Leslie Fay Case

1. After reviewing the common size financial statements and the key ratios of Leslie Fay, there some of the financial statement item that should have been of particular interest to BDO Seidman:

1).Sales: the sales has been growing steadily except the slight drop in 1991, which is contrary to the industry recession.

2). Inventory: Leslie Fay has been known for not catching up the fashion, there should be inventory write-off issue in the apparel industry, which haven't been reflected in the inventory account though.

3) A/R: always a highlight because of its nature of hiding fraud

4). Other assets account: the current and quick ratio of Leslie Fay is significantly higher than the industry norm.

5). Liability account: A/P and debt, to see if understated.

2. Other financial info that the auditor might have obtained:

1). The contract or agreement of Leslie Fay and department stores to verify the A/R and liability

English: USA charitable giving 2009. Data sourced ...

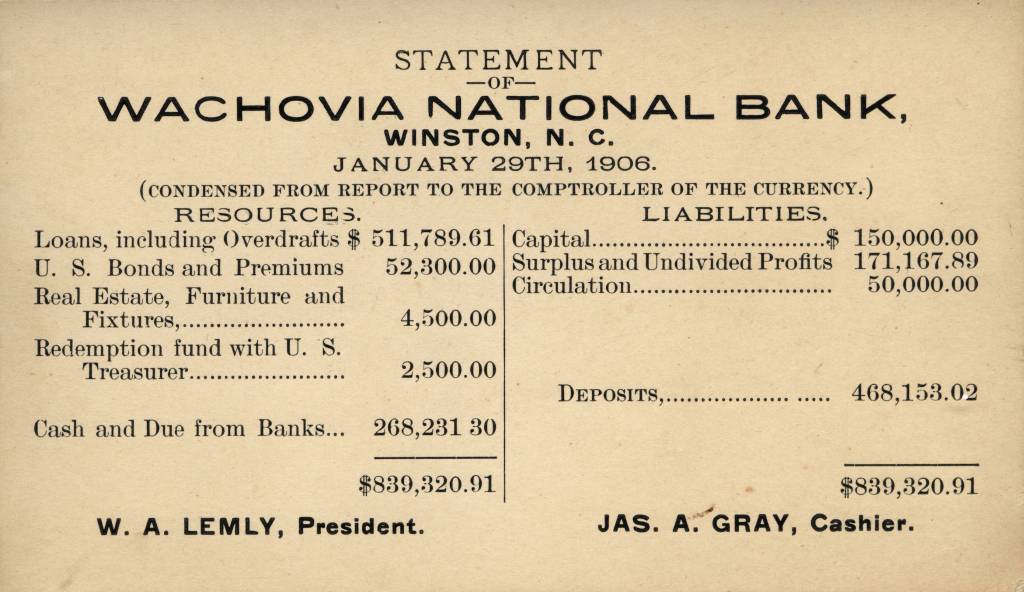

English: USA charitable giving 2009. Data sourced ... Historical financial statement

Historical financial statement BDO Seidman

BDO Seidman2). Documentation with its customer regarding its orders

3). Its credit and bad debt write-off policy

3. Non-financial factors the auditor should consider:

1). The industry

2). Impact of economy on this particular industry and company

3). The company's structure, history and personnel

4). Government regulations that have influenced or will show the effort on the company

4. Paul Polishan's dominance has two-fold implications on the audit:

1). Suppose he's a morally-impeccable person who did everything right and held high integrity and responsibility towards the company, his dominance still shows an internal control weakness which lack the segregation of duties. Such system is prone to the fraud and if Mr. Polishan is sick or absent from work for whatever reason, the finance department might not function well.

2). Mr. Polishan's dominance explained the fraud he perpetuated and hid.

The audit should take this into...