1.

Marriott uses its' cost of capital estimates to create a hurdle rate to effectively run operations. Marriott uses these estimates to operate its four financial strategies. These are managing rather then owning hotel assets, investing in projects that increase shareholder value, optimizing the use of debt in the capital structure and repurchasing undervalued shares. If the company uses its overall WACC it may have divisions accept projects with returns below their respective WACC which will result in losses and vice versa.

2.

The Weighted Average Cost of Capital (WACC) is as average that reflects the expected return on all of a companies securities. For the WACC of Marriott as a whole represents tall of Marriott's divisions as one company. Marriott's divisions are lodging, restaurant and contract services. To calculate the WACC a risk free rate was used of 8.72% reflecting the interest rate on 10 year government bonds. A risk premium of 7.76%

English: Metropolitan Life Bldg., Manhattan, New Y...

English: Metropolitan Life Bldg., Manhattan, New Y... WACC (AM)

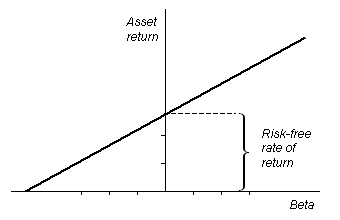

WACC (AM) The Security Market Line, seen here in a graph, de...

The Security Market Line, seen here in a graph, de...or the average returns of arithmetic averages of all long term, high grade corporate bonds was used for the WACC. To unlever the equity beta of 1.11 for Marriott the current debt percentage of 41% was used as shown in their capital structure. The relevered beta was calculated using 60% debt from the target capital structure. Cost of debt was calculated by multiplying the cost of fixed rate debt by fraction of debt at the fixed rate and adding it to the cost of floating rate debt multiplied by fraction of debt at the floating rate. The WACD for Marriott is 9.29%. The WACC was calculated by taking the WACD and multiplying it by debt percentage of capital, 1 minus the tax rate and our expected return and adding it to cost of equity multiplied by equity percentage of capital. The WACC is 8.4% for Marriott...