In a business combination, call it a merger, an acquisition takeover; we normally have the parent company, which becomes the entity after the combination. Accounting for this should be taken with caution because some considerations have to be considered.

According to (Pamela. A Smith 2007), the Fair value increment is accounted for and Goodwill should be determined and allocated. Fair value is the excess of fair value over the book value of the acquiree's identifiable net Assets. Goodwill is the amount paid by the acquirer in excess of the fair value of the identifiable net assets. For example if the purchase price =$400, the fair value of the identifiable net Assets =$320 the book value of Net Assets=$200; then the fair value increment=$120(320-200) and Goodwill=$80(400-320). Currently Accounting Standards are consistent with the parent view of the consolidated entity.

The parent view; The parent company consolidates 100% of the book value of the acquiree's net assets but only the parents percentage share of the fair value increment and good will.

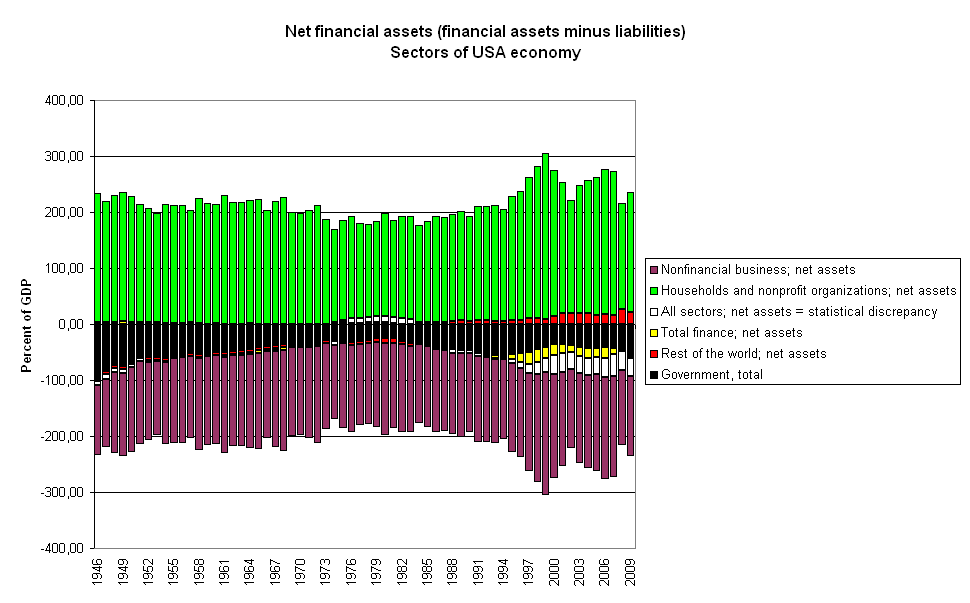

English: Net financial assets (financial assets mi...

English: Net financial assets (financial assets mi... Photo tentatively identified as the information de...

Photo tentatively identified as the information de... Exhibit, ''Home Economics in the New York State Co...

Exhibit, ''Home Economics in the New York State Co...The Non Controlling Interest (NCI) share of the acquiree's original book value with no fair value increment or goodwill allocation.

Very Important; The consolidated entity should recognize only the percentage of the Fair value increment and goodwill that was actually purchased by the acquirer.

SFAS 141 R , Proposes that accounting for business combination and subsequent consolidation follow the entity view under which the parent company consolidates 100% of the book value of the acquiree's net assets places 100% of the Fair value increment. Goodwill is accounted for and dived between the Holding Company and the subsidiary interest. Basically this view requires a full Fair value measurement of the goodwill associated with the Acquisition/merger.

Goodwill being the difference between the fair value of the acquiree as a whole and the fair...