Accounting convention

Definition: -

The definition of accounting convention is Ground rules of accounting that should be followed in preparation of all accounts and financial statements and is designed to help accountants overcome practical problems that arise out of the preparation of financial statements. �

The major rules of convention briefly described below are the most generally accepted:

Business entity convention:

Each set of accounting record should deal with a specific and identifiable business activity. It should deal with only the financial transactions, facts and events relating to that specific activity. The business entity convention must be distinguished from the legal position that may exist between businesses and their owners. For sole proprietorships and partnerships, the law does not make any distinctions between the business and owners. For the limited companies can be both an counting entity and a legal entity, provided that it is not a holding company.

Historic cost convention:

This convention holds that the cost of assets shown on the balance sheet must be based on their historic cost (that is acquisition cost).

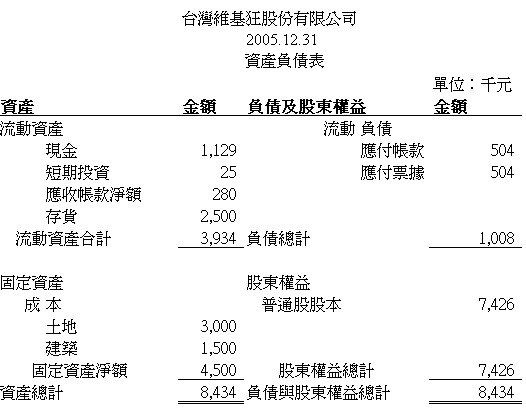

balance sheet in chinese

balance sheet in chinese English: Sample Domestic Balance Sheet (DBS)to be ...

English: Sample Domestic Balance Sheet (DBS)to be ... English: Balance sheet venetian method Česky: Roz...

English: Balance sheet venetian method Česky: Roz...This way of measuring asset value is preferred over other methods based on some form of current value.

Many people find the historic cost convention not easy to support, as outdated historic costs that recording assets at their recent value would provide a more practical view of financial position and would be relevant for a large range of decisions. However, a system of measurement based on current values can present a number of problems.

This convention is also extremely convenient in that it does nothing to concern the double entry system.

Prudence convention:

This convention more than any other that has increase to the idea that accountants are more negative people!! In essence the concept says that whenever there are alternative actions or...