SunGard Write-up

Is SunGard a good LBO candidate? Why? Why not?

We believe SunGard is a strong LBO candidate for the following reasons:

- Formed in 1983, SunGard is a well-established and industry leading company, which operates in the maturing information technology sector. There are relatively few risks to the company's business model and market position

- SunGard has a low debt-to-equity ratio with only $519 mn of long-term debt and over $3 bn of total equity in 2004

- The company is run by a strong and experienced management team. The CEO, Executive Vice President, and CFO all have approximately 15 to 20 year tenures with SunGard.

- SunGard has consistently grown revenue and net income in the past 5 years, illustrating the company's ability to capture market share in the industry

- SunGard has low working capital requirement, with no inventory, and minimal year-to-year changes in working capital

- The company has strong cash flows from operations, which has more than doubled in the past 5 years and has enabled the company to repay large portions of its debt

- There are low future investing and capital expenditure requirements, assuming the company stops making cash acquisitions

- There appears to be feasible exit options such as an IPO, given the high demand from investors which is reflected in the company's rising stock price

- There is the possibility of selling non-core assets to consolidate operations and raise cash, exemplified by the contemplated sale of the company's availability services business

Qualitatively, is the deal a good investment for the buyout investors?

Qualitatively, SunGard appears to be a good (but not great) investment for the private equity firms for the following reasons:

- Ability to leverage company; investment financed with approximately 30% equity

- Ample cash flows to...

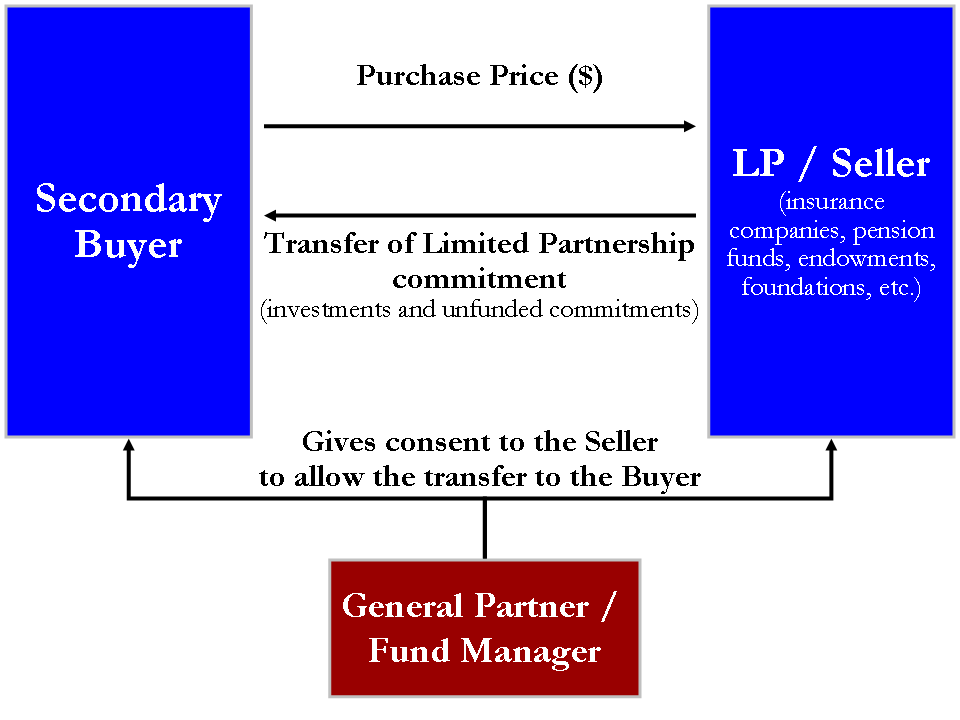

English: Diagram of secondary market transfer for ...

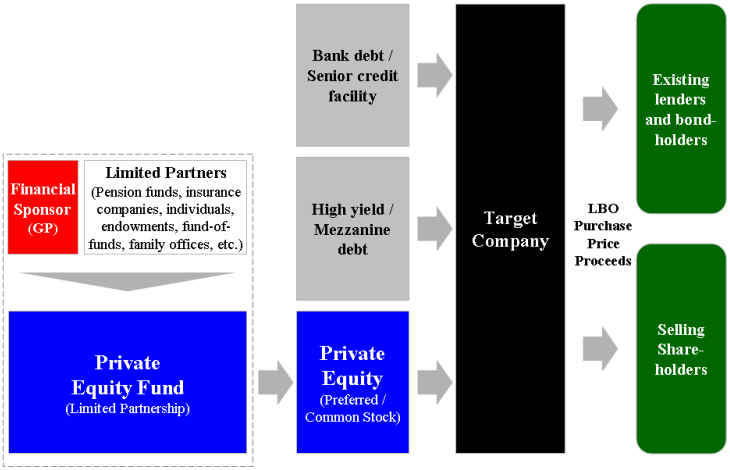

English: Diagram of secondary market transfer for ... Diagram of leveraged buyout transaction structure ...

Diagram of leveraged buyout transaction structure ... English: Diagram of private equity co-investment s...

English: Diagram of private equity co-investment s...