Introduction

Standard Costing became increasingly widespread at the beginning of the 20th century as a system for determining the manufacturing unit cost of a product, by setting standard rates and required material quantities for various production processes (Hyer & Wemmerlöv, 2002). Drury (2008) state that "Product standard costs are derived by listing and adding the standard cost of operations required to produce a particular product." The popularity of this technique increased significantly in the manufacturing industry, mainly because it could be used as a mechanism for managing cost, which could then be used to set product prices.

Over the years, standard costing systems have become more than just cost control tools by helping managers in other decision-making areas, such as performance evaluation and profit measurement. However, towards the end of the 20th century, standard costing has been increasingly criticised as an inadequate management technique. Authors such as, Kaplan and Johnson (1987), Ferrara (1995) and Monden and Lee (1993) have argued that standard costing is inconsistent in today's extremely competitive and global business environment.

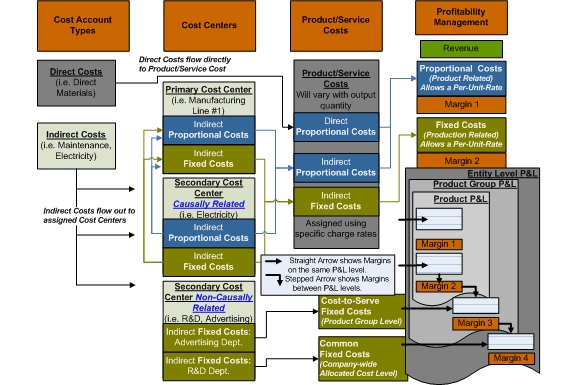

English: GPK Marginal Costing Structure Flow of Gr...

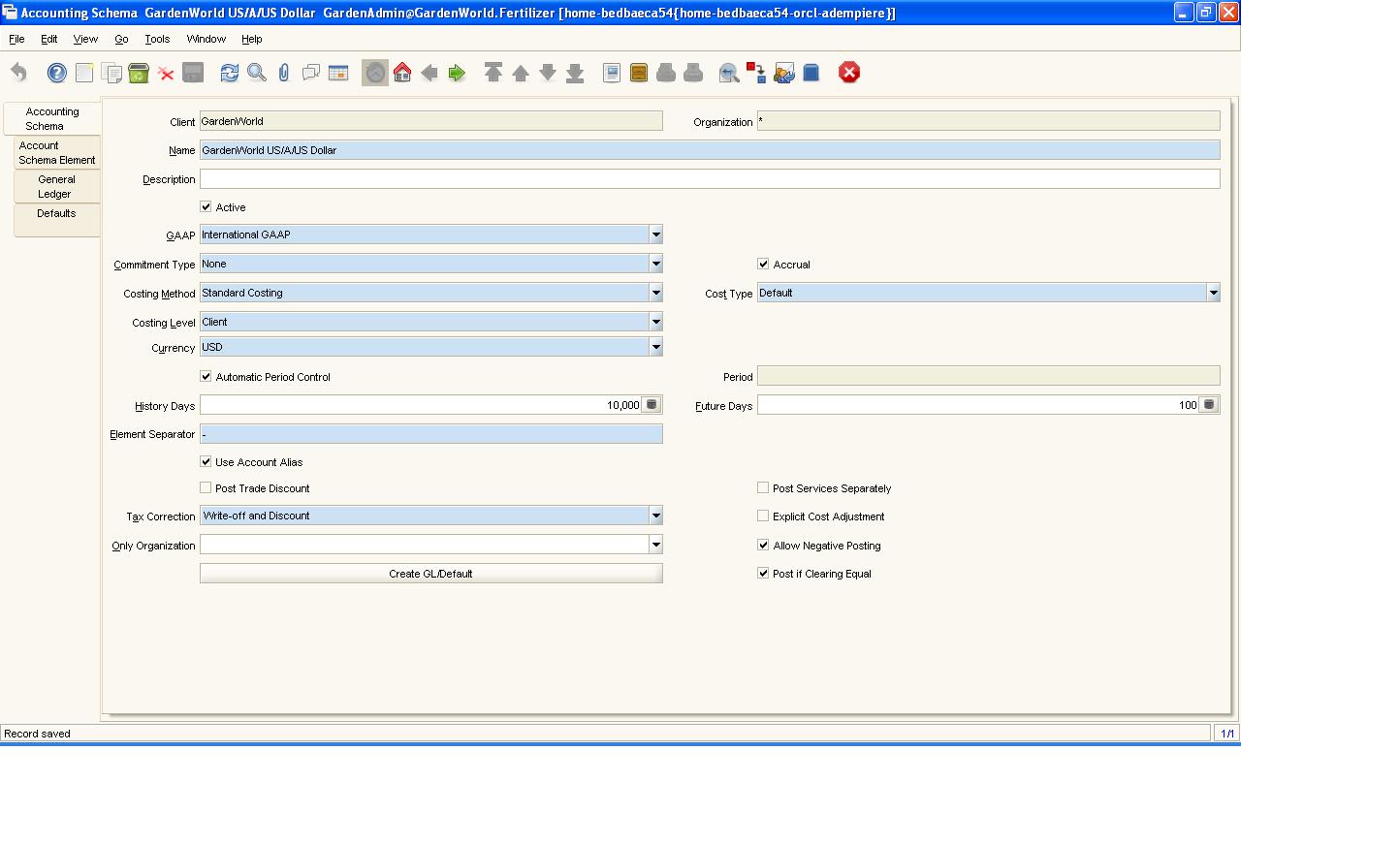

English: GPK Marginal Costing Structure Flow of Gr... English: Accounting Schema : Setting the standard ...

English: Accounting Schema : Setting the standard ... English: Industry in Waterden Road These are the l...

English: Industry in Waterden Road These are the l...They maintain that standard costing can produce certain types behaviour that could threaten the survival of modern businesses. Despite, the growing concerns regarding the application of standard costing in a rapidly changing economic environment, standard costing has remained a relatively common tool among business managers and is still regularly taught to students on various accounting and management courses.

This paper aims to critically analyse the use of standard costing as a control technique in a new era. Firstly, standard costing will be examined so as to understand its application in the business world. Secondly, arguments from various researchers will be presented, which support and criticized the use the standard costing. Finally, these arguments will be weighed, so as to draw conclusions as to whether standard costing is...