Two common costing systems used in business are traditionally cost accounting system (job costing, process costing and operating costing) and activity-based costing system (ABC). There are some similarities and differences between these systems. Regarding the similarities, both accumulate product costs throughout the production process and assign those costs to individual units of production. Additionally, product cost under two costing systems consists of direct materials, direct labor and manufacturing overhead.

In terms of differences, they are different in the way how the overhead costs are allocated. For conventional costing, it assigns manufacturing overhead based on a single volume based cost driver such as direct labour hours. In contrast, ABC approaches cost from the perspective that products do not cause costs. It requires activities which are the causes of all costs incurred so it allocates manufacturing overhead according to the activities needed to produce the products. Therefore, it highlights the existence of non value added activity which is not existed under traditional method.

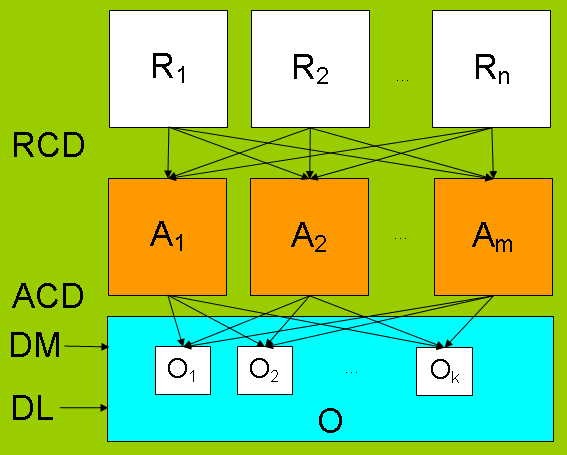

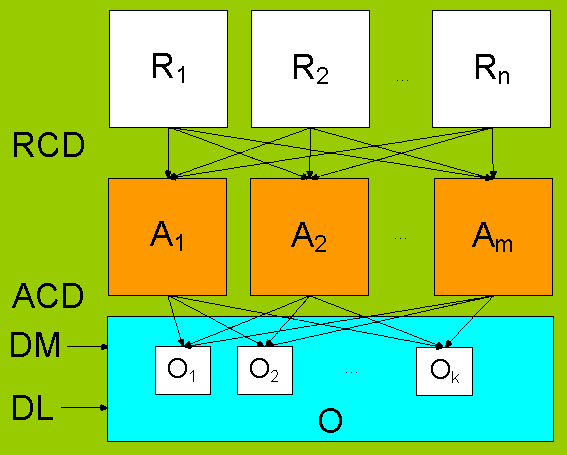

R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... Português: Um Mapa da Gestão de Programas Públi...

Português: Um Mapa da Gestão de Programas Públi...ABC also differs from conventional costing in the use of several cost pools when allocating the overhead costs. For instance, traditional costing uses only one cost pool to distribute the overhead whereas there are many cost pools involved under ABC. Furthermore, ABC employs both volume-based and non-volume-based cost drivers while conventional costing utilizes only volume-based cost drivers. Another difference is that conventional approach complies with the GAAP so it can be used to satisfy conventional financial reporting requirements. On the other hand, accounting standard board does not accept ABC to prepare financial statements so it can be useful for internal management decision.

Under conventional system, there are similarities between job costing, process costing and operating costing. Firstly, they accumulate product costs throughout the production process and assign those costs to products. Secondly, these costing...