Activity based costing (ABC) is a relative new way to allocate costs to specific processes and services. This system assures that the costs are accurately distributed to the products or services that generated them. ABC illustrates costs more accurately, giving management insight to the cost associated with certain business activities. ABC extends the decision-making skills of management by expanding on traditional costing (job order costing/process order costing) techniques. However, since ABC's introduction in the 1980's, many corporations are not using ABC, despite gained managerial decision making capabilities. Even by the mid-1990s, ABC's use has not spread throughout the accounting industry and its use is not obvious (Selto & Jasinski, 1996). The following article will discuss the pros and cons of the ABC method.

ABC is an extension of traditional product costing techniques. These techniques are called job order costing and process order costing. A job order costing system arranges costs for each unit as it goes through a production process.

Cost per Megabase of DNA Sequence (Why biologists ...

Cost per Megabase of DNA Sequence (Why biologists ... English: Simprocess integrates Process mapping, de...

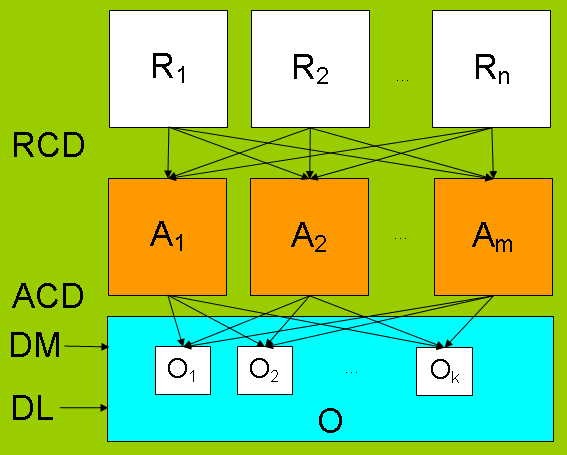

English: Simprocess integrates Process mapping, de... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver...A process cost system collects costs in work in progress account. The numbers of units worked are recorded for the accounting period.

These systems alone do not accurately illustrate costs incurred. Instead, these two costing techniques generally lump costs into 3 main categories (cost centers). These three categories are direct materials, direct labor and overhead. Cost drivers are then assigned to represent the relationship between the cost and the process it is allocated to.

ABC provides a better map of the costs of manufacturing products or distributing services. ABC uses a multitude of activity centers, which are the equivalent to the previously mentioned traditional cost centers. Each of these activity centers has its own cost driver and driver rate. ABC identifies many different costs to products by adjusting the cost driver and driver rates to specific activity centers. This process...