Q 1 Andrew and Jean have been considering a low-cost endowment mortgage. Briefly explain the problems inherent in such mortgages.

According to Yahoo Finance low-cost endowment mortgage is the most usual form of endowment used to repay a mortgage. It provides life cover, which would pay off the mortgage if the policyholder dies. As long as investment assumptions are met the endowment should provide a lump sum sufficient to repay the mortgage at the end of the term. If the assumptions were exceeded then there would be a lump sum over and above the mortgage amount for the borrower to enjoy. There are many problems with Low cost endowment mortgage:

1. Too dependent on investment: In low cost endowment mortgages the life company invests the money and therefore the amount of money received will depend on how smartly the company has invested the money. If the investment in the policy grows at reasonable rate, then the policy will produce enough at the end of the mortgage term to pay off the loan and produce some extra cash.

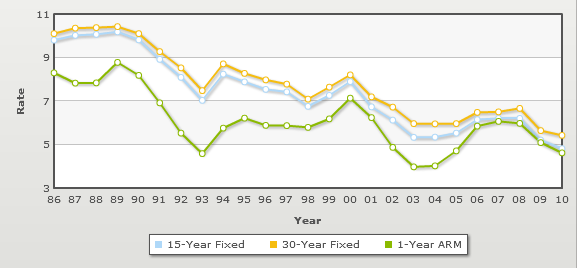

English: Mortgage rates historical trends

English: Mortgage rates historical trends Andrew Jacobs / 20070811.10D.44758 / SML Skydive

Andrew Jacobs / 20070811.10D.44758 / SML Skydive Andrew Jacobs / 20070811.10D.44750 / SML Skydive

Andrew Jacobs / 20070811.10D.44750 / SML Skydive2. No guarantee that loan would be repaid: There is no guarantee that Life Company will invest the money wisely. It is very likely that the endowment policy will not grow enough to produce a substantial profit over and above the amount of the loan, which therefore means it could become more expensive than a repayment mortgage. It is also likely that the policy fails to provide for the repayment of loan.

3. Inflexible: The endowment mortgage is very inflexible. Stopping the endowment policy or cashing it may involve hefty penalties. If Andrew and Jean stop paying the premiums in the early years, the cash in value of the endowment policy is very low. Selling the policy could mean that they loose money...