INTRODUCTION

Realised-profit, matching-based, historical cost accruals accounting (HCA) has for over fifty years been repeatedly challenged as being an inadequate basis for the measurement of "income" which reports increments in the value of businesses. Such challenges continue unabated and are made by both accounting standards regulators and by academic commentators. Despite its obvious deficiencies for measuring valuation based income, and subject to concept of prudence, internationally HCA remains the dominant basis for reporting and share prices appear to be influenced by reported earnings.

This paper will go through few criticisms of our standard accounting model, look at possible alternatives and finally will provide a detailed explanation of why Historical Cost accounting is still the conventionally used method.

What are Historical Costs?

Historical cost is a generally accepted accounting principle requiring all financial statement items be based upon original cost. Historical cost means what it cost the company for the item.

Delavan’s Historic Brick Street Historical Marke...

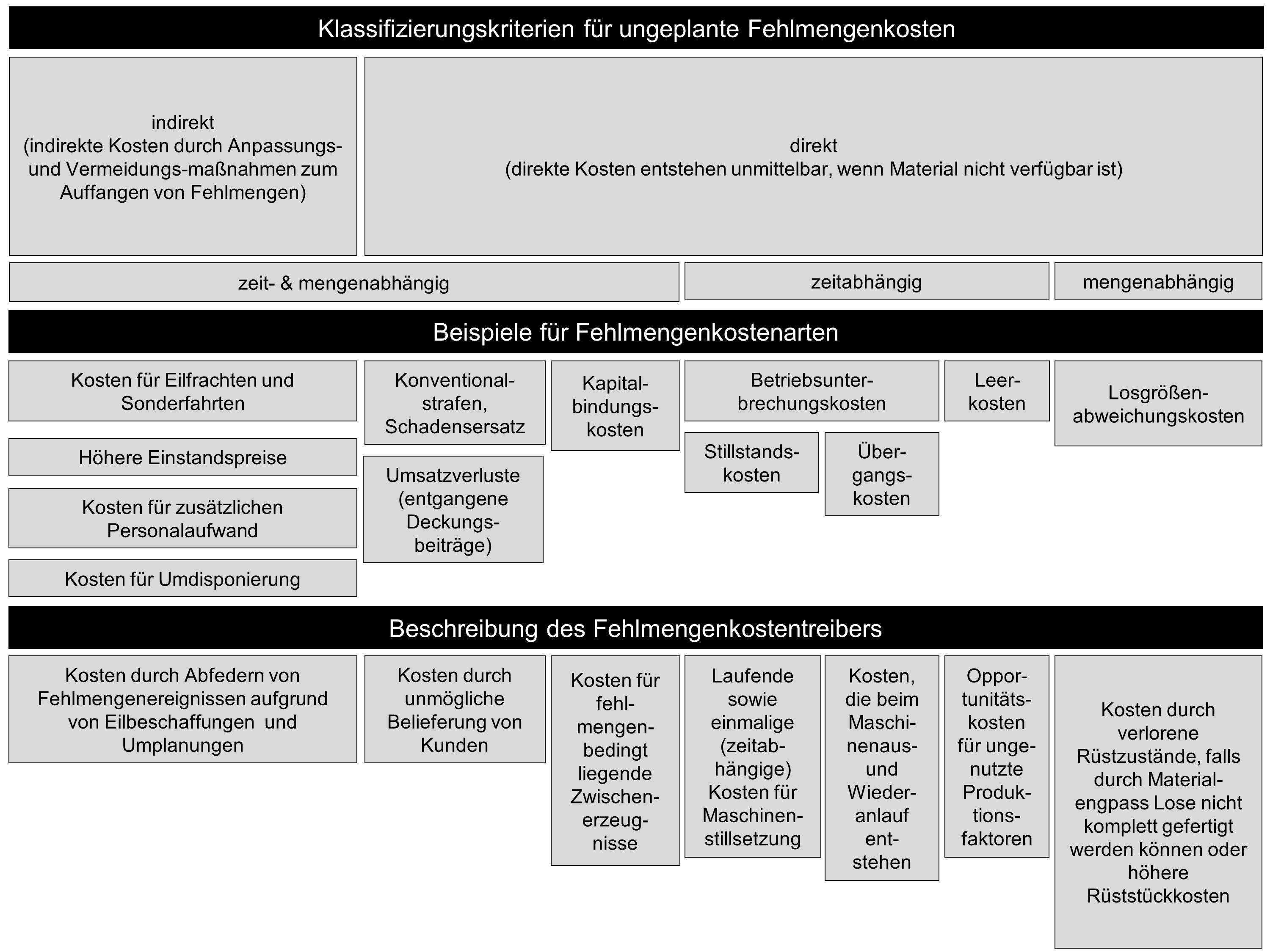

Delavan’s Historic Brick Street Historical Marke... scheme, classification of out-of-stock cost, short...

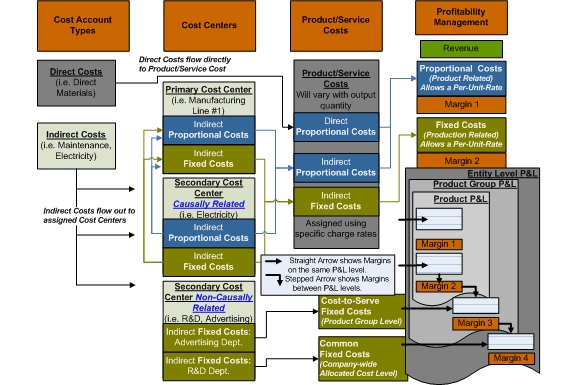

scheme, classification of out-of-stock cost, short... English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr...It is not fair market value. This means that if a company purchased a building, it is recorded on the balance sheet at its historical cost. It is not recorded at fair market value, which would be what the company could sell the building for in the open market.

The role of 'Stewardship'

It is a widely held view that the prime objective of the preparation and publication of regular financial reporting is - so far as public limited companies are concerned - to provide a vehicle whereby the directors can account to the owners of the company on their stewardship of the resources entrusted to their charge (Page 57,Lewis & Pendrill, 2000). Historical Cost accounting adequately helps the Directors to report to the Shareholders of how well their funds or company's resources have been used. A typical historical cost balance sheet will list the company's assets and...

Good essay.

This essay is very informative and nicely structured. Very helpful. Thanx.

5 out of 5 people found this comment useful.