Cost centre - an identifiable part of an organisation for which costs can be calculated.

Examples include 'personnel', and IT. Departments which costs can be calculated do not create revenue and do not charge other departments for their services are included in this heading.

Profit centre - an identifiable part of an organisation for which costs & revenue (and therefore profit) can be calculated.

Examples include a branch of a chain of stores or a specific product. Sales are easy to calculate and it is possible to calculate costs and profit.

Why use cost/profit centres?:

- See which areas aren't achieving

- Set benchmarks

- Middle manages can make more decisions

To set up cost/profit centres it must be possible to:

- Split the business into sections/departments

- Identify people to be responsible for the different departments

- Set targets

- Review/monitor in stages

Disadvantages of cost + profit centres:

- Difficult to allocate costs

- Can cause extra stress + pressure

- Targets need to be achievable

- Cheaper to buy items in bulk (for whole company instead of per department)

A supplies department should be a cost centre for example, as it provides a service for the other departments at no cost and does not generate an income.

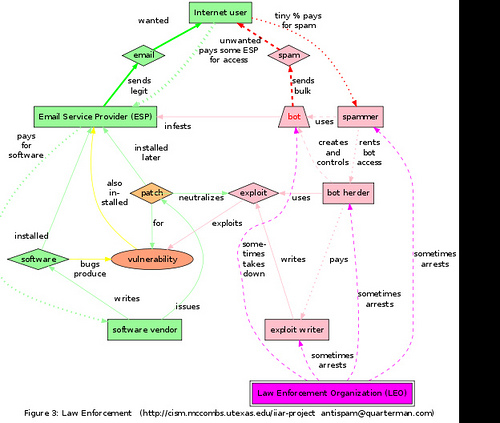

Figure 3: Law Enforcement (http://crism.mccombs.ut...

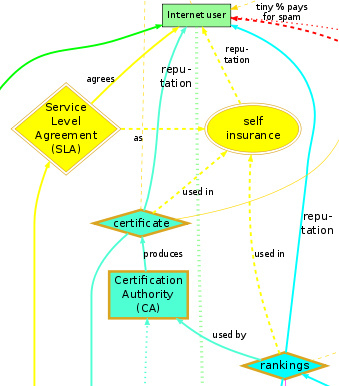

Figure 3: Law Enforcement (http://crism.mccombs.ut... Figure 7: SLAs as Self-Insurance (http://crism.mcc...

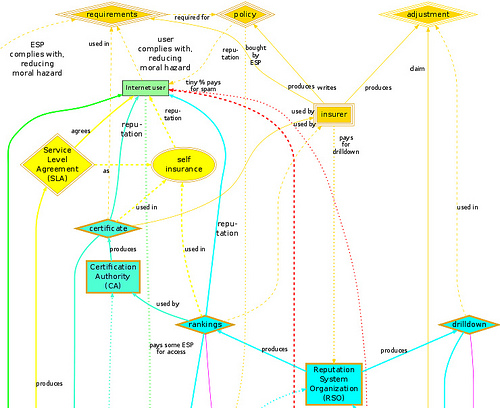

Figure 7: SLAs as Self-Insurance (http://crism.mcc... Figure 9: All the New Levels (http://crism.mccombs...

Figure 9: All the New Levels (http://crism.mccombs...A magazine section of a shop would be a profit centre as it's sole purpose is to generate income.

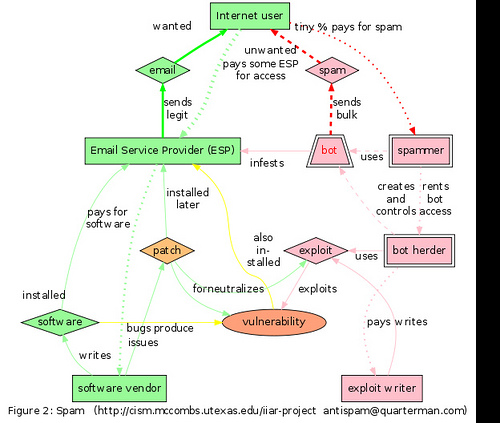

Figure 2: Spam (http://crism.mccombs.utexas.edu/ii...

Figure 2: Spam (http://crism.mccombs.utexas.edu/ii... Figure 5a: Most Spam Volume, ARIN, 8 Sep 2010 - 7 ...

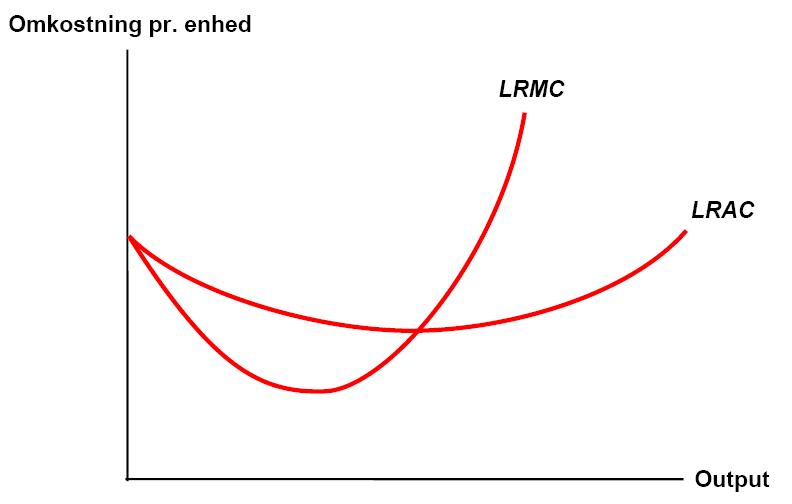

Figure 5a: Most Spam Volume, ARIN, 8 Sep 2010 - 7 ... Cost-Volume-Profit Analysis

Cost-Volume-Profit Analysis