Many economists thought that when the U.S. housing boom ended, so would the overall economic boom. Yet housing starts and sales are down from peak levels, and while various reports indicate housing prices are still ahead of year-earlier levels, that masks the fact prices indeed have declined over the past six months. So why has the decline in housing not yet reduced the GDP and real growth rate of the U.S. economy? A declining housing market can negatively affect the economy in three ways. First and most obvious, there are fewer construction workers, fewer purchases of construction materials, and reduced income for brokers. Second, home-equity refinancing is reduced as prices level off and then decline, which, in turn, reduces consumer spending. Third, defaults and foreclosures increase, not only wiping out individuals who bought more house than they can afford, but many financial institutions as well. It is the third effect that will finally bring the economy down.

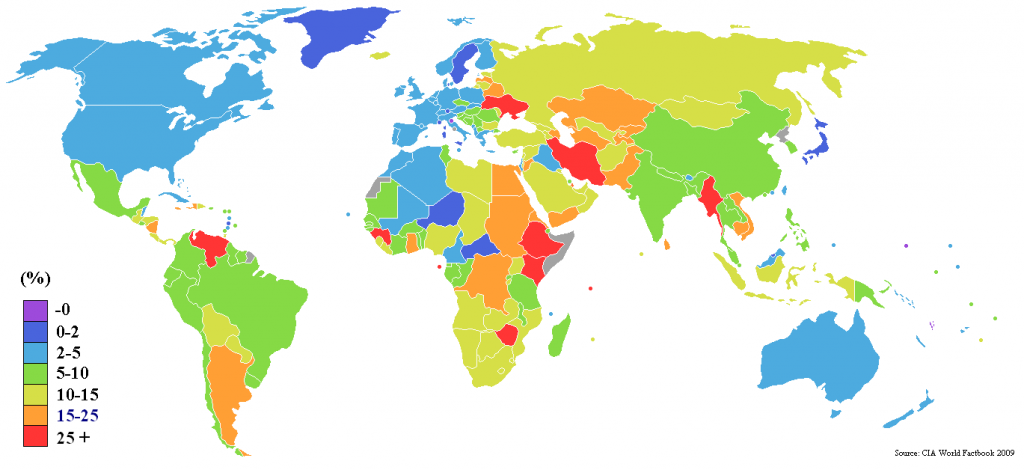

World map showing inflation, updated for 2009. Gre...

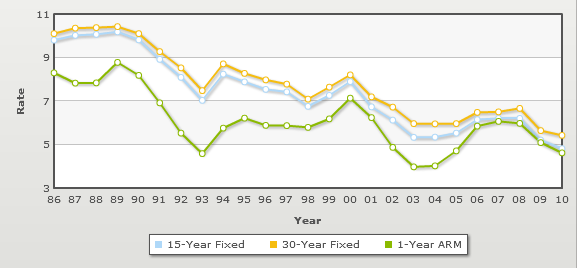

World map showing inflation, updated for 2009. Gre... English: Mortgage rates historical trends

English: Mortgage rates historical trends Inflation

InflationThe good news, it won't happen for several years, well past our ability to forecast. The rash of defaults and foreclosures usually peaks about three years after interest rates rise and housing prices level off and then decline (Evans, M. 2006). History has proven this to the economy, this current process of interested rate hikes started in 2005, suggesting that, the major negative impact of a declining housing market will not his until 2008. There will be some modest decline in the real growth this year and next, but an increase in real GDP (BEA, 2006).

GDP slowdown may give Fed pause, according to businessweek.com (Englund, M. MacDonald R. 2006). The U.S. economy grew at a disappointing 2.5% rate last quarter, raising market expectations that the Fed will suspend interest rate hikes. U.S. gross domestic product for the quarter underperformed. The underperformance of...