1.0 INTRODUCTION

Many decades have passed since Eugene Fama introduced the idea of an "efficient" stock market to the financial academic world; even today it still provides an insight to stock market efficiency but still it continues to cause controversy. Everyone wants to know whether the stock market is efficient in pricing shares and other securities including investors, businessman and academics. The idea that by studying in this area they might be able to discover a stock market inefficiency which is sufficiently exploitable to make them rich, or as a minimum, to make their name in the academic community. There has been extensive research on the subject of stock market efficiency I intend to look at this so I can find out weather the stock market is efficient or if there are any inefficiencies which could be exploited. The final outcome of this paper should give an answer as to weather stock markets present investors with the opportunity for abnormal gain

Stock market of Brussels

Stock market of Brussels Daniel Kahneman

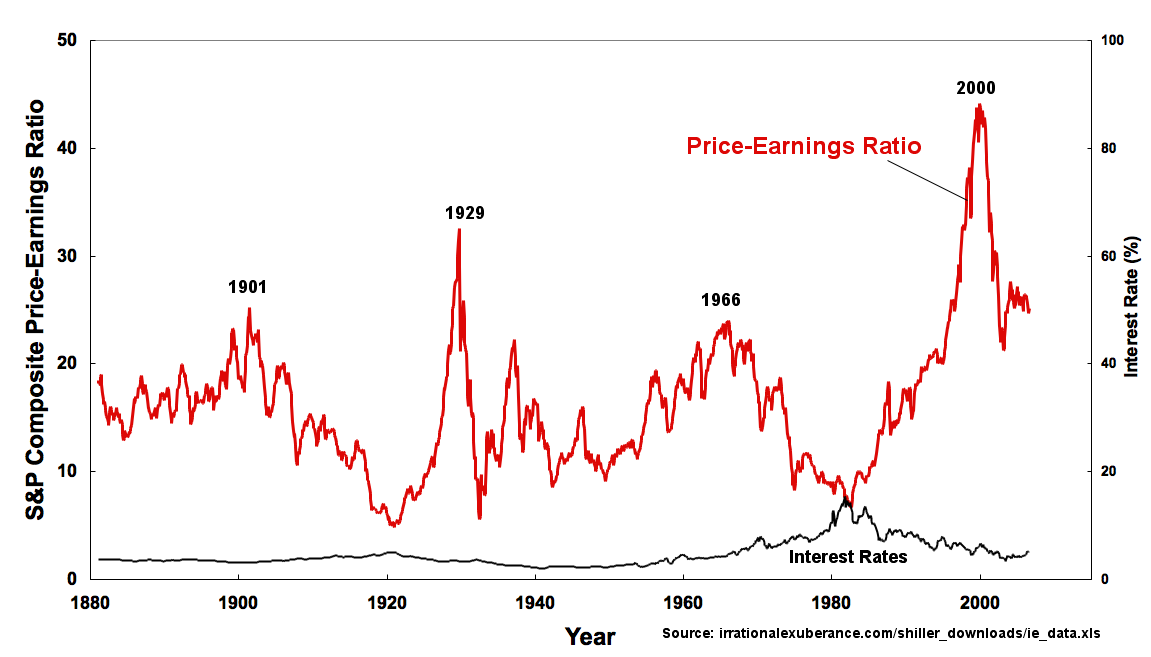

Daniel Kahneman Plot of S&P Composite Real Price-Earnings Ratio an...

Plot of S&P Composite Real Price-Earnings Ratio an...1.1 THE BEGINING

The idea that security prices in an organised market might follow a random walk was first put forward by Louis Bachelier in 1900 for commodities traded on the French commodities markets (Rutterford, 1993:282). Early work dates back to 1953 when Maurice Kendall presented a paper which looked at security and commodity price movements over time. He intended to find regular price cycles, but was unable to do so. The prices of shares moved randomly and today's price could not be predicted by looking at the previous day's price changes.

This finding was confirmed by Fama (1965). He studied the daily proportionate price changes of the thirty industrial stocks in the Dow Jones Average for approximately five years. He discovered the serial correlation coefficients for the daily changes to be small, the average being 0.03 (Rutterford, 1993:285).