Adjusting entries are mainly involved with the use of Accrual basis accounting. Accrual accounting provides a complete background for the operating performance of a business and its financial position. Overall revenue and expenses are recognized when they occur, this produces a relevant measure of profit and financial position, which can then be assessed as to whether the business is running at a profit or loss.

The purpose of adjusting entries is partly to correct errors, however also with the use of adjustments other aims are achieved. Adjustments are made to measure the profitability of a business, which is conducted by preparing financial statements (adjustments made prior to financial statements) at the end of each period . Through the use of adjusting the books (adjusting entries), the business can access profitability. Adjusting entries also helps to place revenues to the certain period in which it is earned and expenses to the periods it was incurred.

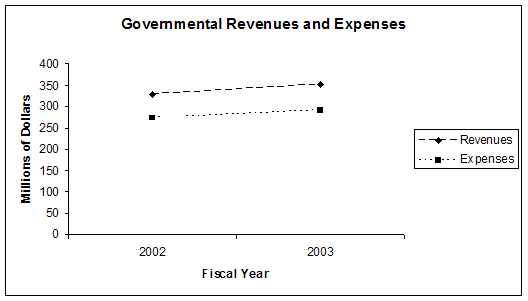

English: Seminole County, Florida Revenues and Exp...

English: Seminole County, Florida Revenues and Exp... Finance

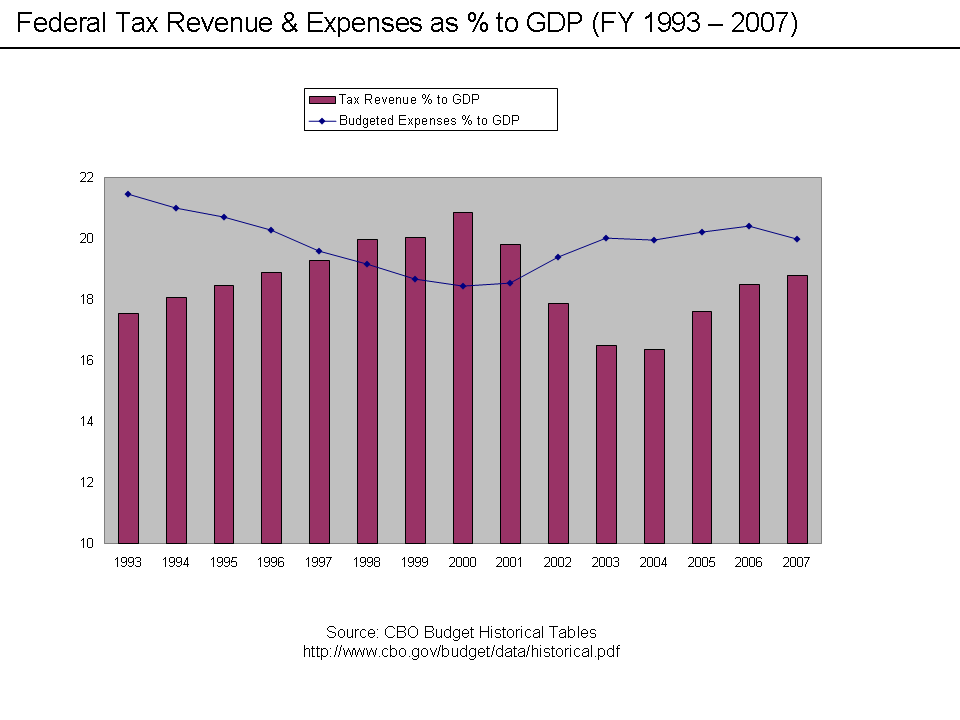

Finance Revenue and Expenses to GDP 1993-2007

Revenue and Expenses to GDP 1993-2007Also adjustments properly measure the periods of accrual basis profit in the statement of financial performance. The statement of financial position helps correct accrual basis balances in relation to relevant asset and liability accounts.

Adjusting entries can be divided up into five categories prepaid expenses, depreciation of non current assets, accrued expense, accrued revenue, and unearned revenue.

Overall, correcting errors in only one element of adjusting entries. Adjustments are used to measure revenue and expenses, in which a net loss or profit can be announced, therefore expressing the business financial performance. Also the assets and liabilities accounts are kept up to date and with adjustments there is evidence to suggest if a business statements are misleading.

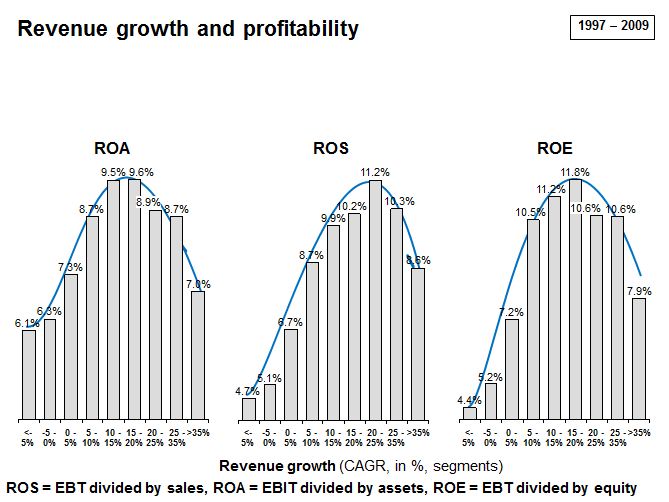

English: Revenue growth and profitability

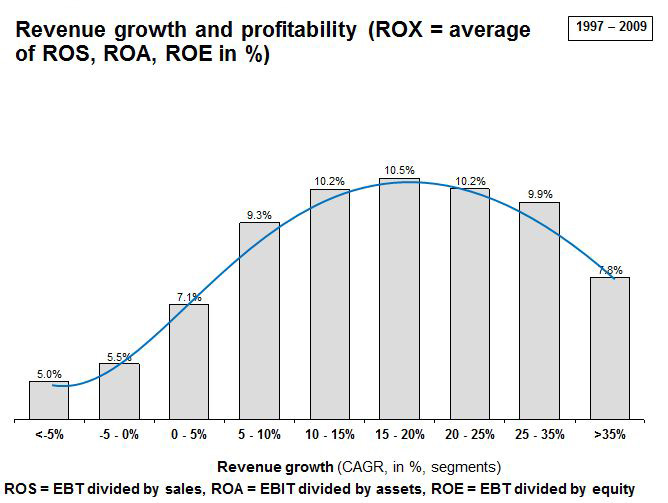

English: Revenue growth and profitability English: Revenue growth and profitability (ROX)

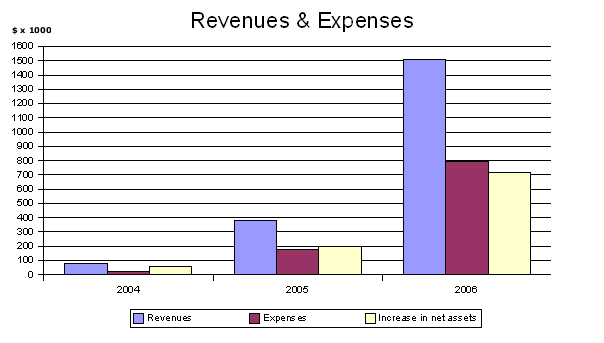

English: Revenue growth and profitability (ROX) Revenues and expenses

Revenues and expenses