Topic: The relationship between corporate governance and earnings quality of Hong Kong listed company

Background

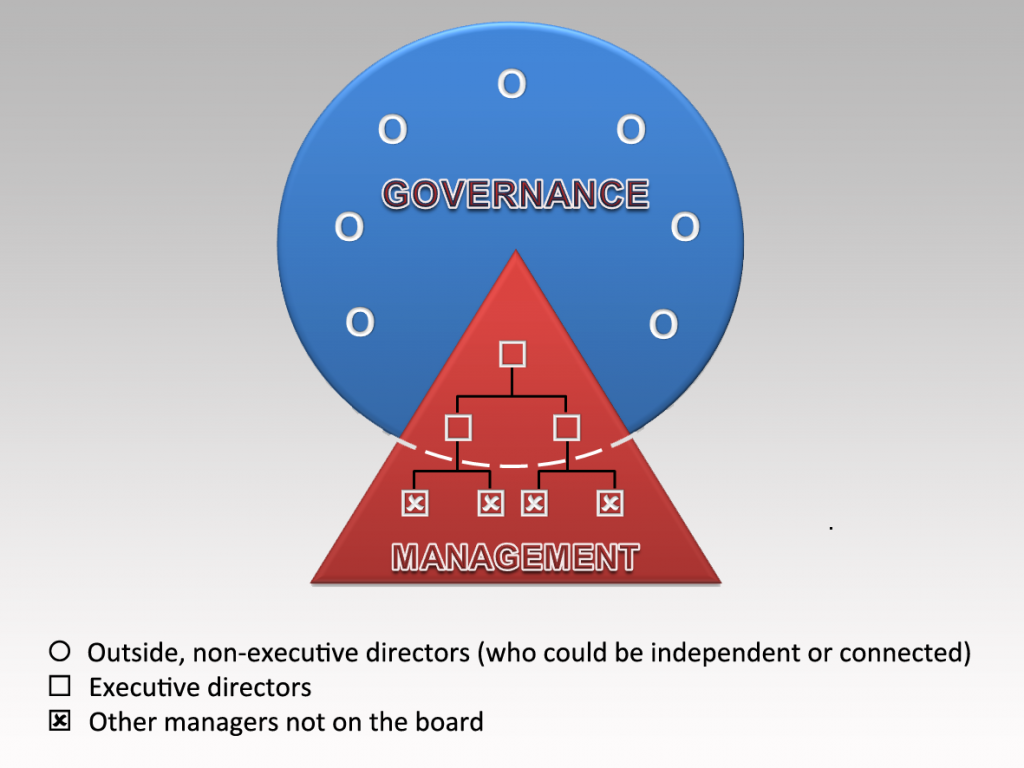

Corporate governance means the relationship between the company's management, board of directors, shareholders and other persons associated with the business interests. Meanwhile, corporate governance also provides a system to allow bodies to set goals, develop strategies to achieve goals, and monitoring bodies' performance. That is what the company's management and the board duties and responsibilities.

Corporate governance, being a crucial issue all over the world, is a no exceptional case for Hong Kong industries as well. Because of corporate governance have an important part for fiduciary responsibilities, responsibility, control mechanisms, auditing and disclose the information to shareholders and others. All related person should abide by the principles of corporate governance in all aspects. And also, the corporate governance system should be designed to detect and prevent fraud.

Moreover, it is being increasingly discussed after the Enron, Adelphia and WorldCom scandals, which had a worldwide outreach (Core, Holthausen, & Larcker, 1999; Loomis, 1999).

Michael Oxley , U.S. Senator from Maryland.

Michael Oxley , U.S. Senator from Maryland. Shore Entertainment, Inc.

Shore Entertainment, Inc. English: Corporate Governance

English: Corporate GovernanceTherefore, the Sarbanes-Oxley Act of 2002 was produced, the most sweeping corporate governance regulation in the US in the last 70 years (Byrnes et al., 2003). The purpose of this Act is to enhance the quality of financial report of listed companies, and to improve the corporate governance structure in order to strengthen the supervision and management positions in the company.

In addition, corporate governance is a certain extent affects the earnings quality. Prior studies have found the Board is the larger of scale, then the company may be more likely to occur financial reporting fraud (Beasley, 1996), and earnings management (DeChow, sloan, & Sweeney, 1996). On the other hand, other studies found that the board size was negatively correlated with earnings management (Chtourou, 2000) and (Xie et al., 2003) also held the...