IntroductionAccounting system is developed into two form, financial accounting and management accounting. Both have different focuses and perspectives to facilitate different users' information need. This paper explores the issues for these two approaches: harmonisation of financial accounting and variability of management accounting. Finally, we discussed its implications for organisation's current or future shareholders.

Harmonisation of Financial AccountingFinancial accounting provides information to external users such as shareholders, creditors and regulatory agencies etc for making economic decision. Information has to be reliable, understandable and easily accessible for today's worldwide users. Harmonisation would allege to narrow national differences in accounting standard and, facilitates the comprehension and reliable comparison of financial reports from different countries (Rodrigues and Craig, 2007; Saudagaran and Diga, 1998). Multinational Companies (MNC) could reduce the compliance cost through avoiding preparing different sets of financial reports when listing on foreign capital markets (Rodrigues and Craig, 2007; S. Henderson et al., 2006; Saudagaran and Diga, 1998).

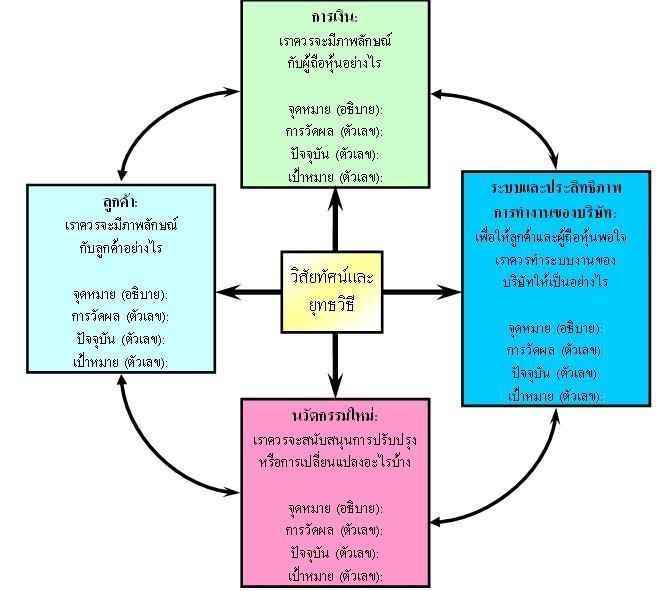

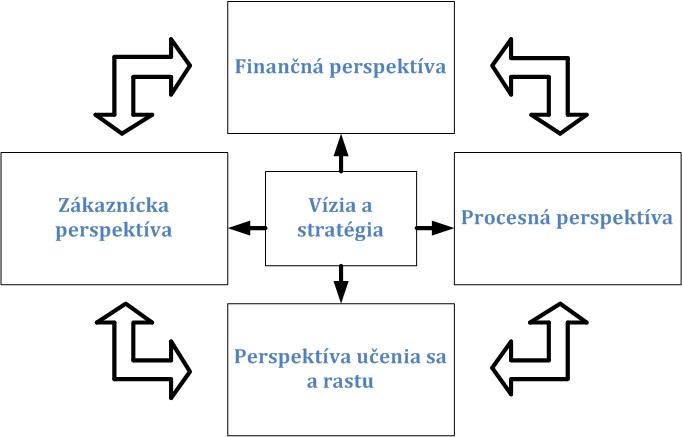

English: Example of a balanced scorecard strategy ...

English: Example of a balanced scorecard strategy ... Balanced scorecard

Balanced scorecard Slovenčina: Balanced scorecard podľa Kaplana a N...

Slovenčina: Balanced scorecard podľa Kaplana a N...The high quality is another benefit of International Accounting Standards (IAS). Saudagaran and Diga (1997) found that IAS are seems to be more flexible and neutral than most domestic financial accounting standards. Coopers and Lybrand (1995) concluded that IAS did not reveal materials differences on reconciliations of IAS to US GAAP. In addition, standardisation will avoid duplicative costs of national and international standards (Ampofo and Sellani, 2005). R&D costs associated with adopting IAS are minimal, as result cost savings for ASEAN in formulating relevant and acceptable financial accounting standards (Saudagaran and Diga, 1997). This also benefit to developing countries who unable to afford the cost of local GAAP.

However, social and cultural differences will provoke different readings and interpretations of IAS, which may lead to different accounting practices within a country (Rodrigues and Craig, 2007). The application of different accounting systems to a common set of...