A very good, detailed essay about International Accounting Stds. My instructor said it was the best paper that year

Internationalization of Accounting Standards for Consolidation

Japan: A Case Study

The purpose of this paper will be to examine problems with internationalization of accounting standards for consolidations on methods from an international perspective - specifically, in the US and Japan. This is an especially timely topic as standardization of financial markets is a prerequisite to international free trade. Given the trends toward greater globalization, the motivations of companies for seeking a uniform accounting system are strong. If companies have to prepare their accounts according to several different sets of rules, in order to communicate with investors in the various capital markets in which they operate or for other national purposes, they incur a considerable cost penalty and feel that money is wasted. This significantly limits global opportunities for multinational businesses. Thus, it is important to understand what the differences are between accounting standards, why they exist, and what problems they pose.

The western front of the United States Capitol. Th...

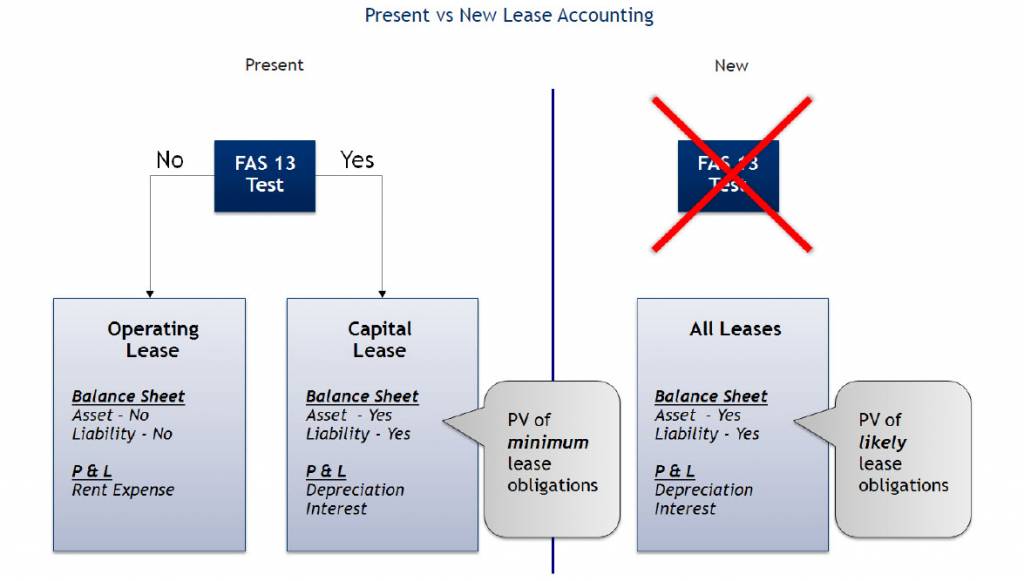

The western front of the United States Capitol. Th... English: Present vs. New Lease Accounting Standard...

English: Present vs. New Lease Accounting Standard... United States Capitol, Washington, D.C., east fron...

United States Capitol, Washington, D.C., east fron...It is worth noting that no one nation has a set of accounting rules which appears to have such clear merits that they deserve adoption by the whole world. No one country can claim to have a uniquely correct set of rules. The United States has the longest history of standard setting. It has the largest standard setting organization which is characterized by high standards of professionalism. But, even the rules of the United States exhibit compromises between different interests of a kind which could have reasonably been decided otherwise. Furthermore, no unanimity exists among U.S. accountants about the merits of the precise details of the compromises that have been struck. For example, the recent discussion memorandum on consolidation outlines three different methods which are GAAP in the US (Beckman,

...Accounting Standards...

This is one of the best papers in this category. It is informative, thorough, well-written, and well-researched. It is obvious that the author put time and effort into researching the topic and stated it clearly.

I recommend this paper to everybody who is studying this topic, it is an excellent research tool.

Excellent Job.

1 out of 1 people found this comment useful.