PROFORMA FOR WRITTEN PART

1. Direct material efficiency variance

The firm was faced with limited storage space at their premises and were unable to relocate or rebuild their premises or use Just-In-Time inventory. Therefore storage costs increased; this increased the DMs costs since storage is part of in-transit costs, which are considered part of DMs cost. Thus, the Materials Efficiency Variance calculated as $800 unfavourable.

DL efficiency variance

Change in the layout of the manufacturing space should reduce the standard time per product in the long run. Besides, new materials are easier to work with in terms of both cutting and sewing, which means workers spend less time. This is reflected in a favourable calculation of LEV at $950.

Variable OH Efficiency Variance

Variable OH efficiency variance was a favourable amount of $150. There were two key reasons for this. The first is that there was a change in the layout of the manufacturing space, which reduced the standard time per product.

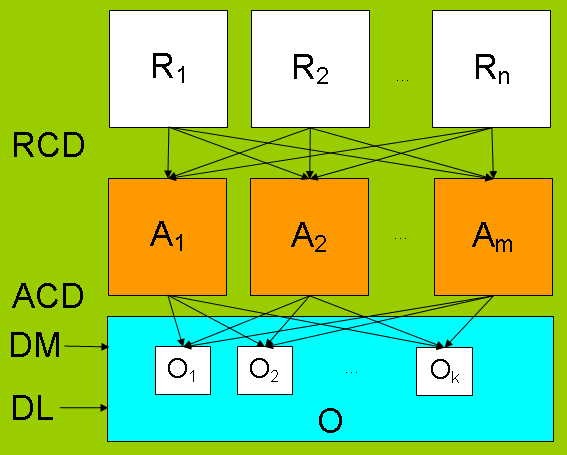

R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... R = resource-catagories RCD = Resource Cost Driver...

R = resource-catagories RCD = Resource Cost Driver... Português: Um Mapa da Gestão de Programas Públi...

Português: Um Mapa da Gestão de Programas Públi...The second reason was that a new material was used, which was easier to work with in terms of cutting and sewing, leading to less labour hours spent per unit. Ultimately this means less variable OH is spent as variable OH used DL as the cost driver.

2. Improvement (1)

The only material that is considered as a DM is fabric .The other materials are treated as indirect materials and are treated as OH. Using traditional costing, the total of the OH costs will be calculated accurately, however when allocating the amount of OH to each product the amount of each individual indirect material will not be allocated accurately. If each material is treated as a DM, the amount of material per unit will be costed more accurately as they will be based on actual...