1.9.1 Introduction

The long-term survival of a firm seems to be dependent more on the firm's competitiveness. No matter how much physical, human and intellectual resources, an organization is able to mobilize, its long-term survival will be in jeopardy if it fails to stay competitive. The firm therefore needs to be able to determine its level of competitive advantage vis-a-vis that of its competitors and also be in a position to improve and sustain it. Normally an organization will set up a marketing intelligence to monitor its competition. This literature review will include an examination of the extent to which financial tools and technique can be used to supplement or complement the traditional marketing intelligence system. It will also examine existing models used to analyze the financial health of a firm and try to determine the extent to which these tools could reveal a company's competitiveness.

1.9.2 Definition of Terms

Historical financial statement

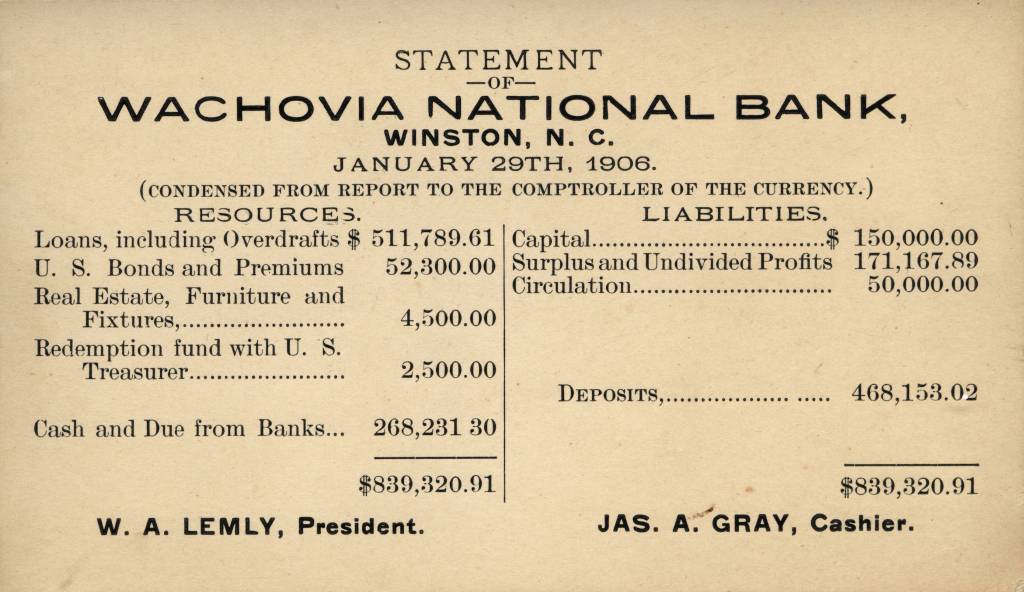

Historical financial statement English: BoT and BoE financial statement 2010 meet...

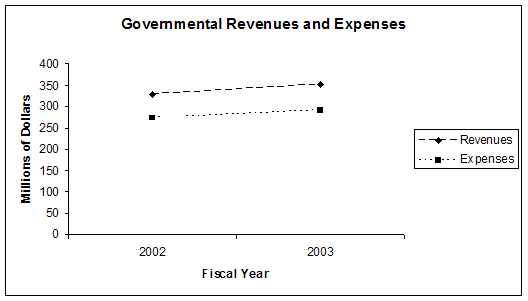

English: BoT and BoE financial statement 2010 meet... English: Seminole County, Florida Revenues and Exp...

English: Seminole County, Florida Revenues and Exp...This study covers the Mining industry and in particular, the gold Mining Industry. According to Kotler, P. (2003) an industry is a group of firms that offer a product or class of products that are close substitutes, for one another. According to him industries are classified according to factors like the number of sellers, the extent to which the product is differentiated, whether entry and exit barriers exist, the cost structure, degree of vertical integration and finally the extent of globalization. The study also covers contract-mining firms. Contract Miners are organizations with civil engineering backgrounds and who use heavy excavating and conveyance machinery to drill, blast and move rock, stones, gravel and top soil on behalf of Mining companies. By Mining companies, this study refers to firms that have obtained mining lease titles from the government and are entitled to mine and process minerals under laws of Ghana.

1.9.3 The concept of competitive Advantage

According to Porter, M. (1985) the first basic determinant of a firms profitability is industry attractiveness and the rules which affect the level of attractiveness are as follows:

* The entry of new competitors

* The threat of substitutes

* The bargaining power of buyers

* The bargaining power of suppliers

* The rivalry among existing competitors.

According to him the aim of an organizations competitive strategy should be to recognize and cope with these rules as well as influence those rules in the firms favour.

Commenting on these five rules, Kotler, P. (2003) is of the view that these rules pose threats to a firm. One of the threats as viewed by Kotler is worth mentioning. According to him a segment is unattractive if there exist numerous or aggressive competitors, if the segment is stable or already declining, if there are high entry and exit barriers or if competitors have high stakes in staying in the segment.

Porter, M. (1985) again outlined two basic types of competitive advantage a firm can possess as low cost and product differentiation which can be combined with scope to produce three generic competitive strategies, namely:

* Cost leadership:

* Differentiation

* Scope

Porter distinguished cost leadership as perhaps the clearest of the three generic strategies. Using cost leadership a firm seeks to dominate its market segment by becoming a low cost producer using its costs advantage in economy of scales, proprietary technology or preferential access to raw materials.

It is crucial to note here that cost is a prime source of competitive advantage. Since costs is measurable to a large extent and can thus be easily reflected in a firm's financial statement, this study will accordingly be assessing the extent to which financial statements relate to competitiveness. The study will also seek to identity models that could represent this relationship.

Porter, M. (1982) was also of the view that a generic strategy does not lead to above average performance unless it is sustained vis-Ã -vis competitor's actions. He added that the sustainability of the three generic strategies requires that an organization's competitive advantage resist erosion by competitors' action or industry evolution.

1.9.4 The Role Of Competitive Intelligence Systems

According to Kotler, P. (2003), markets have become so competitive that it does no longer suffice for firms to concentrate mainly on satisfying the customer. It is his strong belief that organizations must start paying keen attention to the actions and inactions of competitors. He concludes that successful companies now take to designing and operating competitive intelligence systems. Kotler has distinguished four steps to setting up an intelligence system as: setting-up the system, collecting data, evaluating and analyzing the data, and disseminating information and responding to queries.

The traditional marketing intelligence system has remained largely qualitative, paying much less attention to quantitative data. This study will attempt not only to be quantitative but will also attempt to develop models based on financial statements which will serve as benchmarks for assessing and predicting competitiveness.

1.9.5 Financial Management Tools and Techniques

Writing about functional level strategy, McNamee, M. (1985) argued that although knowledge of all functional areas of the organization is necessary for a comprehensive understanding of strategy, the finance function is unique as it serves both as an instrument of strategic analysis as well as a creative strategic tool. He developed this further and concluded that from the perspective of Strategic Management, finance has two linked major roles of control and creativity. As a control Financial Management can be used to implement, monitor and evaluate a business strategy and creatively, finance can be used to power an organization towards its objective and to give the firm advantages over its competition.

1.9.6 Financial Statement Analysis

A company's financial statement enables stakeholders to know where the company stands at a particular time and consequently predict where the company could be in the future. An organization's financial statement consists of the Balance Sheet, the Income Statements, Statement of Source and uses of funds and finally notes and explanations attached to the statement.

The term financial statement analysis, sometimes also referred to as financial performance evaluation, describes all the techniques employed by users of financial statements, to show important relationships in the financial statements and the trend the figures there-in contained tend to exhibit.

The objectives of financial statement analysis are to assess the historical operating performance and financial health of a supplier, customer or competitor.

It also facilitates the understanding of the economics of a firm in order to fore cast its future increase in wealth and risks.

In order to aid an extensive analysis and understanding of financial statements, analysts normally adopt various techniques of comparison generally referred to as bench marking. These bench markings occur at three levels namely: the level of the firm where comparison can be made with past data, future data and even budgeted data, at an inter-company comparison level and finally at an entire industry level where comparison is done with computed industry average.

(a) Tools and Techniques of Financial Analysis

In order to produce order out of chaos or to make mere numbers tell a story, financial analysts have devised tools, which tend to show relationships between numbers and their changes from year to year.

There is no need to over-emphasize the fact that financial accounting literature is one of the least impoverished in terms of volumes of writings on financial analysis tools and techniques. Perhaps, the only comment worth making is that different writers slightly different on the classification of these tools. An interesting classification that this study will adopt is horizontal analysis, trend analysis, vertical analysis and ratio analysis.

In horizontal analysis changes in like items are computed form one year to another. It begins with the computation of changes, from the previous year to the current year, the base year being the first year considered. The cedi amount of change is the divided by the base period amount and converted into percentage if necessary:

Percentage change = 100 x (Amount of Change)

(Base year amount)

Trend analysis is similar to horizontal analysis. The difference is that in trend analysis the number of years being examined is more that one. In trend analysis a base year is selected whose figures are set equal to 100 percent. Each subsequent year's like items are divided by those of the base year. Trend analysis is important as it could reveal changes in the nature of a business. The calculation of trend analysis is illustrated below:

Trend % = Any year Amount

Base year Amount

Another class of financial tools and techniques is the vertical analysis. It is sometimes referred to as a common-size statement. In vertical analysis, the analysts sets a total figure in the statement equal to 100% and computes each components as a percentage of the total. Vertical analysis helps the analyst to compare the level and significance of a particular item within the enterprise and can also compare its changes form one year to another. As a matter of convention, sales is normally used for income statement items and fixed assets are used as base for the balance sheet items.

The last but not the lease set of tools is ratio analysis. It is the most widely known and used technique in financial analysis. A financial ratio is a relationship expressed between two accounting figures mathematically. Their prime advantage lie in the fact that they enable analysts to compare different companies of different sizes. However the purpose of ratios is to point out areas that need further investigation. Financial ratios could be sub-classified as follows:

* Ratios that measure the risk of not meeting current liabilities, are normally referred to as liquidity ratios.

* Activity ratios, which measure the level of activity by determining ability to dispose inventory, and collect the associated debts.

* Solvency Ratios that measure the firms ability to meet long-term debts

* Ratios that measure profitability

* Investment ratios that measure and evaluate a company's shares

Financial analysis tools, though considered as the most objective and quantitative analysis of a firm's financial position, do have limitations in application. It is important to point out from the outset that relationships or findings revealed by these tools should be considered as pointers that require further investigation and follow-ups. It is also worthy of note that the accounting profession, despite increasing regulation, still has a lot of lee ways in reporting accounting data. For example book values as against market value are used. Also accountants have discretion in the way they treat intangible assets such as patents and franchise.

b) Costs and Cost Behavior

The term costs refer to a quantified amount expended in acquiring goods and services. There are various types of costs and equally numerous classification of such costs. Kwame Gyasi (2004) has provided some basis of classification of costs as follows: natural classification, relationship to production, relationship to volume or activity, period charge against revenue, classification for planning and control and classification for decision making.

Among the various basis of classification, relationship of costs to volume or activity provides the best understanding of costs behaviors to the Accountant and the Financial Manager.

A basic classification of costs in relation to volume is variable costs, fixed costs and semi-variable costs. Those costs, which tend to vary in direct proportion to volume, are classified as Variable Costs. On the other hand, fixed costs refer to costs which are constant within a certain range of output. Semi variable costs are those costs, which combine the characteristics of fixed, and variable costs.

The basic financial management tools and techniques, which utilize the concept of cost behavior, are classified as Cost-Volume-Profit Analysis (CVP Analysis). The CVP Analysis is defined as the examination of costs behavior patterns that underlie the relationship amongst costs, volume of output and profit. These techniques include Marginal costing and Break-even Analysis. It is an objective of this study to explore the extent to which Mining Sub-contractors utilize the CPV Analysis and techniques to achieve competitive advantage.