To: John Clayton

From: Controllers

RE: Recommended accounting policies in light of new business plans and lending conditions

ROLE: Accounting controllers hired to assess 2014 financial statements to advise on appropriate accounting policies due to changes in business plans and new lending conditions.

USERS: As Wellness Fitness Limited's (WFL) CEO, you want to maximize net income and shareholders' value. The two external shareholders are users who also want to maximize net income and shareholder value to increase their return. Finally, Morgan Bank is another user who wants to ensure that financial statements comply with IFRS standards and GAAPs. They also want to ensure that the company complies with the current ratio covenant and is financially stable to repay the requested bank loan. The bank is the most critical user because without this sizeable loan, the company would be unable to grow and expand its membership.

CONFLICTS: Management will want to recognize revenue right away and defer expenses to maximize income.

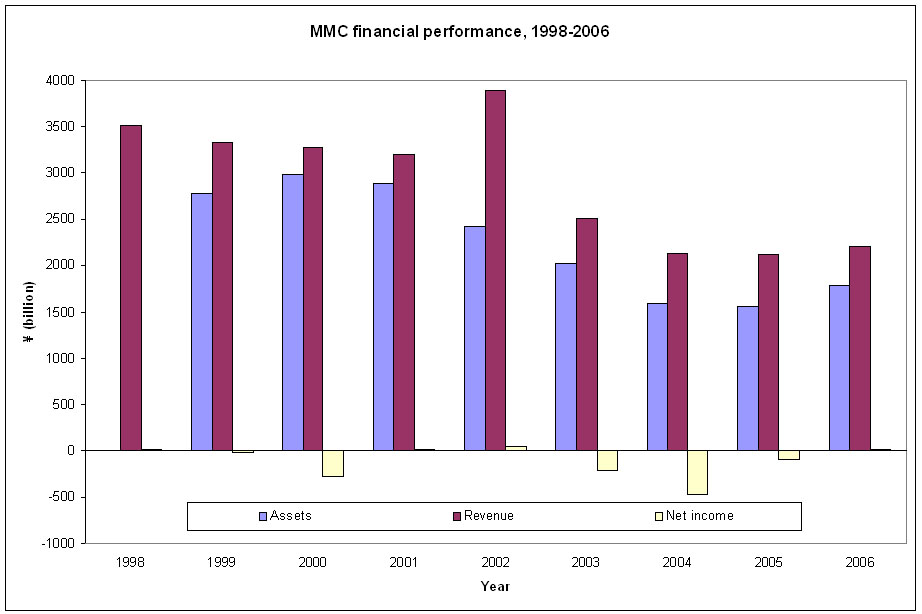

Graph of consolidated financial results of Mitsubi...

Graph of consolidated financial results of Mitsubi... Net Income

Net Income Net Income

Net IncomeThis may not comply with IFRS which conflicts with the bank's objectives.

CONSTRAINTS: As a public company and as requested by the bank, annual audited financial statements must be prepared using IFRS standards. To receive the bank loan, the year-end current ratio must not drop below 1.2:1, as stated by the bank's covenant. Ethics is another constraint because users will want to ensure that management is not biased in fulfilling personal goals; financial statements should accurately reflect the business' financial position.

ISSUE #1: Depreciation of Capital Assets

Depreciation on capital assets was not recorded. Under accrual accounting and IFRS, a portion of the cost of these capital assets must be expensed each month to reflect their use. Depreciation is not a fictitious expense; it is a non-cash expense that cannot be ignored because cash is not...