The Underwriting Expense Ratio measures efficiency by comparing the amount of losses incurred while making a sale and issuing a policy to the amount of premiums for all policies sold in a certain accounting period. It calculates the percentage of written premiums that go toward paying expenses associated with a new policy before any claims are paid out. The smaller the numerator (underwriting expenses), the lower the ratio. Therefore, by minimizing underwriting expenses, a company can improve efficiency. Of the 4 companies I researched, Dakota Truck Underwriters were the most efficient in this area with a ratio of 19.5%. Drivers Insurance Company had the largest Underwriting Expense Ratio, despite having the lowest amount of underwriting expenses relative to the other 4 companies. However, their ratio was the largest because they had the least amount of premiums written. While calculating all 4 ratios, I found that the Daily Underwriters of America and Discover Property & Casualty Insurance Company did not have any Total Other Income.

English:

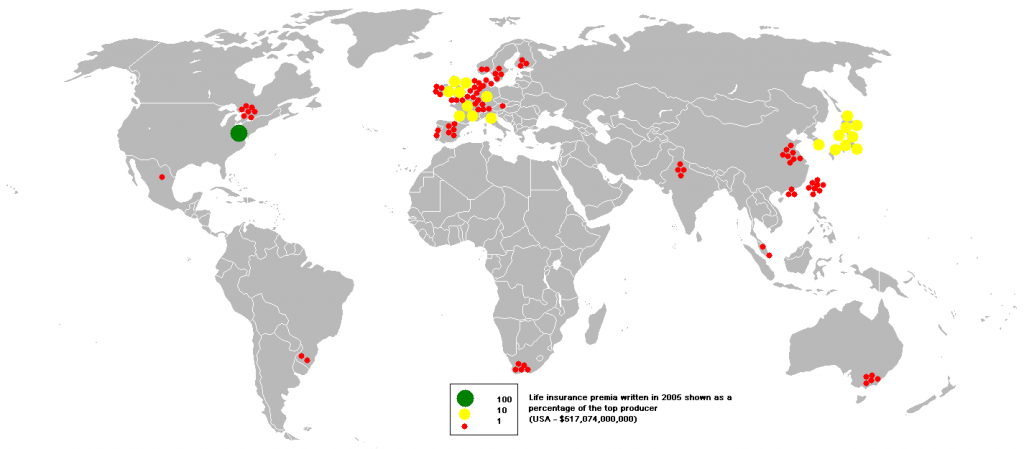

English: English: This bubble map shows the global distribu...

English: This bubble map shows the global distribu... insurance broker

insurance brokerPerhaps this is why their ratios were larger than Dakota Truck Underwriters.

The Loss Adjustment Expense Ratio also measures efficiency, but does so by calculating the percentage of earned premiums that are used to pay claim costs other than the claim itself. These consist of attorney's fees, acquiring expert witnesses for trial purposes, hiring a claims department, etc. Much like the Underwriting Expense Ratio, it is best to minimize this ratio by minimizing the amount of adjustment costs and maximizing the amount of earned premiums through sales. In my report, the Daily Underwriters of America did the best job at this task. And surprisingly, Dakota Truck Underwriters had the highest ratio. Each of the other 4 companies had a lower LAE Ratio compared to their Underwriting Expense Ratio. Dakota Truck Underwriters' was 3.6%...