ension AccountingPension accounting is an issue that has been delayed, debated and, in many respects, is still unresolved in terms of implementation. The Financial Accounting Standards Board (FASB) released Statement of Financial Accounting Standards No. 132, and it is the most recent pronouncement regarding pension accounting. However, before the issuance of SFAS 132, there were other statements used for the accounting of pensions.

History under Prior StandardsThe FASB's Statement of Financial Accounting Standards No. 87, Employers' Accounting for Pensions, was published in December 1985. The major provisions under this standard is measuring the cost and reporting the liabilities resulting from defined benefit pension plans. In 1956, the Committee on Accounting Procedure concluded that improvements in pension accounting were necessary beyond what was considered practical at those times. In 1966, the Accounting Principles Board (APB) agreed. Later, information about pensions and their importance grew, and there were increases in the number of plans and amount of pension assets and obligations.

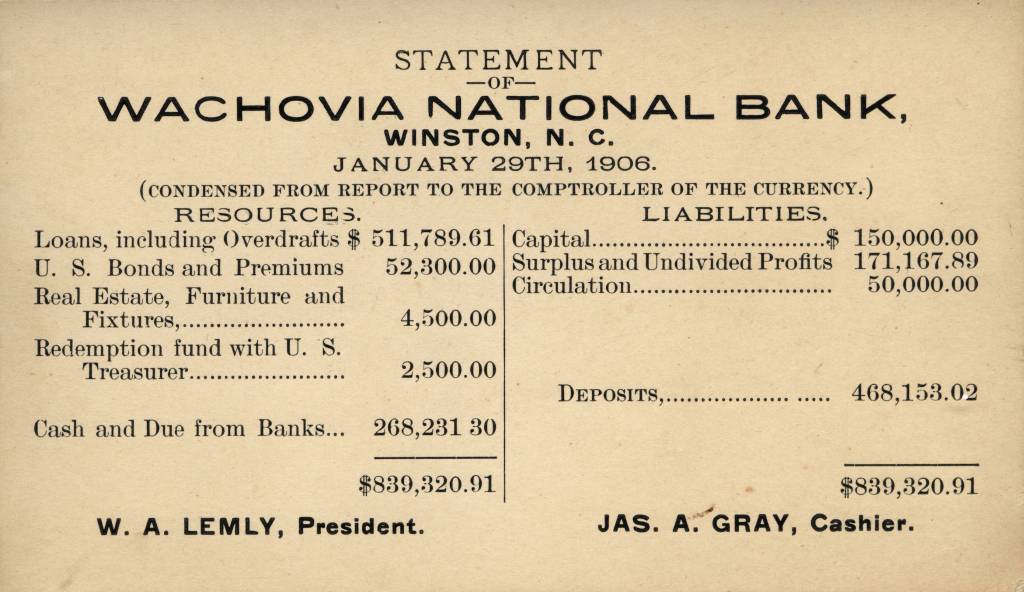

Historical financial statement

Historical financial statement English: BoT and BoE financial statement 2010 meet...

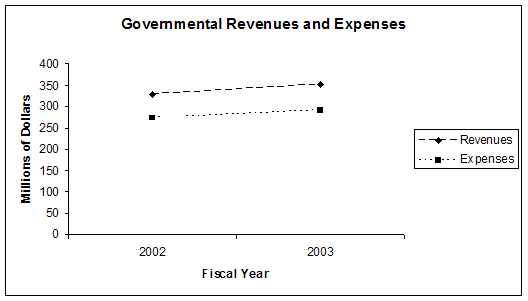

English: BoT and BoE financial statement 2010 meet... English: Seminole County, Florida Revenues and Exp...

English: Seminole County, Florida Revenues and Exp...Statement of Financial Accounting Standards No. 87 requires the recognition of pension expense. In addition, recognition on the balance sheet is required for a portion of the pension-related assets and liabilities. Before the issuance of SFAS 87, some companies were already recognizing pension expense using accrual-basis accounting. However, SFAS 87 did significantly improve accounting for pensions. The FASB then issued SFAS's 132 and 132(R) to improve the disclosure requirements for pensions (Soroosh, Espahbodi, 2007).

Highlights of SFAS 132The major foundation of Statement of Financial Accounting Standards No. 132 is disclosure of pensions and other postretirement benefits; measurement and recognition are not addressed. There are certain disclosures than an employer must reveal if the employer sponsors one or more defined benefit pension plans (FASB, 1998).

According to the FASB's SFAS No. 132, employers are required to explicitly report benefits paid and contributions...