Executive summary Since July 1993 when Tiffany & Company made the new agreement with its Japanese distributor, Mitsukoshi Limited, Tiffany would face the risk of any exchange-rate fluctuations which previously Mitsukoshi used to bear. In addition, as long as the retail sales in Japan are expected to increase, it is necessary that Tiffany hedge the risk of exchange rates between dollar and yen. Basically two kinds of derivatives which are forward contract and put option, will be regarded as risk hedging tools. In this report, hedging is defined as the purchase or sale of foreign exchange forward or option to offset completely the risk of fluctuation in a rate of exchange when payments are to be made in that foreign currency in the future Analysis Basically we split our analysis methods into three parts, which are one-month hedging, two-month hedging, and three-month hedging analysis. Then we will look into the profits from each hedging method, assuming that Japanese yen will be depreciated in the near future as it was mentioned in the case.

Balance & Options

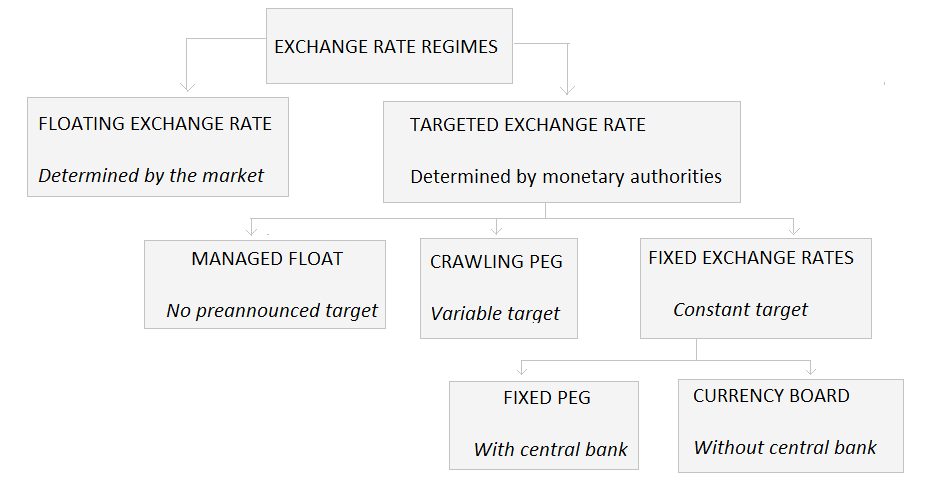

Balance & Options English: Exchange Rate Regimes

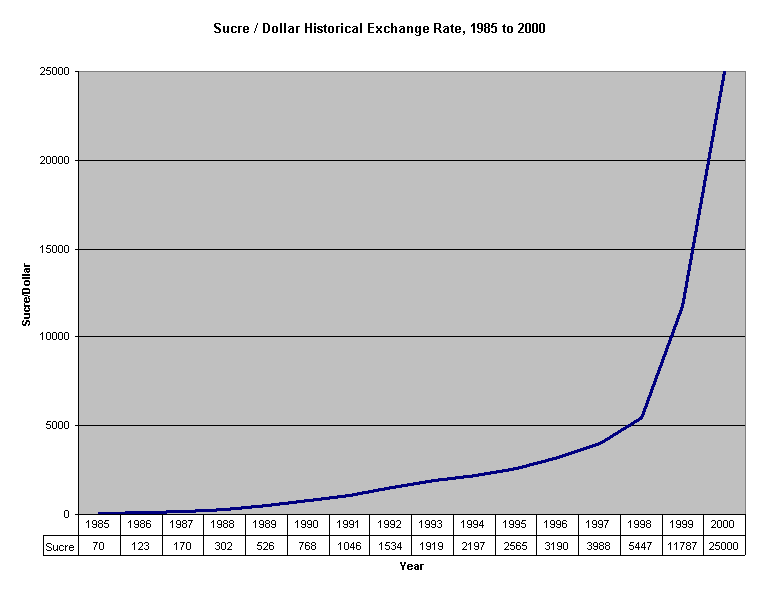

English: Exchange Rate Regimes Historical exchange rates between the ecuadorian S...

Historical exchange rates between the ecuadorian S...But also we will simulate several cases of Japanese yen?s appreciation.

First we would like to mention the cost of purchasing each put option then each cost will be used to calculate the profit from each derivative.

Here is the cost of buying put option. Actually Tiffany Co. needs to exchange yen into dollar so we are not regarding call option but put option.

Strike Price July August September Strike Price July August September The cost of put option purchase Calls Puts July August September 87.0 87.0 0.36 -$225.0 89.0 89.0 0.54 -$337.5 90.0 90.0 0.25 0.5 0.92 -$156.3 -$312.5 -$575.0 91.0 3.32 91.0 1.04 -$650.0 91.5 91.5 0.85 -$531.3 92.0 1.54 2.52 92.0 0.57 1.07 1.44 -$356.3 -$668.8 -$900.0 92.5 92.5 0.94 1.12 1.63 -$587.5 -$700.0...