"Economics is the study of how human beings coordinate their wants and desires, given the decision-making mechanisms, social customs, and political realities of the society" (Colander, 2004, p. 3-4). There are two problems that face any economy on a given supply this is how much should be produce and who it should be produced for. This paper will summarize an article from Chevron, and the supply and demand on gas and why prices increase.

Throughout the years, the cost of gasoline has fluctuated greatly. Consumers have watched in awe as prices have plummeted down to less than a dollar a gallon and up to more than three dollars a gallon. In the wake of Hurricanes Katrina and Rita, the U.S has seen gas prices skyrocket. The greatest single factor that may contribute to the rise and fall of gas prices are fluctuating demands and competition within the oil industry.

Detailed analysis of changes in oil price from 197...

Detailed analysis of changes in oil price from 197... English: A sample of crude oil from Haenigsen, Ger...

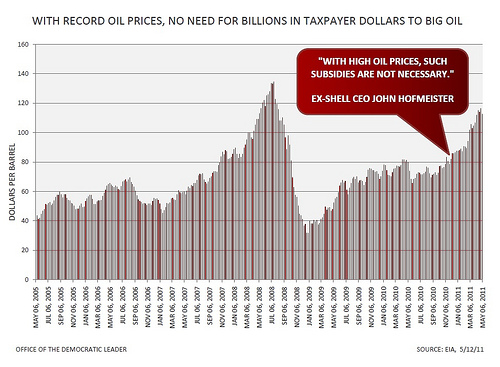

English: A sample of crude oil from Haenigsen, Ger... With Record Oil Prices, No Need For Billions In Ta...

With Record Oil Prices, No Need For Billions In Ta...Several factors will determine what causes the rise of gas prices. These can include natural disasters, or other factors. As stated by Chevron:

Crude oil prices have risen dramatically over the last year, driven by strong global demand, limited spare oil production capacity, continuing political instability in certain oil producing regions, and most recently reduced supply from the impact of hurricanes in the Gulf of Mexico (2005, p. 1).

During the hurricane, supply stations had to be shut down or were severely damaged by the storms. This caused a supply and demand problem within the United States. Individuals and families were evacuating the area and were in need of gas to get out of the affected areas. Due to the shut downs individuals across the country were panicking that there would not be enough gas and were heading to the pumps in droves. This caused an increase in demand when...