Executive Summary Portfolio Bought a Portfolio 1000 of Cotton Futures On Nov 8th 2001 at $32.15 Primary Asset Value is (1000 X $32.15) = $ 32,150.00 Primary Asset Cost to me (Primary Asset Value X Margin Cost (6%)) = $1929.00 Sold 1000 of Cotton Futures on Nov 16th 2001 at $ 34.71 Primary Asset Value is (1000 X $34.71) = $ 34,710.00 Primary Asset Cost to me (Primary Asset Value X Margin Cost (6%)) = $2082.60 Bought CRC Futures 1000 on Nov 8th 2001 at 187.61 Primary Hedge Value (1000 X $ 187.61) = $ 187,610.00 Primary Hedge Asset Cost ($187,610.00 X 6%) = $11,256.60 Sold CRC Futures 1000 on Nov 9th 2001 at 189.03 Primary Hedge Value is (1000 X $ 189.03) = $ 189,030.00 Primary Hedge Cost ($189,030.00 x 6%) = $ 11,341.80 Entry and Exit Points on Primary Asset Market Entry Point on Nov 8th 2001 : 3215 Profit Exit Point : 3415 Loss Exit Point : 3015 Profit Analysis on Primary Asset Profit from Asset = Primary Asset Value at Sold - Primary Asset Value at Cost $34,710 - $32,150 Profit from Primary Asset = $2560.00

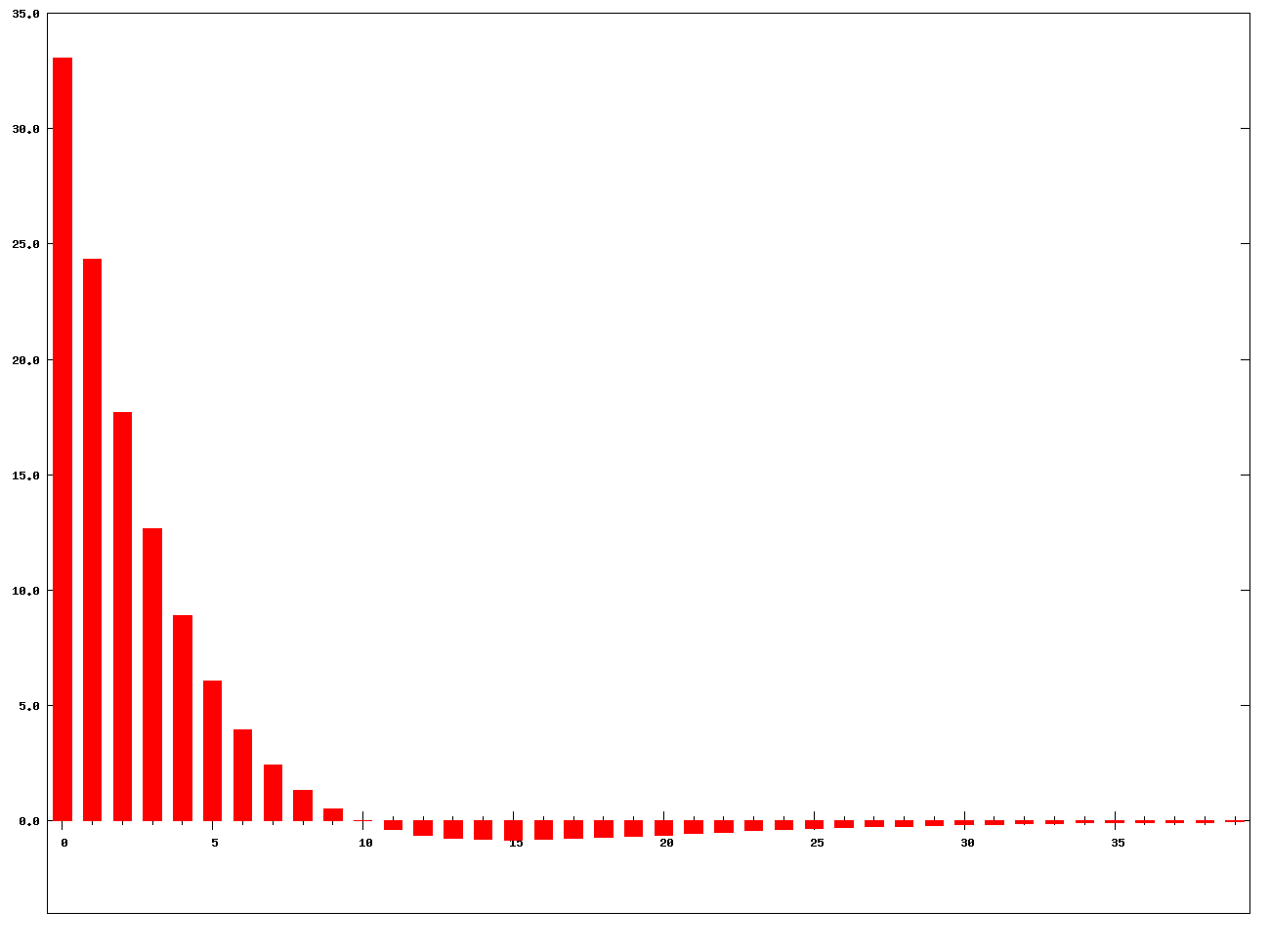

Double exponential moving average weightings N=10

Double exponential moving average weightings N=10 Golden Book Encyclopedias Vol. 4 - Chalk to Czecho...

Golden Book Encyclopedias Vol. 4 - Chalk to Czecho... Arizona, land in transition

Arizona, land in transitionPrimary Asset Holding Period Return Hold Period Return = Primary Asset Profit X (360 days / No. of holdingdays) ------------------------ Primary Asset Cost Hold Period Return = 9555.20 % Hedging Analysis For Hedging purpose we will use CRC Futures as it includes Soybean futures Hedge Asset Holding Period ReturnHolding Period Return = (189,030.00- 187,610.00)/ 11256.60 x (360/1) Holding Period Return = 4541.3357% Total Portfolio Holding Period Return: Total Portfolio Profit $ 2560.00 ---------------------------- --------------= Total Portfolio HPR 1398.24% Total Portfolio Cost $13,185.60 Cotton Futures: Cotton Futures are being traded for last couple of years because of the scarcity of cotton due to high demand of cotton for textile...