According to the AASB Framework, the entity need to disclosure all relevant information, which has an influence on the economic decision making of users when they evaluating past, present or future events or confirming, or correcting past evaluations (AASB Framework). The nature and materiality of information is crucial when judging the relevance of financial statement. The quality of relevant transaction account in the financial report help users not only to predict and identify the financial performance and position of the entity, but also evaluate the capability of entity in shielding against risks (AASB Framework).

Besides relevance, reliability is another indispensable characteristic of financial statement. Reliability quality requires the information provided by the entity must be free form material error and bias. Thus users can rely on these information to evaluate the position of the entity. Some qualities, such as faithful representation, substance over form, neutrality, prudence and completeness, are important standard when preparing reliable information (AASB Framework).

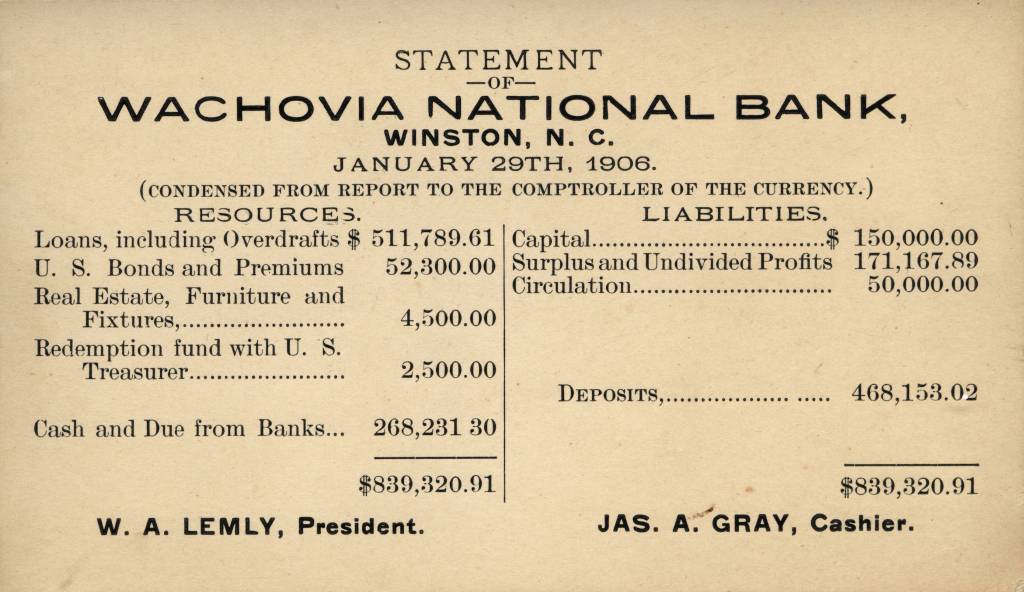

Historical financial statement

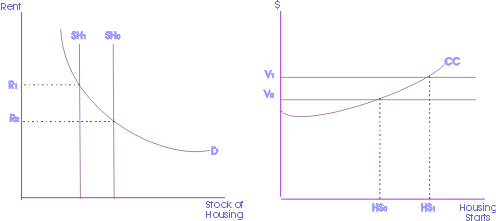

Historical financial statement English: Real estate economics - with depreciation

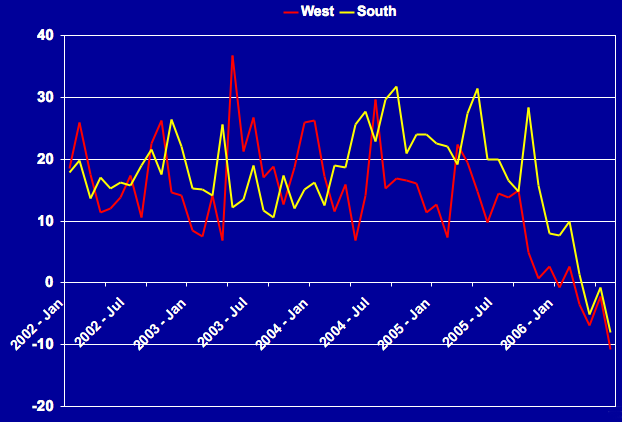

English: Real estate economics - with depreciation English: Condominium Price Depreciation in the sou...

English: Condominium Price Depreciation in the sou...Using fair value as an example, the reliability requires entity to estimate the fair value of asset based on the substance over form rule. However, due to the need of estimation and judgement of some accounting issues such as revaluation and depreciation, the reliability of information cannot be precisely fulfilled. Besides, some constraints on relevant and reliable Information are worth mentioning. In some circumstances, the reliability and relevance are mutually contradictable sue to timeliness (AASB Framework). For example, some contingent liabilities, such as legal action, are very uncertain but may have material relevance for users to make decision (AASB Framework).

In the comparison and contrast of property, plant and equipment (PPE) treatment method in both companies, it can be seen that both company state PPE at historical cost less depreciation. Historical cost includes expenditure that is directly attributable to the acquisition of the...