Adia owns a house and has an elderly third cousin living with her. Adia decides she needs fire insurance on the house and a life insurance policy on her third cousin to cover funeral and other expenses that will result from her cousin's death. Adia takes out a fire insurance policy from Ajax Insurance Co. and a $10,000.00 life insurance policy from Beta Insurance Co. on her third cousin. Six months later, Adia sells the house to John and transfers the title to him. Adia and her cousin move into an apartment. With two months remaining on the Ajax policy, a fire totally destroys the house, at the same time, Adia's third cousin dies. Both insurance companies tender back premiums but claim they have no liability under the insurance contracts, as Adia did not have an insurable interest.

Insurable interest can be established through either pecuniary (monetary), or relationship.

John_Deere_4630_Tractor.jpg

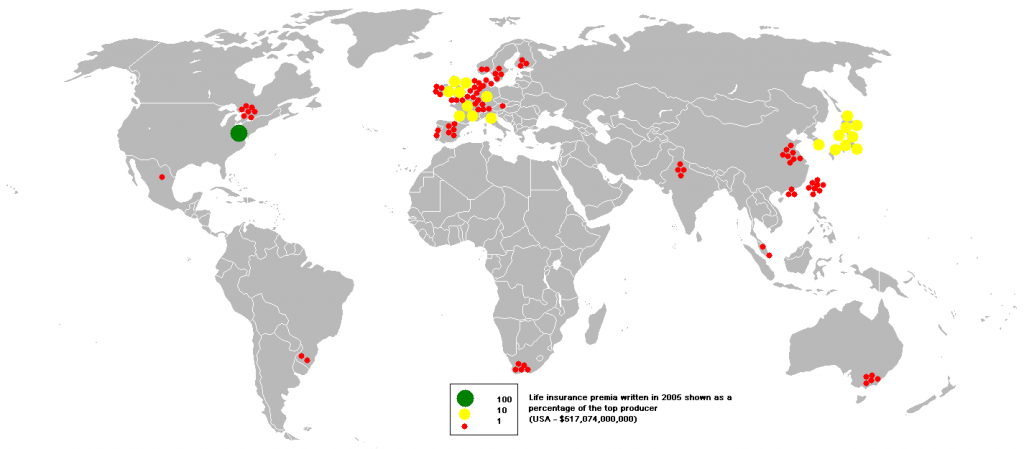

John_Deere_4630_Tractor.jpg English: This bubble map shows the global distribu...

English: This bubble map shows the global distribu... insurance broker

insurance brokerPecuniary interest can be established by ownership or interest in property either personal or real. Individuals may insure property that they have an insurable interest in.

Insurable interest based in relationship can be established through either close blood relation or affinity. This prevents life insurance from being used as a gambling tool. If persons could simply insure strangers then the possibility of gambling on the life span of another could become an issue.

Blood relations can be parents and children, brothers and sisters, grandparents and grandchildren, and husbands and wives. Life insurance policies are based upon an insurable interest that must exist at the time the policy is issued. Therefore, if spouses divorce, unless the policy contains a clause to terminate upon divorce, the policy may be maintained.

Affinity can be established by demonstrating an interdependency or reliance of either party. This is most easily demonstrated through businesses that insure...