Case Analysis Report:

U.S. Bank

Table of Content

4Abstract �

5Introduction �

5Liquidity Position Evaluation �

7Quality of Assets �

7Delinquent Loan Ratios �

8Net charge-off �

8Nonperforming assets �

9Capital Adequacy �

11Expected Future Performance �

13Conclusion: �

14Appendix: �

15Reference �

�

Abstract

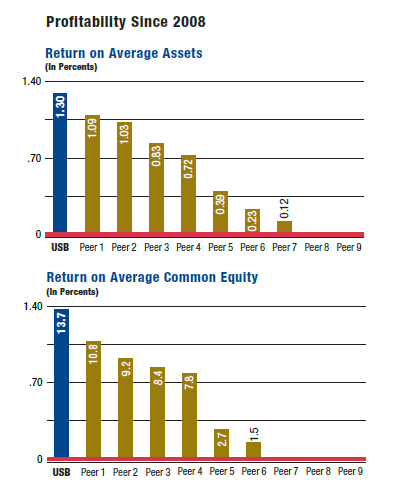

This report is to evaluate the performance of U.S. Bancorp from three aspects: liquidity analysis, asset quality and capital adequacy based on the financial report in past three to four years. Some key financial ratios of the bank will be included and compared with peer group companies in this report. U.S. Bancorp has recovered from economic recession quickly, maintained a good performance compared to the banks in the peer group. We believe that U.S. Bancorp will keep expanding and growing in the future.

Introduction:

U.S. Bancorp is a bank holding company that ascended to a top 5 position with $354 billion in assets at December 31, 2012 in the commercial banking industry.

United States

United States Figure 1

Figure 1At year-end 2012, the company operated 3,084 banking offices and 5,065 ATMs in 25 states. It has approximately 66,000 employees and global payments services to more than 17.6 million customers. U.S. Bancorp was named Fortune magazine's 2012 Most Admired Superregional Bank.

U.S. Bancorp provides various kinds of financial services, encompassing commercial and wholesale banking, wealth management, payment processing service and treasury/corporate services. A multitude of uncertainties kept many companies from applying for new commercial loans and encouraged others to defer spending and expansion in 2012. Despite those doubts and hesitations, for the full year, U.S. Bank grew average commercial loans and leases by 17.9 percent over the prior year, accelerating growth over the 9.8 percent increase in 2011. This growth was driven by customer organic growth and new customers. So, compared with competitors, U.S. Bancorp performed better during the negative...