Introduction

Since the early days of trade, man has struggled to secure equitable compensation for their goods. Value has always been determined by demand but the question remains, how do you equate a cask of wine with a number of furs or a bolt of fabric? These were issues early traders encountered. In most cases bartering worked for early traders. However, how do you get the goods you want if the other person doesn't want what you have to trade? The answer was money. Unfortunately, when currency came into being the same question arose, how and why should a handful of coins, beads, or seashells be accepted in exchange for goods? The solutions to these questions are addressed by the Gold Standard, which values currency, and the Foreign Exchange Markets which, provide a method for exchanging one form of currency for another.

Gold Standard

The following quote from the Federal Reserve Bank of Minneapolis accurately portrays how early currency came into existence,

Most early cultures traded precious metals.

Campaign poster showing William McKinley holding U...

Campaign poster showing William McKinley holding U... Gold Key, weighing one kilogram is used to access ...

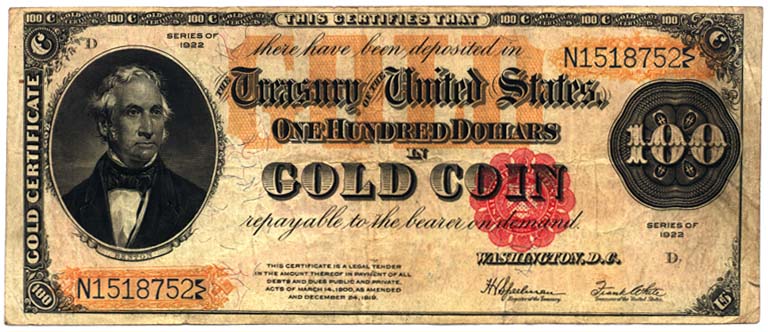

Gold Key, weighing one kilogram is used to access ... US gold certificate (1922)

US gold certificate (1922)In 2500 BC the Egyptians produced metal rings for use as money. By 700 BC, a group of seafaring people called the Lydians became the first in the Western world to make coins. The Lydians used coins to expand their vast trading empire. The Greeks and Romans continued the coining tradition and passed it on to later Western civilizations. Coins were appealing since they were durable, easy to carry and contained valuable metals (n.d.).

The Gold Standard was created in 1717 by Sir Isaac Newton (Ball, McCulloch, Frantz, Geringer, & Minor, 2006). Simply stated a country could not create currency unless it was supported by their gold reserves. Michael Bordo states,

The gold standard was a domestic standard, regulating the quantity and growth rate of a country's money supply. Because new...