Financial statements are a necessity when it comes to businesses. They are used by both internal managers as well as outside users and provide information about the entire company. Managerial accounting is primarily used by individuals within a company or organization. The main purpose of financial accounting is to prepare financial reports that provide information about an organization's performance to external parties like creditors, investors and tax authorities (Hilton, 2006).

There are several key differences between both managerial and financial accounting. The first key difference is in the purpose of each method. For example, managerial accountings' purpose is in decision making and the control of information while financial accountings' purpose is more general, as it used to provide general information for credit and investment decisions. Another key difference between the two types of accounting is frequency of preparation. In managerial accounting, reports can be created for any period of time (i.e.

Finance

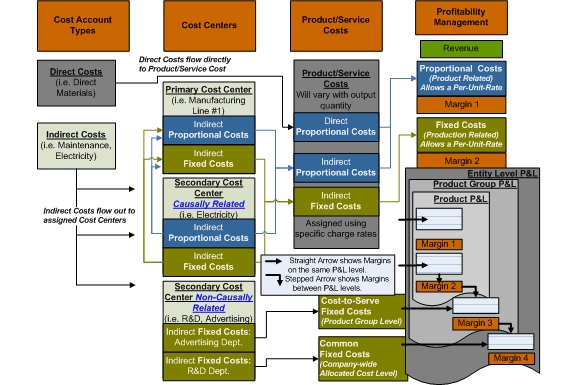

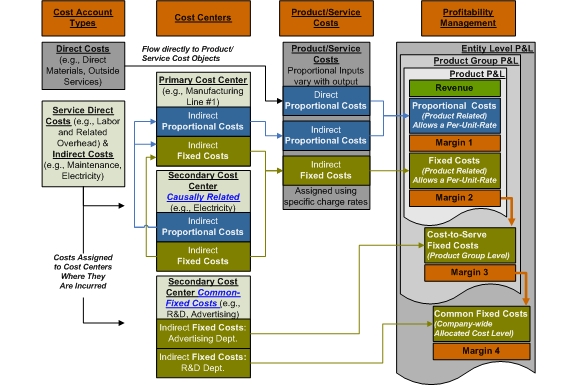

Finance English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr... English: GPK Marginal Costing Structure Flow of Gr...

English: GPK Marginal Costing Structure Flow of Gr...- daily, weekly, monthly). Financial reports are usually generated for a set period of time, such as fiscal year. Managerial accounting reports are prepared utilizing scientific and statistical methods to arrive at monetary values (Financial, 2007). Examples of these reports include sales forecasting, budget analysis, and merger/consolidation reports. On the other hand, financial accounting focuses on the production of financial reports, including basic reporting on profitability (this is of specific interest to potential investors). The last key difference between managerial and financial accounting is the regulation and standardization of the two. Financial accountants follow GAAP (generally accepted accounting principles). These principles are set by a professional body. Managerial accountants utilize procedures that are not regulated by a standard-setting body. Both financial and managerial accounting is important to all organizations. Without managerial accounting, management would not be able to forecast and make sound decisions. It helps upper management evaluate, plan...