EXECUTIVE SUMMARY

The purpose of this report is to present the pilot Activity-Based Costing (ABC) for the University. The emergence of ABC systems has been viewed as the means by which management accounting can re-establish its relevance. It became popular towards the 1980's, because it prevents cost distortion and provides a process view with traditional accounting cannot provide.

The University is considering adopting ABC because the widespread concern about rising costs for higher education and the unique characteristics of universities that make for special challenges.

The report discusses the various changes in the manufacturing sector with regard to the introduction of ABC and shows how this method can be employed in a higher education institution. It also discusses the advantages and disadvantages of using ABC and explains how ABC may, or may not help the university control its costs.

TABLE OF CONTENTS

TABLE OF CONTENTS 1

INTRODUCTION 2

MAIN BODY 2

CHANGES IN THE MANUFACTURING SECTOR WITH REGARD TO THE INTRODUCTION OF ABC 2

HOW ABC MAY BE EMPLOYED IN A HIGHER EDUCATION INSTITUTION 3

ADVANTAGES OF USING ABC 3

DISADVANTAGES OF USING ABC.......................................................................................................................

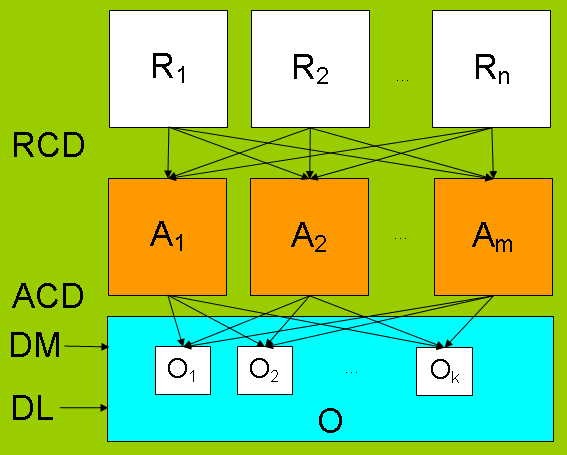

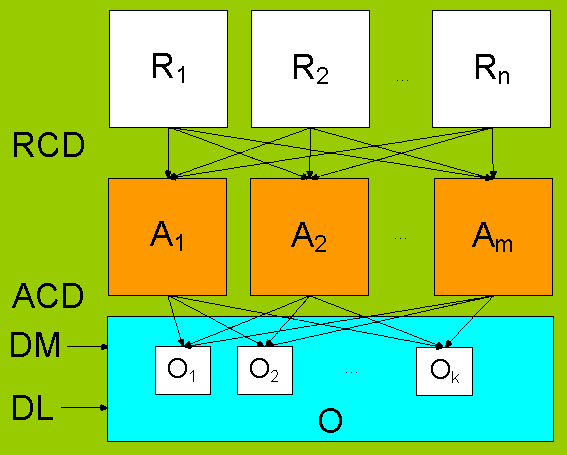

English: Simprocess integrates Process mapping, de...

English: Simprocess integrates Process mapping, de... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver........4

HOW ABC MAY, OR MAY NOT HELP THE UNIVERSITY CONTROL ITS COSTS 4

CONCLUSION 4

APPENDIX 6

APPENDIX 1: DIFFERENCE BETWEEN ABC AND TRADITIONAL COSTING 6

APPENDIX 2: ACTIVITY-BASED COSTING : APPLICATION TO HIGHER EDUCATION 7

APPENDIX 3: EXAMPLE ON INPLIMENTATION OF ABC 7

BIBLIOGRAPHY 9

1. INTRODUCTION

Traditional costing system has been criticised for cost distortion and lack of relevance during the last 20 years (Johnson and Kaplan 1987). A new costing method, known as Activity Based Costing, was developed as a means of overcoming the systematic distortions of traditional costing systems.

ABC was innovated 50 years ago, but its implementation started in the 1980s due to the intense global competition which led to...