� DATE \@ "M/d/yyyy" �12/2/2007�

Activity-Based Costing

In

Government

�

Table of Contents

Executive Summary

Activity-Based Cost (ABC) Management

What is ABC?

Traditional Cost Systems vs. ABC

Strengths and Weaknesses of ABC

ABC Usage In Government Agencies

A Real Life Example: Texas State Government

Conclusion / Recommendations

Appendix

References

�

Executive Summary

Activity-Based Cost management is one of the most important methodologies in the managerial accounting for data analysis and decision making. ABC can help both public and private organizations improve their cost structure, and it carries a vital role for these organizations to understand their cost behavior. This paper addresses what basically ABC intended to do, its strengths and weaknesses, and describes successful applications of ABC in the public sector, which includes a real life example. There will be recommendations section at the end upon improving the performance throughout an organization.

�

II. Activity-Based Cost Management

What is ABC?

In the rapidly developing and globalizing world, markets become much intense than before, therefore, organizations started to seek for methods where they can do more with less.

Cost per Megabase of DNA Sequence (Why biologists ...

Cost per Megabase of DNA Sequence (Why biologists ... English: Simprocess integrates Process mapping, de...

English: Simprocess integrates Process mapping, de... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver...The successful companies not only compete against domestic competitors, but also the companies over the world. For example, after China entered into World Trade Organization, they opened their domestic market for the western companies in different industries such as car manufacturing, farm products and so on. Due to the product enrichment, the customers in China have more options than ever, and they started to seek to find the high quality goods. In order to compete in such competitive business environment, companies became more customer-driven, therefore, their costs increased.

The above situation is not only faced by China, but all over the world. The significant changes in the world's market mechanisms influenced the development of a new managerial accounting methodology, called Activity-Based Costing. "A powerful tool for measuring performance, Activity-Based Costing is used to identify, describe, assign costs to, and report on agency operations"�. Activity-Based Costing, ABC, is simply assigning costs to activities based on how the costs are consumed by the ongoing processes in an organization. In other words, costs are charged to processes or products based on the amount of each activity within that process, therefore, it's understood that products or services which may seem similar in terms of profits can be actually quite different. As a result of ABC implementation, the full cost of a service now covers all direct and indirect costs that are related to that service. Direct costs may include wages, salaries, and benefits of the employees who are working to produce that service, as well as the materials and/or supplies used. "The agents that cause activities to happen are called cost drivers."� Indirect costs may include Shared Administrative Expenses, support functions and so on. The goal of Activity-Based Costing is to understand how costs are incurred. The use of Activity-Based Costing systems is one technique that can provide valuable benefits to an organization by enhancing accurate product costing and management decision making. ABC systems can help managers assess whether or not the company is performing the right activities.

Traditional Cost Systems vs. ABC

It's important to understand how traditional cost systems and ABC differ. This can be vital for managers because they are the ones who are going to implement a cost system to their organization, and wrong implementations may result with dramatic results, such as wrong cost allocations, product drops due to profit miscalculations and so on. In the table below some of the differences between traditional cost systems and ABC listed:

Traditional Cost Systems | ABC |

Structure-oriented | Process-oriented |

Overhead is allocated on volume based | Allocate costs to products or services from activity cost pools |

Top to bottom approach (Model is present, cost is distributed on every operation) | Bottom to top approach (No model at first, a model is created based on actual operations) |

Tries to understand cost behavior with a predetermined budget | Tries to understand how costs are incurred |

Less number of overhead cost pools and rates (cost drivers) | More number of overhead cost pools and rates |

Managers don't know the real costs of the products and services | Creates a vision for the managers to better explain the real costs of a product or service |

Generally simple, understandable by everyone with little accounting knowledge | Most of the time complex and hard to understand system. Occasionally, needs special training and costs more to implement |

Strengths and Weaknesses of ABC

Firstly, the implementation of ABC is very advantageous in a highly competitive market, because the system would not under-cost complex, low volume products or services and over-cost simple, high-volume products or services. Secondly, it can help in improvement in cost-control: managers can see costs broken out by a number of activities rather that buried in one or two overhead cost pools. The pooling of costs by activities provides information that helps managers to better plan and control costs. ABC system also generally improves the ability of an analyst to estimate the cash flows. By separating costs into activity pools and identifying a cost driver in each cost pool, the analysts are able to determine more accurately, the levels of various costs that will be incurred.

The major problem with ABC system is that the cost of implementing may exceed the benefits. While using ABC, it can be difficult to associate a cost with driver and measure the effect of the activity on that cost. Also the calculations are generally very complex and may not be worthwhile if the information is not used. Similarly, ABC provides data which has a wide variety of usage. Therefore, different uses require more or less detail or accuracy. This brings the necessity of building a cost system with a clear idea of the types of decisions or assessments that the ABC data will be asked to support. Some implementations of ABC can be either too detailed or not detailed enough.

"Eventually, as the ABC/M data are applied as an enabler for multiple uses, the size of the system and level of effort to maintain it typically stabilizes at an appropriate level. Through using the data, the ABC system self-balances the tradeoff between the level of administrative effort to collect and report the data and the benefits as it meets various users' needs"�.

III. ABC Usage in Government Agencies

"Measuring the cost of government services is useful for a variety of purposes, including performance measurement and benchmarking; setting user fees and charges; privatization; competition initiatives or 'managed competition'; and activity-based costing and activity-based management"�. Over the world, most of the government offices are experiencing financial pressure to continue their operations without increasing their price. These government offices have to spend and the form of spending can be very diverse. The main cause of the expenditure is the effort of serving people better, either due to the political reasons or the responsibilities each government office carries. While serving, trying to be cost effective is a tough task to handle. Like I mentioned in the beginning of this paper, there is a competitive environment which is valid for the government offices too. Each agency is competing with the one in another city or the ones in the same city's suburbs. These suburbs sometimes can be more advantageous by keeping their costs lower than cities, as a result of dealing with much smaller populations.

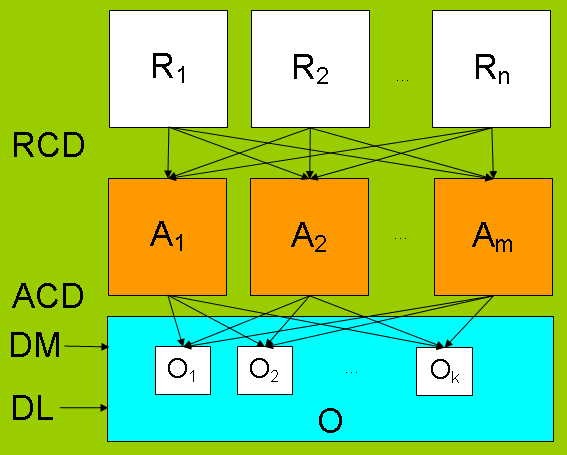

When the state and local governments have the duty to serve, they are having difficulty because of limited funding by federal government. "Regardless of where the pressure is coming from, the message to government from citizens is this: better, faster, cheaper-hold the line on taxes but don't let service slip"�. On top of this, people want to be taxed less and the quality in the government offices has to be high. To achieve all of these, a need for better costing, and the tools to survive in this environment rises, and this is where ABC enters the game. "ABC/M answers fundamental questions such as 'what do things cost?' and 'why?' It further answers 'who in particular receives them?' and 'how much costs did they each receive?'� This is important because one cannot compete if s/he doesn't know how to cost. It's important for the public organizations or government offices to know what the cost of each service or product they produce is, rather than knowing how much they spend over the previous time periods. Because, knowing the cost of each service helps the officers to make better decisions for the future. Figure 1 below explains which part in a cost system ABC reveals information for better decision making. This valuable information then can be used to recover the costs through fees that the government office charges, and help to create new visions in order to providing more efficiency by trying different alternatives.

Figure 1 - The Primary View of Most Managers�

As a result of successful implementation of ABC to government offices, the government services can be clearly reviewed and understood by the managers. This will bring lower costs, therefore lower prices for us people by the means of less taxes and fees we pay everyday for government services. If government offices know how much their services cost, they can sign more contracts and do more business, rather than outsourcing, which will result in more revenues and higher quality services for community.

IV. A Real Life Example: Texas State Government

We talked about the advantages when the government offices take action and implement ABC. In response to this, Texas State Government decided to put ABC into place in the five agencies; General Services Commission, Texas Water Development Board, Texas Workforce Commission, Texas Department of Economic Development and Texas Cosmetology Commission, as well as two volunteer agencies, the Texas Department of Transportation and the Texas Comptroller of Public Accounts. The employees of these agencies are trained in order to conduct ABC system. The pilot involved 16 major programs or agency divisions encompassing hundreds of business activities in the seven agencies. Agency employees documented their current business processes, estimated the time and resources needed to carry them out, and distinguished between activities that contribute to their organizations' missions and those that do not. As a result, the management team was able to identify a number of useful improvements to current processes. The pilot project was completed in Fall 2000. In assessing its results, the management team reached the following conclusions*:

While ABC/ABM studies can be costly in terms of time and other resources, the net return on such an investment in Texas could be considerable.

To realize the greatest impact per dollar spent on ABC/ABM, the state should target its use, rather than requiring its widespread application across all government activities.

State agencies should consider using an ABC study to estimate the true cost of any activities under review. This will enable them to pursue reengineering opportunities and benchmark their operations against other public and private organizations.

The ultimate success of ABC/ABM depends on how agencies use the study results. The ABC/ABM pilot project is only the beginning of a more detailed process that agencies must go through to realize results and cost savings.

Many of the savings identified in this report represent savings in productivity, which are not always easily translatable into hard dollars.

Many opportunities for improvement identified in the pilot project would require an investment in new technologies.

Participating agencies sometimes found that, to achieve the full benefits of ABC/ABM, they would need the cooperation of other agencies or amendments to existing legislation.

*: More detailed information about Texas State Government can be found in Appendix.

V. Conclusion / Recommendations

It's a known truth that Activity-Based Costing system is not suitable for all the organizations and companies. In other words, "⦠is not a panacea for all the product cost accounting ills or shortcomings in manufacturing."� It's the complexity that makes ABC implementation a costly and tough job. But once an organization adopts the ABC, the long-term savings can make it worthwhile. For a government office, having quality services and low costs at the same time is vital because they have lots of expenditure but limited funding. While ABC can be useful to calculate the real cost of the services they provide, it can also be a good guide to show alternative service delivery options. I think government offices like Texas State Government should adopt the ABC system when they need to boost their client base. Also, ABC will help them to understand whether or not they are fully recovering the costs of the services they provide. They will be able to compare and compete with the other public sector organizations and private sector companies which are doing the similar operations.

As I mentioned above, the difficulty of ABC lies under its complexity. The employees who are going to use this system can create resistance for the change. But this difficulty can be overcome by using effective techniques. Like Texas State Government used, the employees can be trained using consultant companies who are aware of the ABC system and its yields, and can transmit this information to the employees. When the employees become aware of what this new system can add, they wouldn't resist as hard as before. This training can be costly, but again the long-term benefits can outweigh this cost.

Lastly, it's my recommendation that the government agencies should add value to what ABC system brings. All in all, ABC system can only bring data. It's those agencies who should evaluate this data and act accordingly. If they do not progress in this direction, they won't have a chance to realize the real cost savings. Once they start acting in the right direction, all the efforts and risks involved while implementing ABC will be outweighed by the benefits of this tool.

�

Appendix

Summary of Review Areas in Texas State Government Project

Agency | Program Area | FY99 Total Cost (Areas studied) | Gross Potential Savings | Savings Percent of Total Costs |

General Services Commission | Business Machine Repair | $1,602,140 | $188,680 | 11.7% |

Leasing | 928,891 | 125,425 | 13.5% | |

Capitol Zone Maintenance | 5,123,168 | 169,480 | 3.3% | |

Total GSC | $7,654,199 | $483,585 | 6.3% | |

Department of Transportation | Voucher Processing- Central only | $3,088,249 | $414,735 | 13.4% |

Map Sales | 518,283 | 308,182 | 59.4%* | |

Total TxDOT | $3,606,532 | $722,917 | 20% | |

Texas Workforce Commission | Controller | $2,141,086 | $71,160 | 3.3% |

Unemployment Insurance Collections | 2,053,916 | 226,460 | 11% | |

Austin Tax Office | 957,890 | 89,400 | 9.3% | |

Out of State Unit | 366,900 | 40,950 | 11.1% | |

Total TWC | $5,519,792 | $427,970 | 7.7% | |

Texas Cosmetology Commission | All Areas | $2,452,353 | $546,710 | 22.2% |

Total TCC | $2,452,353 | $546,710 | 22.3% | |

Texas Water Development Board | Loan Servicing: D Fund II Program | $6,557,745 | $257,732 | 3.9% |

Total TWDB | $6,557,745 | $257,732 | 3.9% | |

Texas Department of Economic Development | Finance | $1,265,480 | $113,050 | 8.9% |

Internet Clearing House | 1,133,670 | 172,360 | 15.2% | |

Total TDED | $2,399,150 | $285,410 | 11.9% | |

Comptroller of Public Accounts | Revenue Processing | $11,106,521 | $2,772,956 | 24.1% |

Account Maintenance | 12,323,182 | 2,180,895 | 19.4% | |

Revenue Refunds | 6,835,098 | 837,900 | 11.1% | |

Revenue Accounting | 9,478,357 | 372,456 | 3.9% | |

Total CPA | $39,743,158 | $6,164,207 | 15.5% | |

Total All Agencies | $67,932,929 | $8,888,530 | 13% |

�

References

Norm Raffish, "How Much Does That Product Really Cost", Management Accounting (March 1991): 36-39

Activity-Based Costing Concept Paper, OSD Comptroller iCenter, 2002

http://www.dod.mil/comptroller/icenter/learn/abconcept.htm

James D. Tarr, "Activity Based Costing in the Information Age", ACA Group, 2004

http://www.theacagroup.com/activitybasedcosting.htm

Cost Analysis and Activity-Based Costing For Government, GFOA, 2004

SAS White Paper, Activity-Based Cost Management in Government - Applying ABC/M to Critical Problems in the Public Sector

"Activity-Based Costing in Texas Government", Report to the 77th Texas Legislature, January 2001

http://www.cpa.state.tx.us/specialrpt/abc/

Ronald W. Hilton (fifth Edition) Managerial Accounting, McGraw-Hill Higher Education

Robert S. Kaplan, "The Four Stage Model of Cost Systems Design," Management Accounting, February 1990

� Department of Defense, Activity-Based Costing Concept Paper, 2002

� Norm Raffish, "How Much Does That Product Really Co$t", Management Accounting (March 1991)

� SAS White Paper, Activity-Based Cost Management in Government - Applying ABC/M to Critical Problems In The Public Sector

� Cost Analysis and Activity-Based Costing for Government, The Government Finance Officers Association (GFOA), 2004

� SAS White Paper, Activity-Based Cost Management in Government - Applying ABC/M to Critical Problems In The Public Sector

� SAS White Paper, Activity-Based Cost Management in Government - Applying ABC/M to Critical Problems In The Public Sector

� SAS White Paper, Activity-Based Cost Management in Government - Applying ABC/M to Critical Problems In The Public Sector

� Norm Raffish, "How Much Does That Product Really Co$t", Management Accounting (March 1991)

�PAGE � � PAGE �15�