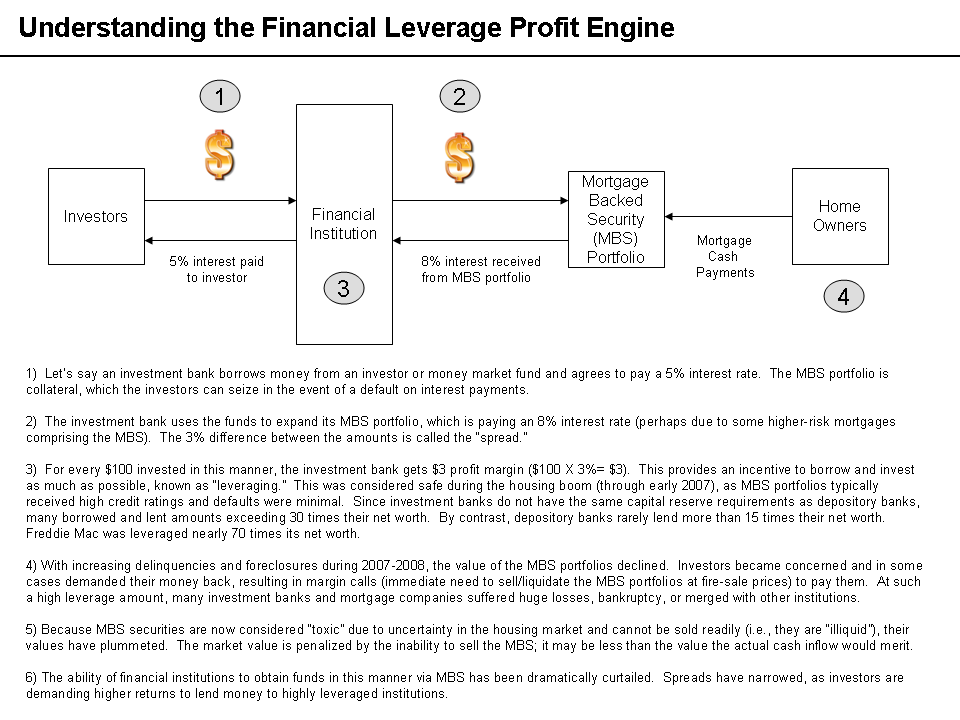

Graphique du bilan de la Wikimedia Foundation / Gr... Understanding Financial Leverage

Understanding Financial LeverageAn entity prepares its financial statements, except for cash flow information, under the

accrual basis of accounting.

Traditionally, a complete set of financial statements consist of a balance sheet, an income statement, a statement of changes in equity, a cash flow statement, and explanatory notes (including accounting policies). However, with the recent amendment to LKAS-1 some of the titles of the components of the financial statements have been changed. For instance, a balance sheet may now be referred to as a statement of financial position. Furthermore, the revised LKAS- 1 has also introduced a new statement, the statement of comprehensive income.

2.3 Complete Set of Financial Statements

The components of a complete set of financial statements are

A statement of financial position at the end of the...