Perfect competition is a market structure characterized by a large number of buyers and sellers of essentially the same product. The firms produce a standardized product and there is a free entry and exit of these firms to and from the industry. The firm in a purely competitive market faces a perfectly elastic demand curve at the price determined by equilibrium in the market (Hirschey 379).

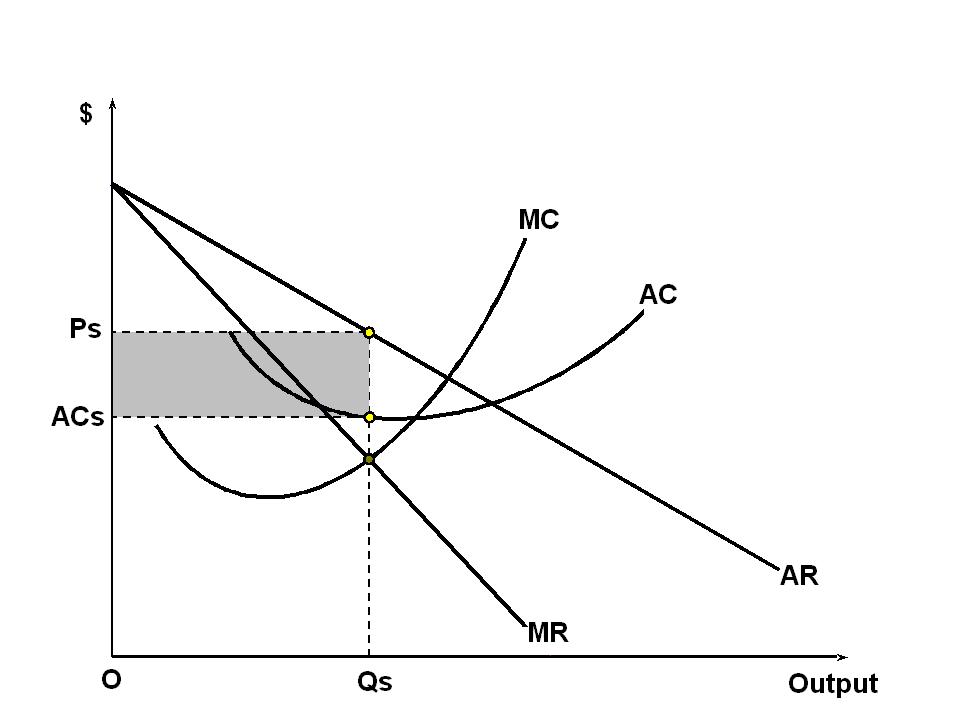

The firm in a short-run supply curve is the short-run marginal cost curve above the minimum point on the average variable cost curve, also known as the shutdown point. In the short run, firms behave differently than in the long-run. It is important to remember that a profit-maximizing firm always produces where marginal cost is equal to marginal revenue. When a firm is small relative to the market, and its product is indistinguishable from the product of other firms, the firm views itself as having no influence on the market price.

English: Short-run equilibrium of the firm under m...

English: Short-run equilibrium of the firm under m... Long-run average-cost curve with economies of scal...

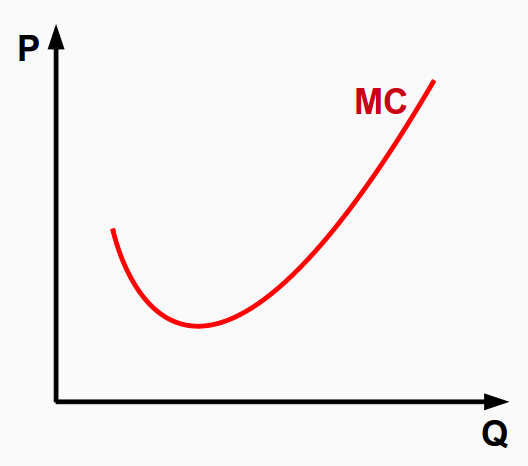

Long-run average-cost curve with economies of scal... English: marginal cost curve Polski: krzywa kosztu...

English: marginal cost curve Polski: krzywa kosztu...In perfect competition, if a firm wants to sell any of its output it must sell at the market price, which is referred to as a price taker.

When a market is in equilibrium, the purely competitive firm can sell as much of the product as it wishes. From the firm's viewpoint, this means it faces a perfectly elastic demand curve. As demand increases, the firm will move up its marginal cost curve. Another increase in market demand would cause the firm to move further up its marginal cost curve. The higher price would lead it to supply more output. However, by doing this the firm is suffering a loss which means factors could earn more in some other use. The opportunity costs are not being met. However, since this is the short run, that means that some factors are fixed. The fixed...