Accounting Quick Study Assignment (Chapter 7) QS 7-1. What is the difference between the terms liquidity and cash equivalent? Answer. The liquidity of an asset refers to how quickly and easily, an asset can be converted into other types of assets or be used to buy services or satisfy obligations. Assets are evaluated in terms of their liquidity. Cash, being the most liquid and prepaid expenses, being the least liquid.

Conversely, cash equivalents are those assets, which are short-term, or temporary, investments that are highly liquid, that is, they can be instantly converted to cash. These assets even participate in increasing the company's return. Some examples are investments in treasury bills, commercial paper, and money market funds.

QS 7-2a. What is the main objective of internal control and how is it accomplished? Answer The main objective of a properly designed internal system is to promote operations and protect assets from waste, fraud, and theft.

SOMF Asset Patterns

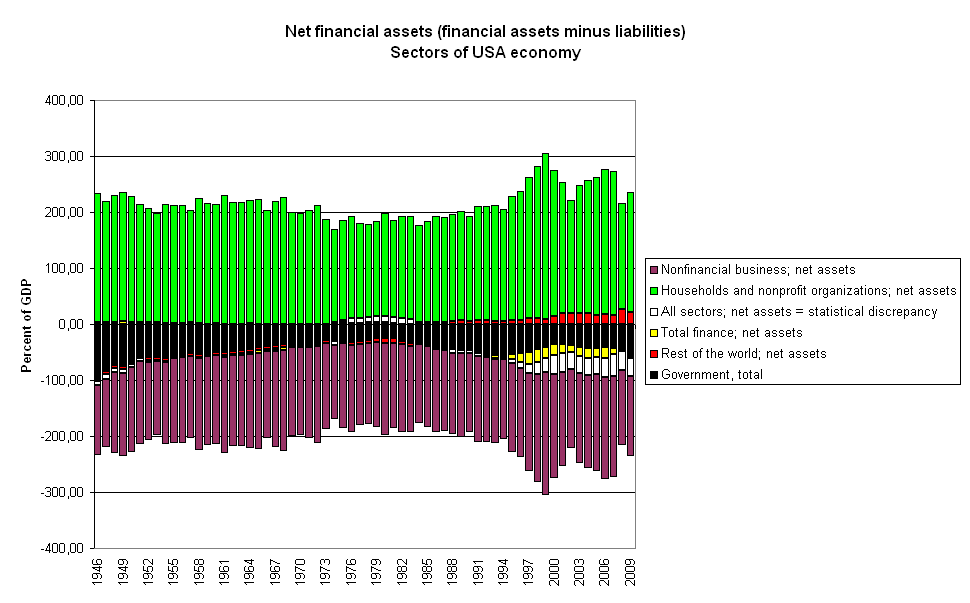

SOMF Asset Patterns English: Net financial assets (financial assets mi...

English: Net financial assets (financial assets mi... Seal of the United States bankruptcy court. Church...

Seal of the United States bankruptcy court. Church...It also helps to ensure that accurate and reliable accounting data are produced. It is a good system to manage the internal operations.

To accomplish the internal control system, and for it to work efficiently some broad principles are established. They are as follow: 1. Clearly Establish Responsibilities.

2. Maintain Adequate Records.

3. Insure Assets and Bond Key Employees.

4. Separate Record-Keeping and Custody over Assets.

5. Divide Responsibility for Related Transactions.

6. Use Mechanical Devices Whenever Feasible.

7. Perform Regular and Independent Reviews.

QS 7-2b. Why should record-keeping for assets be separated from custody over the assets? Answer. Record-Keeping for assets should be separated from custody over the assets as the custodian of an asset, knowing that a record of the asset is being kept by another employee, is not as likely to misplace, steal or waste the asset. The record keeper, who does not have access to the asset, has no reason to falsify the record. This principle assures that the fraud is less likely to happen. QS 7-3. In a good system of internal control for cash that provides adequate procedures for protecting both cash receipts and cash disbursements, three basic guidelines should always be observed. What are these guidelines? Answer. The three basic guidelines that should be always observed, which provide adequate procedures for protecting both cash receipts and cash disbursements are as follow: 1. Duties should be separated so that people responsible for actually handling cash are not responsible for keeping the cash records.

2. All cash receipts should be deposited in the bank, intact, each day.

3. All cash payments should be made by cheque.

QS 7-4a. The Petty Cash Fund of the No-Fear Ski Club was established at $50. At the end of the month, the fund contained $4.35 and had the following receipts: film rental $12.50, refreshments for meetings $20.15 (both expenditures to be classified as Entertainment Expenses), postage $4.00, and printing $9.00. Prepare the journal entries to record (a) the establishment of the fund; (b) the reimbursement at the end of the month.

Answer. Account Title and Explanation Dr. Cr. (a) Petty Cash 50.00 Cash 50.00 Established a petty cash fund.

(b) Entertainment expenses 32.65 Postage 4.00 Printing 9.00 Cash 45.65 Reimbursed petty cash.

QS 7-4b. Explain when the Petty Cash account would be credited in a journal entry.

Answer. The fund in the Petty Cash account is increased if it is being exhausted and reimbursed to frequently. If the Petty Cash Fund becomes too large due to these increases, some of the money from the fund is redeposited in the Cash account (chequing account). For such a reduction the Cash account is debited and the Petty Cash account is credited.

Cash

Cash Cash

Cash buried cash

buried cash