CHAPTER 20

DEMAND AND SUPPLY ELASTICITY

I. Price Elasticity of Demand

A. Concept of Price Elasticity

The responsiveness or sensitivity of quantity

demanded to a change in price.

B. General Formula for Price Elasticity

Percentage change in quantity demanded

Percentage change in price

C. Mid-Points Formula

E/demand =

D. Interpreting the Elasticity Coefficient

A coefficient higher than 1 is elastic

" " lower " 1 is inelastic

" " exactly 1 is unitary

A negative coefficient implies that a lower

price results is lower quantities sold.

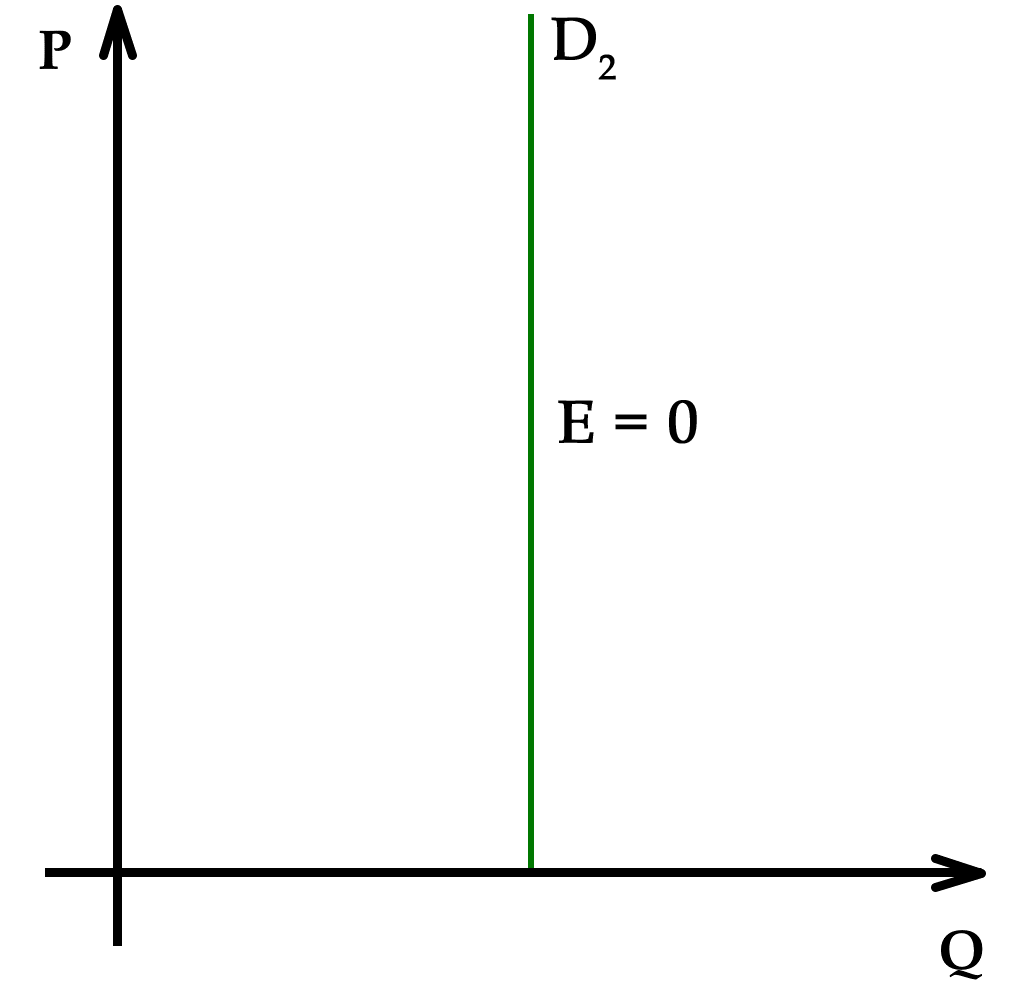

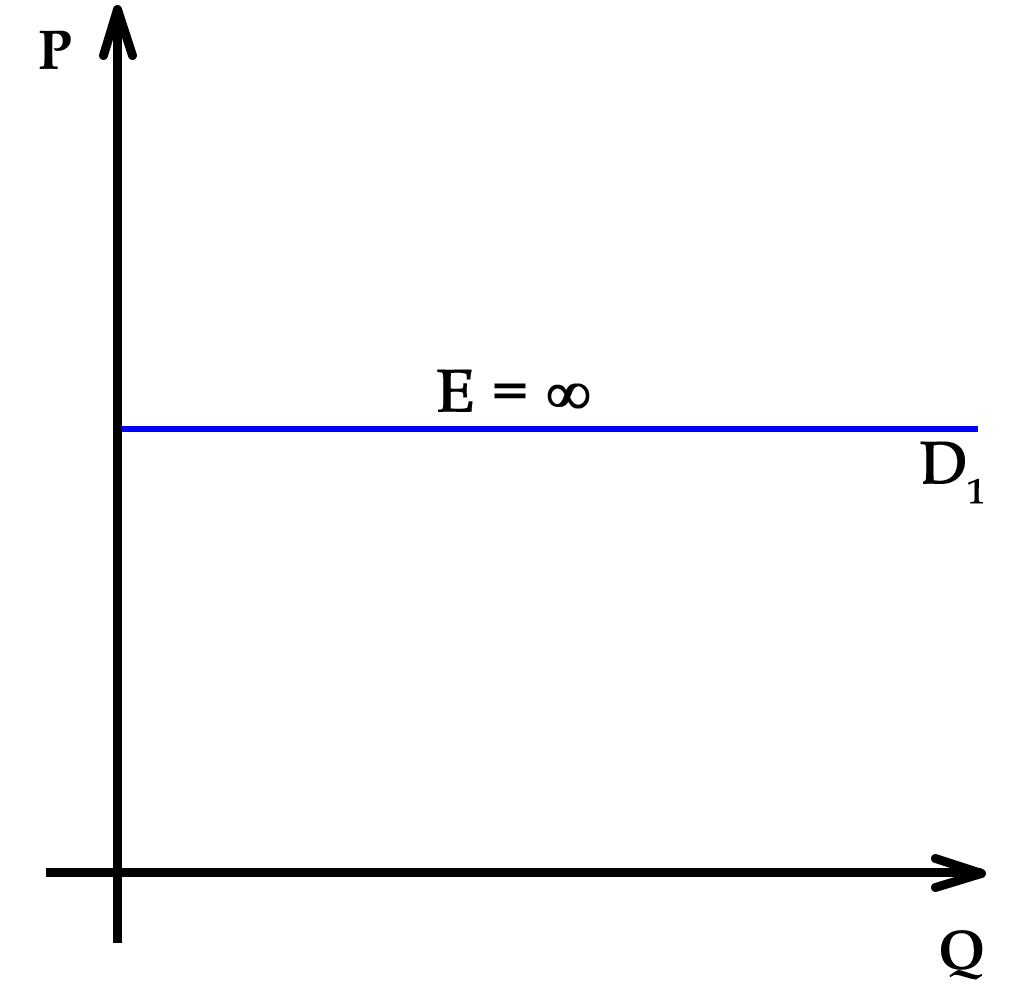

E. Extreme Elasticities

Perfectly Elastic Perfectly Inelastic

Demand or Supply Demand or Supply

II. Total Revenue Test

If Demand is Elastic If Demand is Inelastic

P TR P TR

P TR P TR

III. What Determines Price Elasticity

A. The number and quality of substitute goods.

B. The proportion of income the purchase makes up.

C. The size of the expenditure.

D. The time available for adjustments.

Perfectly inelastic demand

Perfectly inelastic demand Perfectly elastic demand

Perfectly elastic demand Graphical explanation of the total revenue test to...

Graphical explanation of the total revenue test to...E. Luxuries tend to be elastic.

F. Necessities tend to be inelastic.

G. Durable goods tend to be elastic. H. Promotion.

IV. Cross Elasticity of Demand

Shows whether two goods are substitutes or

complements.

Cross Elasticity Percentage Change in Q

Formula Percentage Change in P

If two goods are substitutes, the coefficient will be

positive.

If two goods are complements, the coefficient will be

negative.

V. Income Elasticity of Demand

Shows the responsiveness of certain goods to changes

in real consumer income.

Income Elasticity % Change in Q Demanded

Formula % Change in Real Income

Income-sensitive products have a coefficient higher

than 1.

The coefficient will vary according to income level.

VI. Elasticity of Supply

Shows the responsiveness of quantity supplied to a

change in price.

General Percentage Change in Q Supplied

Formula Percentage Change in Price

Determinants of Supply Elasticity

A. Short-Run Period (inelastic supply)

B. Long-Run Period (more elastic supply)

C. Market Period (short= inelastic; long= elastic)

VII. Applications of Price Elasticity of S and D

A. Wage bargaining (wage give-backs may save jobs if

the product is income-sensitive/ elastic)

B. Bumper crop in agriculture (will reduce the total

revenue of farmers, since products are inelastic.)

C. Automation (if the product is elastic, workers

displaced by automation, may be rehired)

D. Deregulation (works well on elastic goods)

E. Excise taxes, sin taxes (should be applied to

inelastic goods in order to enhance tax revenue)

CHAPTER 21

THE FINANCIAL ENVIRONMENT OF BUSINESS

I. The Legal Organization of Firms

A. Single Proprietorships (over 13 million, 74.3%)

Advantages:

1. Easy to organize

2. The owner is his own boss

3. All profits go to the owner

Disadvantages:

1. Unlimited liability

2. Limited financial resources

3. Owner is responsible for all decisions

B. Partnerships (1.7 million, 7.1%)

Advantages:

1. Easy to organize.

2. Easier to raise capital.

3. More specialization in management.

Disadvantages:

1. Unlimited liability

2. Each partner is responsible for the actions

of all other partners.

3. Division of authority leads to discord

4. The withdrawal of one partner ends the

business.

C. Corporations (over 3 million, 18.6%)

Definition: An artificial person, invisible,

intangible, and existing only in the eyes of the law.

Advantages:

1. Limited liability of stockholders.

2. The ability to raise capital by selling stock.

3. Larger size permits specialization, efficiency

4. Continuity of life ensured.

5. Separation of ownership and control.

Disadvantages:

1. Legally more complex.

2. Principal-agent problem.

3. Double taxation of corporate profits.

II. Methods of Corporate Financing

A. Share of Stock (ownership)

Legal claim to a share of the firm's future profits.

Common stock entails voting rights.

Preferred stock gives preferential treatment in the

payment of dividends. (no voting rights)

Stocks have no maturity dates.

Stockholders have a claim on the company's assets

only after all creditors had been paid off.

B. Bonds (corporate debt)

Interest must be paid on time.

Bondholders have no voice in management.

Bonds have a maturity date.

Claims of bondholders are satisfied before stock-

holders.

C. Secondary Market

Market for previously issued stocks and bonds.

D. The Stock Market

1. Random Walk Theory -future stock prices are

unpredictable.

2. Inside Information (illegal to use)

3. Price/ Earnings Ratio

Price of stock divided by earnings per share

4. Yield (%): Dividend per year divided by the

price of stock.

5. Dividend: dollars paid per share

E. Global Capital Markets

III. Problems in Corporate Governance

A. Separation of Ownership and Control

B. Asymmetric Information: Unequal sharing of

information.

C. Adverse Selection: The worst credit risks are the

ones likely to seek loans.

D. Moral Hazard: borrowers are likely to engage in

risky behavior resulting in default.

E. Incentive-Compatible Contract: pledging part of

corporate assets as collateral.

CHAPTER 22

COST AND OUTPUT DETERMINATION

I. Costs of Production

A. Explicit Costs (contractual costs)

Payments to outsiders for labor, materials, fuel,

transportation, rent, etc.

B. Implicit Costs

The cost of self-employed, self-owned resources,

such as the value of one's labor in its best alterna-

tive use.

C. Normal Rate of Return

The going rate to be paid to the investor for

employing his resource. (A cost of production)

D. Opportunity Cost of Capital

The income a resource would generate in its best

alternative use.

II. Profits

A. Normal Profit (Normal Rate of Return)

The minimum payment required to keep the

entrepreneur in business.

B. Economic/ Pure Profit (Not a cost of production)

Profits in excess or Normal Profit. (Total Reve-

nues minus Opportunity Cost of All Inputs)

C. Accounting Profit

Total Revenue minus Explicit Cost

D. Total Profit (Total Revenue minus Total Cost)

III. Types of Costs

TFC = Total Fixed Cost (overhead) It must be paid

even if output is zero. Examples: debt servicing,

depreciation, mortgage, property taxes, insurance.

TVC = Total Variable Cost. This cost changes with

output. Examples: labor, energy, raw materials.

TC = Total Cost (TFC + TVC)

MC = Marginal Cost. The increase in total cost

resulting from the production of an additional

unit of output. MC =

When Marginal Product is rising, MC is falling.

AFC = Average Fixed Cost AFC =

AVC = Average Variable Cost AVC =

ATC = Average Total Cost ATC =

or AFC + AVC

IV. Types of Products

TP = Total Product (output or Quantity Produced)

MP = Marginal Product. The increase in TP resulting

from the use of an addition unit of labor input.

The point where MP begins to fall is the Point

of Diminishing Returns.

AP = Average Product. Total Product divided by

Labor Input.

V. Types of Revenues

TR = Total Revenue (Output times Average Revenue)

MR = Marginal Revenue. The increase in TR upon

selling an additional unit of output. MR =

AR = Average Revenue. Total Revenue divided by

output sold. AR =

VII. Short vs. Long Run

A. Short Run Period. At least one factor of production,

usually capital, is fixed. Fixed costs exist only in

the short run.

B. Long Run. All costs are variable in the long run.

Plant size and all inputs can be varied.

VIII. Relationship between Average and Marginal

Costs The Marginal Cost curve always intersects the

ATC and AVC curves at their lowest points

IX. Long Run Cost Curves

A. Falling LR-ATC

B. Constant LR-ATC

C. Rising LR-ATC

D. Minimum Efficient Scale

The output range in which LR-ATC remains at

a minimum

E. Planning Horizon in the Long Run

CHAPTER 23

PERFECT COMPETITION

I. Characteristics

A. A large number of buyers and sellers.

B. Homogeneous/ standardized product

C. Free entry in/ exit from industry

D. Producers have no control over price.

E. Information is freely available to both buyers

and sellers

F. No non-price competition (No advertising)

G. No government intervention.

H. Example: agriculture

II. Demand Curve of the Perfectly Competitive

Producer

The D curve is perfectly elastic. Reason: each produ-

cer is too small to make an impact on industry supply.

Industry D curve is down-sloping.

The Average Revenue and Marginal Revenue Curves

are the same.

III. Profit Maximization in the Short Run

A. Total Revenue - Total Cost Approach

B. Marginal Revenue - Marginal Cost Approach

IV. The Short-Run Break-Even Point

The point where Average Total Cost = Price

V. Operating While Suffering Losses

Price is between Average Total Cost and AVC

VI. Short Run Shut-Down Price

The point where price drops below AVC

VII. Short Run Supply Curve of the Perfectly

Competitive Producer

That portion of the MC curve which rises above the

Average Variable Cost Curve.

VIII. Short Run Industry Supply Curve

The sum of quantities produced by all suppliers in

the short run.

IX. Long Run Industry Supply Curve

Reflects adjustments in the market supply after the

entry or exit of efficient/ inefficient producers.

X. Long Run Equilibrium

The output level at which

MR = MC = LRATC = SRATC

Marginal Cost Pricing = The opportunity cost of

production equals Marginal Cost. (There is no pure

profit, only normal profit)

CHAPTER 24.

MONOPOLY

I. Characteristics

A. A single producer/ seller

B. No close substitutes for the product.

C. Sole control over price (price-maker)

D. Sole control over market supply.

E. Blocked entry

F. Goodwill advertising

G. Government control

H. Examples: public utilities, Intel (?); US

Postal Service

II. Barriers to Entry

A. Economies of scale

B. Cost of capital

C. Patent rights

D. Cost of research

E. Exclusive franchises

F. Control over raw materials.

G. Economic and political muscle

H. Exclusive distributorships, fair trade pricing

I. Tariffs and other government protection

III. The Monopolist's Demand Curve

As volume produced increases, market price

falls. The falling price is the monopolist's

Average Revenue (AR = D) curve. Marginal

Revenue (MR) will be even more sharply down-

ward sloping:

Output AR (price) TR MR

1 $ 7 7 7

2 6 12 5

3 5 15 3

4 4 16 1

5 3 15 -1

6 2 12 -3

IV. Profit Maximization under Pure Monopoly

Profit is maximized at the point where Marginal

Revenue (MR) equals Marginal Cost (MC)

V. Pricing Behavior of Monopolists

A. The monopolist does not charge the highest

possible price. Objective: highest total profit.

B. Monopolists may suffer losses.

C. Monopolists prefer to produce in the elastic

portion of the demand curve which is approp-

riate for price cuts to maximize total revenue.

D. Limiting profits to discourage rivals.

VI. Price Discrimination

The product is sold at different prices to

different buyers. Prices are not justified by

cost differences.

Conditions for Price Discrimination

A. Downsloping Demand Curve

B. Separation of market/ segregation of buyers

can be achieved at a reasonable cost.

C. Buyers must have different elasticities of

demand.

D. The firm must be able to prevent the resale

of the product.

E. Examples: peak-time energy/ telephone use;

postal service, airlines, train service, theaters

VII. The Economic/ Social Cost of Monopolies

A. A lower quantity sold at a higher price.

B. Contributes to unequal income distribution.

C. Large profits enable more research and more

rapid technological growth.

D. Greater efficiency due to mass production.

E. The creation of giant multinational corpora-

tions transcending national boundaries.

CHAPTER 25.

MONOPOLISTIC COMPETITION

OLIGOPOLY

I. Monopolistic Competition

A. CHARACTERISTICS

1. A large number of producers/ sellers.

Small market share. Independence.

2. A highly competitive market.

3. Product differentiation.

4. Some limited control over price.

5. Advertising and other non-price

competition.

6. Brand allegiance.

7. Easy entry/ exit.

8. Examples: small grocery stores, clothing

stores, gas stations, restaurants.

B. PRICE AND OUTPUT DETERMINATION

1. The Demand curve and the Marginal

Revenue curve are mildly downsloping.

2. Profit maximization/ loss minimization

occurs where MR = MC

3. Short Run Equilibrium occurs where

ATC = Demand (AR) (Zero econ. profit)

4. Note that MR is below Price (AR) at the

Short Run Equilibrium.

C. MONOPOLISTIC VS. PERFECT

COMPETITION

1. Both earn zero economic profit in the

long run.

2. Under perfect comp. P = MC

Under monopolistic comp. P > MC

3. ATC is higher and output is lower

under monopolistic competition,

resulting in underallocation of resources

4. Economic Efficiency: P = MC = ATC

Correct Resource Allocation: P = MC

Most Efficient Technology: P = ATC

D. PROS AND CONS OF ADVERTISING

Pros

1. Adds 2% to the GDP

2. Promotes product differentiation and

competition.

3. Finances the media.

4. Stimulates product development.

5. Provides information about new products.

6. Promotes employment.

7. Diminishes monopoly power.

Cons

1. Competitive advertising is persuasive,

not informative.

2. Diverts resources from the economy.

3. Results in higher product prices.

4. Self-canceling in nature.

5. Inconvenient to the public.

6. It may contribute to monopoly power.

(High cost may be a barrier to entry)

7. Advertising may reduce efficiency.

II. Oligopoly

A. CHARACTERISTICS

1. A handful of producers/ sellers

2. Pricing interdependence

3. Heavy promotion/ nonprice competition

4. Difficult but sometimes easy entry

5. Anti-trust regulation

6. Collusion or price competition

7. Differentiated or standardized products

8. Examples: tobacco, car, tire, cereal,

camera, computer, steel industry

B. RESULT OF INTERDEPENDENCE

1. The reaction of rivals is unpredictable

2. The Demand and Marginal Revenue

curves are difficult to estimate

3. Prices tend to be inflexible (sticky)

4. Prices are changed in unison

C. OLIGOPOLY MERGERS

1. Horizontal merger (firms producing

similar products in the same industry)

2. Vertical merger (buying up one's supp-

liers or customers in the same industry)

3. Conglomerate merger (buying up unre-

lated companies in other industries)

D. MEASURING CONCENTRATION

Concentration Ratio: market share of the

top four companies in an industry

E. COLLUSIVE OLIGOPOLY

Due to price-fixing and limits on quantity,

it has the same effect as monopoly.

(see market demand curve for monopoly)

1. Cartels (illegal in the US)

Formal written agreement to fix prices and

limit output. OPEC.

2. Obstacles to collusion

-Demand and cost differences (MR = MC

points do not coincide with output allowed)

-Number of firms and their sizes

-Cheating (secret price concessions)

-Recession (excess capacity, declining profits)

-Legal obstacles (anti-trust action)

3. Price leadership (tacit collusion)

F. GAME THEORY

An analysis of alternative outcomes from

various interactive patterns of the participants

Cooperative game = players collude to improve

their position/ make themselves better off

Noncooperative game = no collusion

Zero sum game = gains offset losses

Negative-sum game = players as a group lose

Positive-sum game = players as a group gain

Example: prisoners' dilemma

G. KINKED DEMAND CURVE UNDER

NON-COLLUSIVE OLIGOPOLY

Rivals ignore a price increase but match a price

cut. This creates a break in the MR curve, and

causes a king (steeper decline) in the D curve:

H. ECONOMIC IMPACT OF OLIGOPOLY

1. Smaller quantity at a higher price (maybe)

2. Poor allocation of resources.

3. Income inequality

4. Technological advance

5. Influence on legislation/ government

CHAPTER 26.

REGULATION AND ANTI-TRUST POLICY

I. Types of Regulation

A. SOCIAL REGULATION

Deals with conditions under which goods and

services are produced. Main concern: the impact

of production on society and the physical charac-

teristics of goods. (Consumer Products Safety

Commission, Occupational Safety and Health

Administration, EPA, Equal Employment Oppor-

tunity Commission)

B. INDUSTRIAL REGULATION

Deals with the overall performance of selected

industries. Objective: to maintain competition; to

approve/ scrutinize mergers, etc. (FCC, FTC)

C. PRICE REGULATION

1. Cost of Service: no monopoly profits allowed.

2. Rate of Return: normal/ competitive profits

allowed.

II. Behavior of Regulated Industries

A. CREATIVE RESPONSE

Complying with the letter but not the spirit of the

law.

B. CAPTURE HYPOTHESIS

Regulated industries impose their will upon the

regulatory agencies.

C. SHARE THE GAINS, SHARE THE PAINS

Regulators must take into account the interest of

three groups: the legislators, the regulated indust-

ries, and the consumers.

III. Cost of Regulation

The total cost of government regulation is

estimated to exceed $600 billion annually, about

8% of the nation's income.

IV. Deregulation

A. Short Run Effects

1. Monopoly profits may disappear

2. Loss of employment and income

3. Level of service may decline

4. Some companies may go bankrupt

These negative effects may be offset in the long

run by lower prices due to increased competition.

B. Theory of Contestable Markets

Competitive conditions may exist even if there are

only a few producers in an industry. A market is

contestable if there is easy entry/ exit.

V. Federal Anti-Trust Laws

A. THE SHERMAN ACT OF 1890

No firm, state, or individual may conspire to

restrain trade or monopolize. (Poor enforcement)

B. THE CLAYTON ACT OF 1914

1. outlaws price discrimination

2. forbids tying contracts

3. prohibits the purchase of competitors' stocks

4. prohibits interlocking directorates

C. FEDERAL TRADE COMMISSION ACT (1914)

1. Public hearings to investigate unfair competi-

tion. "Cease and desist" orders.

2. Establishment of the FTC

3. Amended in 1938: the Wheeler-Lea Act

directed against deceptive advertising.

D. ROBINSON-PATMAN ACT (1936)

Directed against discriminatory pricing, discounts

or other concessions designed to lessen competit.

E. CELLER-KEFAUVER ACT (1950)

Eliminated a loophole under the Clayton Act:

firms could no longer purchase the physical

assets of competing firms, in addition to stocks.

VI. Exemptions from Antitrust Laws

Some exemptions include labor unions, public

utilities, professional baseball, hospitals, public

transit authorities, military suppliers

VII. Enforcement of Antitrust Laws

Market share test: a market share of 70% or

more constitutes monopoly as a rule of thumb,

but a smaller percentage may qualify based on

the existence of substitutes (tea/ coffee) and

geographic boundaries.

CHAPTER 27.

LABOR DEMAND AND SUPPLY

I. Reasons for Studying Labor Costs

A. They comprise a high percentage of total cost.

B. They ration labor to various industries.

C. They determine the combination of labor and other

resources to be used.

D. They determine personal income distribution, the

ratio between profits and wages, and the incomes

of various professions.

II. Marginal Physical Product of Labor

A. Demand for labor is derived from demand for the

product or service it produces.

B. Marginal Physical Product refers to the change in

output resulting from the use of an additional unit

labor.

C. The Marginal Physical Product declines because of

the Law of Increasing Marginal Costs.

III. Marginal Revenue Product of Labor

A. Marginal Revenue Product = The increase in total

revenue generated by an additional unit of labor

Marginal Physical Product x Marginal Revenue

(MRP = MPP times MR)

B. Marginal Factor Cost = The cost of employing and

additional unit of labor. Under a perfectly compe-

titive labor market, MFC equals the wage rate.

Labor Marginal Total

Input Output Phys. Prod. Price Revenue MRP MFC

1 10 10 3 30 30 12

2 18 8 3 54 24 12

3 24 6 3 72 18 12

4 28 4 3 84 12 = 12

5 30 2 3 90 6 12

Rule for resource employment: the point where

Marginal Revenue Product equals Marginal Resource

Cost

The Marginal Revenue Product Curve is the

Labor Demand Curve of the firm.

IV. What Determines the Elasticity of Labor Demand

A. The rate of decline in the Marginal Physical Prod.

(If MPP declines slowly, MRP also declines

slowly, and the Labor Demand Curve is elastic)

B. Elasticity of Product Demand. (If demand for the

product is elastic, Labor Demand is elastic, too)

C. The ease of resource substitutability. (The more

substitutes exist for the product, the greater the

elasticity of demand for labor)

D. Labor Cost-Total Cost Ratio. (The greater the

share of labor in total cost, the greater the elas-

ticity of demand for labor)

V. Wage Determination under Imperfect Competition

Under imperfect competition the product price falls

and wage rate increases with rising output. As a result,

MRP falls, and MFC increases: Wage

Labor Output MPP Price TR MRP Wage Cost MFC

1 10 10 3 30 30 4 4 4

2 18 8 2.75 49.5 19.5 6 12 8

3 24 6 2.50 60 10.5 7.5 22.5 10.5

4 28 4 2.25 63 3 10 40 17.5

5 30 2 2 60 -3 12 60 20

The equilibrium wage rate is determined by the point of

intersection between the MRP and the MFC curves. This

shows that the company will hire three units of labor at

a wage rate of $10.50, and output will be set at 24 units.

VI. What May Change the Demand for Labor?

A. Demand for the product labor produces.

B. Changes in productivity which may be due to

1. better technology

2. higher quality of labor or management

3. change in the combination of labor and capital

C. Market demand for labor = the sum total of each

firm's labor demand curve in the industry.

D. The type of competition that exists in the industry.

(Monopolists hire fewer workers than competitive

firms)

VII. Wage Issues

A. The real minimum wage is directly related to teen-

age unemployment.

B. Efficiency wage: a higher than competitive wage

rate which tends to ensure lower labor turnover

and higher labor productivity.

C. Insider-outsider theory: workers holding jobs at an

enterprise try to keep out any outsiders who might

be willing to work for less.

VIII. What Determines Labor Supply?

A. Wage rate changes in other industries.

B. Changes in working conditions.

C. Job flexibility and job sharing.

IX. The Optimum Combination of Resources

A. The Profit Maximizing Rule

1. Under Perfect Competition

MRP of Labor MRP of Capital

Price of Labor Price of Capital

2. Under Imperfect Competition

MPP of Labor MPP of Capital

MFC of Labor MFC of Capital

B. Least Cost Rule

The firm will hire resources up to the point where

the MPP of the last dollar spent is the same for

each resource:

MPP of Labor MPP of Capital

Price of Labor Price of Captial

(Cost per unit of service)

CHAPTER 28.

UNIONISM AND LABOR LAWS

I. Types of Unions

A. CRAFT UNIONS

They are composed of skilled craftsmen of given

trade or vocation.

They maximize their income by limiting member-

ship through

- examinations and occupational licensing

- initiation fees, long apprenticeship period

- legislation to require the use of union labor

- restriction on interstate movement

Examples: plumbers, electricians, carpenters

B. INDUSTRIAL UNIONS

They maximize power by including all workers of

an industry. They have a social/ economic agenda.

Objectives: political influence, power to workers,

social change, influencing government actions.

Examples: Teamsters, United Mine Worker, UAW

(Congress of Industrial Organizations -CIO)

II. Collective Bargaining

Negotiation between management and union

leaders to achieve a mutually acceptable labor

contract.

III. History of Unionism

A. REPRESSION PHASE (1790-1932)

1. Criminal conspiracy doctrine

2. Injunction - court order against strikes/ pickets

3. Blacklisting, discharge for union activity

4. Lockout - shutting down business for weeks

5. Hiring strikebreakers (scabs)

6. Yellow dog contract (promise not to join union)

7. Paternal/ company unions (run by management)

B. ENCOURAGEMENT PHASE (1932-1947)

1. Norris-Laugardia Act (1932)

Eliminated injunctions/ yellow dog contracts

2. Wagner Act (1935) National Labor Relations

Act. Established the NLRB

Gave workers the right to strike without penalty

and to engage in collective bargaining.

C. INTERVENTION PHASE (1947- Present)

1. Taft-Hartley Act (1947) Key provisions:

a. Eliminated unfair union practices:

- coercion to join

- jurisdictional strikes (fight over which union

should perform a job)

- secondary boycotts (refusal to buy the products

of competing unions)

- sympathy strikes (in support of other unions)

- large initiation fees

- featherbedding

b. Regulated union contracts:

- required financial reports to the NLRB

- regulated political contributions

- required non-communist affidavits

c. Regulated contract content

- outlawed closed shop

- check-off had to be authorized by workers

- separated welfare and pension funds

- introduced reopening clauses

- introduced the 80-day cooling-off period

2. Landrum-Griffin Act (1959)

Regulated the election of union officers.

IV. Business Unionism

The American Federation of Labor (AFL) created

in 1886. First president: Samuel Gompers. Principles:

A. Rejection of socialism

B. Objectives limited to better pay, shorter hours,

better working conditions, fringe benefits

C. Political neutrality - non-interference by gov't

D. Autonomy of craft unions within the AFL

V. Government Regulation

A. Right-to-Work Laws - make it illegal to require

union membership as a condition of employment

B. Union Shop - requires a promise from new workers

to join the union within 30 days (illegal in states

which have right-to-work laws)

VI. Union Goals

A. Setting wage above the market rate.

B. Providing employment for all members

C. Restricting labor supply

D. Increasing worker productivity

E. Increasing demand for union-made goods

VII. Benefits of Labor Unions

A. Promoting better working conditions; social

efficiency

B. Reduction of wage inequality

C. Reduction of monopoly profits

D. Giving political voice to workers. Influence on

legislation

E. Reduction of workplace friction through orderly

arbitration and grievance procedures

VIII. Monopsony Model

A single buyer for labor. Example: professional and

college sports.

Monopsony Model Bilateral Monopoly Model

IX. Bilateral Monopoly Model

A national labor union facing a monopsonist.

Example: The United Mine Workers against a

mining company which owns virtually all the

jobs in a town.

CHAPTER 29.

RENT, INTEREST, PROFIT

I. Rent

A. ECONOMIC RENT

Payment received for a resource over and above its

opportunity cost.

Additional land rent has no incentive function to

generate more land because the supply of land is

fixed (perfectly inelastic).

B. Function of economic rent: it allocates resources

their highest-valued use.

C. Economic rent to labor: income earned over and

above labor's second best alternative use.

Examples: movie stars, rock stars, sports heroes

II. Interest

A. Definition: price paid for the use of someone else's

money. (Borrower is actually buying time)

B. What determines the interest rate:

1. Length of loan.

2. Risk.

3. Size/ type of loan.

4. Handling charges.

5. Market imperfections.

6. Supply and demand of loanable funds

C. Case study: Rent-to-own stores

D. Equilibrium Interest Rate:

E. Nominal vs. Real Rate of Interest

Nominal: stated interest rate in current dollars

Real: Nominal minus Anticipated Inflation

F. Allocative Role of Interest

Interest allocates loanable funds to their most

profitable uses.

G. Interest and Present/ Future Value

Present Value of Future Dollars: An amount

to be received in the future has a smaller value

today. (see table on p. 659)

An amount paid out today has a greater value

in the future.

III. Profits

A. Economic Profit

Total Revenue less Explicit + Implicit Costs

B. Accounting Profit

Total Revenue less Explicit Costs

C. Sources of Economic Profit

1. restricted entry of rivals

2. innovation, new ideas

3. risk taking (payment for uninsurable risks)

4. providing a service to society

5. giving employment opportunities to others

D. Functions of Economic Profit

1. profit encourages innovation/ investment

2. profit shows the direction the economy should

take

3. profit ensures the efficient allocation of

economic resources

CHAPTER 30.

INCOME, POVERTY, AND HEALTH CARE

I. Income

A. THE LORENZ CURVE

Shows the inequality in income distribution among

the five quintiles of the economy.

The 45-degree line represents perfect income

equality. The field between the curve and the 45-

degree line shows the inequality gap.

B. CRITICISMS OF THE LORENZ CURVE

1. it does not show income received in kind

2. it does not show differences in the size of

households

3. it does not account for the age differences

of families (older people tend to earn more)

4. it reflects income before taxes

5. it excludes all unreported income

C. CAUSES OF INCOME INEQUALITY

1. ability differences

2. education/ skill level

3. level of ambition

4. job tastes

5. willingness to take risks

6. property ownership

7. market power (legislation, inside info.)

8. luck, connections, discrimination

D. DISTRIBUTION OF WEALTH

Richest 1% owns 36% of all assets

Next 9% owns 31% of all assets

Richest 10% owns 67% of all assets

Remaining 90% holds 33% of all assets

E. DETERMINANTS OF INCOME DIFFERENCES

1. Age Earnings Cycle

The average person's income peaks at age 50

Intergenerational Mobility: income rises from

one year to the next.

2. Intragenerational Mobility

Successive generations earn more than their

forefathers

3. Marginal Productivity

With increasing skill and experience people

become more productive.

4. Investment in Human Capital

Treating education/ retraining as an investment

F. EGALITARIANISM vs. EFFICIENCY

Equality in income distribution would maximize

consumer satisfaction from the national income

but it would remove the incentive to work

Comparable worth doctrine: women should earn

the same wages as men if they hold the same job

and have the same skills as men.

II. Poverty

A. Poverty in the US and the world

The number of Americans officially below the

poverty line is about 37 million.

In 1996 the official poverty level for an urban

family of four was $16,000.

According to the UN, 1,300 million people live

in poverty worldwide.

B. Income Maintenance Programs

1. Social Security (OASDI = Old Age, Survivors'

and Disability Insurance) 90% of working men

are covered by Social Security in the US. At this

time about 50 million people receive benefits

averaging $713 per month.

2. Supplemental Security Income (SSI), Aid to

Families with Dependent Children (AFDC)

3. Food Stamps. The program has more than 28

million recipients at an annual cost of 30 billion.

4. Earned Income Tax Credit (EITC)

Provides benefits up to $2,528 for those with

incomes between $8,425 and $11,000. In Missi-

ssippi and DC nearly half the families are

eligible. Nationwide eligibility: 20%

III. Health Care

A. Health Care Spending

In 1965 health care costs were 6% of natl. income

In 2000 health care costs will be 15 % " "

B. Reason for High Costs

1. The top 5% of health care users incur 50% of

all costs.

2. The population is living longer. The top 5%

is made up of people 70 and older.

In 1996 12% of the population was over 65

In 2035 22% " " " will be over 65

3. Costly new technologies

4. Third-party financing tends to increase demand

for health care

5. Moral hazard. Role of the deductible.

6. Abuses by health care providers.

C. Dealing with Health Care Costs

1. National Health Insurance

Would the healthy subsidize the chronically ill?

2. Medical Savings Accounts

Tax exempt employee savings. It would relieve

employers from providing zero-deductible health

care services.

3. Employee could apply unused MSA's toward a

supplementary retirement plan.

4. Moral hazard (seeking medical care when unne-

cessary) would be reduced.

IV. Discussion on Welfare Reform

A. Do high welfare benefits reduce the incentive to

work?

B. Are government sponsored job training programs

effective in reducing dependence on welfare?

C. The "leaky bucket" theory of welfare.

D. Pro's and con's of the negative income tax.

Objectives:

1. to get people out of poverty

2. to provide incentives to work

3. costs should be reasonable

No plan can meet all goals some of which are

mutually exclusive.

E. Relationship between income distribution and

the overall efficiency of the economy.

F. What is net worth? What is the difference between

income and wealth?

G. How can we reform federal Medicare spending?

CHAPTER 31.

ENVIRONMENTAL ECONOMICS

I. Private vs. Social Costs

A. Private Costs (Internal Costs)

They are paid by the individuals/ firms that incur

them.

B. Social Costs

The sum total of private (internal) and external

costs imposed upon society.

II. Externalities

A. Definition

Externalities develop when private costs diverge

from social costs.

B. How to Correct for Externalities?

1. require the installation of pollution abatement

equipment

2. cut pollution-causing activity

3. pay an ongoing fee for pollutants emitted

4. create a market for pollution rights

5. apply punitive taxes against polluters

6. force polluters to pay for the cleanup

C. "Optimal" Quantity of Pollution

Point of intersection between the marginal cost and

marginal benefit of pollution abatement.

D. Problems of Assigning Responsibility for Pollution

1. Determining property rights

Private Property: exclusive ownership rights

Common Property: air, water, etc. owned by all,

therefore by none

2. Responsibility for pollution is easily assigned

when private property rights are involved. The

same is not true for common property.

3. Transaction Costs: costs associated with reach-

ing and enforcing agreements (pertaining to

pollution)

III. Recycling

A. Benefits and costs.

B. Is the world running out of scarce resources?

CHAPTER 32.

PUBLIC CHOICE:

THE ECONOMICS OF INTEREST GROUPS

I. Collective Decision Making

The manner in which voters, politicians, and interest

groups influence public choice. The Theory of Public

Choice is simply the study of collective decision-

making.

II. Differences between Private and Public Choice

A. Public goods are provided at no cost to the user

B. The gov't can use force to achieve its objectives

C. The political system is run by majority rule 51:49%

D. The private economy is run by proportional rule.

(Dollar votes express the intensity of a want)

III. The Iron Triangle

It is an alliance of bureaucrats, interest groups

(lobbies), and congressional committees which parti-

cipate in making public choices.

IV. Interest Groups

A. Distributional Coalitions

Special interests, unions, and professional organi-

zations representing their members. Their interest

is concentrated while the public interest is diffused.

B. Logrolling

Elected representatives exchange political favors

at public expense.

V. The Role of Bureaucrats and Politicians

A. Rational Ignorance

Voters prefer to delegate their vote to elected repre-

sentatives in order to minimize the time invested in

making public choices.

B. Paradox of Voting

People are unable to rank public choices that might

benefit them.

C. Median Voter Model

Politicians tend to gravitate toward the center to

ensure mass-appeal.

D. Nonselectivity

No single bundle of public goods fits the needs of

any single voter perfectly.

VI. Political Rent-Seeking

The use of private resources in an attempt to get

government benefits for special interest groups.

VII. The Farm Problem

A. History of the Farm Problem

1. 1900-1915 was the golden age of US agricult.

2. By 1960 farm income fell to 50% of non-farm

income

3. The proportion of US population living on farms

dropped from 43.8% (1880) to 1.8% today

B. Causes of the Farm Problem

1. Long-Run Causes

a. inelastic demand for farm products

b. rapid improvements in technology

c. lagging demand for farm products

d. immobility of resources

2. Short-Run Causes

a. fluctuations in output due to weather

b. fluctuations in domestic/ foreign demand

c. high fixed cost of equipment

C. Public Policy toward Farmers

1. The policy has been based upon the assumption

that the farm is the last remaining bastion of

perfect competition.

2. Price Supports (minimum guaranteed price) The

government buys up the surplus.

3. Price Subsidies (a price below equilibrium with

payments made to farmers as an offset)

4. Target Price (The use of deficiency payments to

guarantee the farmer the targeted price)

5. Parity Ratio

Prices received divided by Prices paid

The adjustment of farm income to increases in

the cost of living & operating a farm.

6. Surplus Controls

a. restricting supply (acreage rotation/ reserve)

b. new uses for farm products

c. giveaways (food stamps, school lunch, aid)

CHAPTER 33.

WORLD TRADE

I. The Importance of World Trade

A. Volume

Since 1950 the world's GDP has increased 6-fold

while the volume of trade has gone up 13-fold.

B. Dependence on Trade

In 1950 imports in the US added 4% to annual

income, today they add 12%. In other countries

import dependence is much greater.

II. Beneficial Effects of World Trade

A. Gains from trade increase living standards

B. Trade allows increasing use of worldwide speci-

alization (taking advantage of comparative

advantage)

C. Trade leads to a better allocation of the world's

resources

D. Product and resource prices move toward equality

III. Obstacles to Trade

A. Politics (embargo, tariffs, quotas)

B. Currency/ exchange rate differences

C. Pressures to achieve a trade surplus

D. Negative Terms of Trade (ToT= Export Prices

divided by Import Prices)

IV. Comparative Advantage

A. The ability to produce a good at a lower opportu-

nity cost than one's trading partners

B. Gains from trade through specialization

V. Exports and Imports

A. In the long run, imports are paid for by exports

B. Restrictions imposed on imports will eventually

result in lower exports

C. Dumping (selling below domestic price or pro-

duction cost)

VI. Arguments against Free Trade

A. Military self-sufficiency

B. Protection of domestic employm./ living standards

C. Infant industry argument

D. Diversification for stability

VII. Quotas

Limitation on the quantity to be imported

VIII. Tariffs

Import duties imposed on foreign goods

IX. GATT and the WTO

GATT (General Agreement on Tariffs and Trade),

established in 1947, and the WTO (World Trade

Organization), established in 1995 aim to reduce

tariffs and trade barriers worldwide.

CHAPTER 34

EXCHANGE RATES & BALANCE OF

PAYMENTS

I. Balance of Trade vs. Balance of Payments

A. Balance of Trade shows the difference between

exports and imports.

B. Balance of Payments is a summary of all economic

transactions with the rest of the world. It includes

trade, transportation, tourism, military spending,

interest and dividend income, sale of assets, sale

of gold, and currency exchange

II. Current Account Transactions

A. Merchandise Trade $ - 161 bill.

B. Export and Import of Services + 68 "

C. Unilateral Transfers - 30 "

Total: - 191 + 68 = - 123 bill

III. Capital Account

A. US Capital Going Abroad - 314.8

B. Foreign Capital Coming In + 431.5

C. Official Transactions + 6.3

+ 123 Bal: 0

IV. Official Reserve Account Transactions

A. Foreign Currency Exchange

B. Sale of Gold

C. Special Drawing Rights with the IMF

D. Reserve Status at the IMF

E. Holdings of the US Treasury

V. What Affects the Balance of Payments

A. Relative Rate of Inflation (higher inflation worsens

the balance of payments)

B. Political Stability (stability improves the balance)

VI. Exchange Rates

A. Flexible/ Floating Exchange Rate

The rate is determined by the supply and demand

of currencies.

B. Appreciation of a Currency

An increase in the value due to increasing demand

for the nation's goods in world trade

Curve: An increase in demand for German-made

goods means higher demand for German Marks,

and a higher dollar cost of the DM:

C. What Determines Exchange Rates

1. Interest Rates (Higher rate=stronger currency)

2. Productivity (Higher prod.=stronger currency)

3. Changes in Product Preferences

4. Economic/ Political Stability

5. Relative Income Changes

VII. The Gold Standard and the IMF

A. Pegged/ Fixed Exchange Rates

They were based upon the gold standard. From

1933 to 1971 the $ was pegged at $35/ oz of gold

B. The Bretton Woods System (1945)

Established the IMF to help nations deal with their

balance of payments problems. Nations had to

intervene to keep the value of their currencies

within 1% of declared par value.

C. Special Drawing Rights (SDR's) (1967)

The IMF allocates SDR's to member nations based

upon a quota system

D. Removal of the Dollar from the Gold Standard

After Dec. 18, 1971 the $ was no longer exchange-

able for gold.

E. Dirty/ Managed Float of the $ (1973)

Exchange rates are determined by the supply and

demand of currencies but central banks may inter-

vene to "support" a currency in order to imporve

their trade position.

CHAPTER 19

CONSUMER CHOICE

I. UTILITY THEORY

A. Utility = the want-satisfying power of a good or

service

B. Marginal Utility = The increase in total utility upon

the consumption of an additional good or service

C. Total Utility = Satisfaction derived from the con-

sumption of all units of a good or service

D. The Law of Diminishing Marginal Utility = The

more units of a good we consume, the less our

additional satisfaction

Example:

Quantity of Big Macs Marginal Total

Consumed Utility Utility

1 10 10

2 4 14

3 - 4 10

(Total Utility reaches its peak at the point where

Marginal Utility is zero)

E. Optimization of Consumer Satisfaction

The consumer's income should be allocated so that

the last dollar spent on each product purchased

should yield the same marginal utility:

Marginal Utility of A Marginal Utility of B

Price of A Price of B

Example:

Quant. A Price MU of MU/ P Quant. Price MU of MU/P

of A of A A of A of B of B B of B

1 $ 4 20 5 1 $ 3 12 4

2 4 8 2 2 3 9 3

3 4 4 1 3 3 3 1

The consumer should purchase three units of each product

in order to maximize satisfaction from a budget of $ 21.

The consumer will always buy that product first which

yields the highest MU per dollar.

II. Assumptions about Consumer Behavior

A. The consumer is rational in making choices

B. The consumer is fully aware of the products features

and the value of each feature to him

C. The consumer's budget is limited (budget restraint)

D. Prices ration the goods available (budget line)

E. Income Effect = A decline in the price of a product

means an indirect increase in real income.

F. Substitution Effect = If the price of a good falls, con-

sumers will buy more of it, and less of its substitutes

whose prices are unchanged.

III. Budget Line = Shows various combinations of two

products which can be purchased on a given income

IV. Indifference Curve = Shows all combinations of

products A and B which yield the same level of total

satisfaction to the consumer

V. Indifference Map = A series of indifference curves, each

showing a different level of total utility

VI. Consumer Optimum = The point where the highest

indifference curve is tangent to the budget line.

VII. Income-Consumption Curve = The line connecting

points of consumer optimum as income increases

VIII. Price-Consumption Curve = The line connecting

points of consumer optimum as the price of a good

changes