�PAGE � �PAGE �4� Accrual Versus Cash

Accrual versus Cash Based Accounting

In the cash method of accounting, you record your expenses and income when cash is exchanged. You record income when you receive payment and you record expenses when you actually pay them. This method is used most by small business owners. Cash-basis accounting is a method of bookkeeping that records financial events based on cash flows and cash position. Revenue is recognized when cash is received and expense is recognized when cash is paid. In cash-basis accounting, revenues and expenses are also called cash receipts and cash payments.

Cash-basis accounting does not recognize promises to pay or expectations to receive money or service in the future, such as payables, receivables, and prepaid expenses. This is simpler for individuals and organizations that do not have significant amounts of these transactions, or when the time lag between the initiation of the transaction and the cash flow is very short.

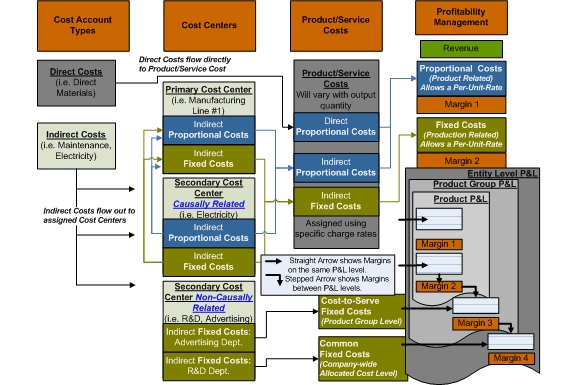

English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... English: Business Line Finance and Accounting

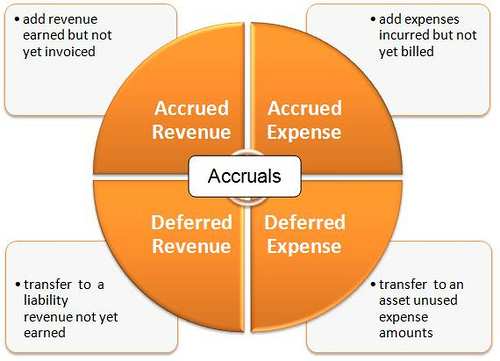

English: Business Line Finance and Accounting y2cary3n6mng-76r9m3-accruals

y2cary3n6mng-76r9m3-accrualsSome of the issues with cash-basis are this accounting fails to meet GAAP requirement because it does not follow the following two principles:

revenue recognition principle - revenue should be recognized when it is realized (e.g. a credit sell).

matching principle - revenue should be matched to the expense if possible (e.g. Sales to COGS).

Additionally, cash-basis accounting is not viable for cost accounting in manufacturing operations because expense is not associated with product cost.