TABLE OF CONTENTSABSTRACT1TABLE OF CONTENTS2LIST OF TABLES4LIST OF FIGURES5INTRODUCTION61. Types of Health Insurance Plans61.1 Indemnity (Fee for service)61.2 Managed Care71.2.1 Health Maintenance Organizations (HMO)71.2.1.1 Group Model HMO.81.2.1.2 Staff Model HMO.81.2.1.3 Network Model HMO.81.2.1.4 Individual Practice Association (IPA) HMO.91.2.2 Preferred Provider Organizations (PPO)91.2.3 Point of Service (POS)101.3 Consumer Choice Products101.3.1 Health Reimbursement Accounts (HRA)101.3.2 Medical Savings Accounts (MSA)111.3.3 Flexible Spending Accounts (FSA)111.4 Medicare Supplement Insurance (MSI)121.5 Long Term Care (LTC)121.5.1 Skilled Nursing Care131.5.2 Intermediate Nursing Care131.5.3 Custodial Care131.5.4 Home Care131.6 Disability Insurance141.7 Hospital-Surgical Policies151.8 Catastrophic and Specified Disease Coverage161.9 Hospital Indemnity162. Health Insurance in Turkey172.1 Health Institutions and Personnel in Turkey172.2 Provision of Health Services in Turkey183. Conclusion22REFERENCES23LIST OF TABLESTable 1: Numbers of in-patient and out-patient medical institutions17Table 2: Health payments of Government Employees Retirement Fund19Table 3: Health payments of Social Insurance Institution19Tablo 4: Total health expenditures in OECD countries as a ratio20Tablo 5: Total health expenditures in OECD countries as a % of GDP20LIST OF FIGURESFigure 1: Total expenditure on health as % of GDP in selected OECD countries and Turkey (2007)21INTRODUCTIONBefore approving a health insurance contract, the insurance company wants the individual to prove that he is insurable.

Health-Insurance-rates

Health-Insurance-rates California Health Insurance

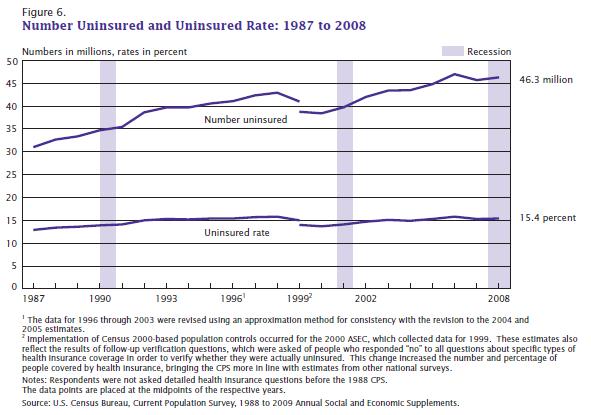

California Health Insurance English: This image depicts the numbers of uninsur...

English: This image depicts the numbers of uninsur...This process is usually called underwriting. In underwriting, the hazards that affect the probability of loss must be evaluated. After the individual is found appropriate for insurance, the cost of the policy should be set and this depends on several factors. The first and the most obvious factor is age. Annual claims generally increase with advancing age for all types of benefits. Gender is also of considerable significance in health insurance especially in disability income insurance. Females show higher disability rates than males up to the age 55 in most studies. The individual's medical history is also of concern. Past illnesses or accidents will probably increase the cost of policy. Also...